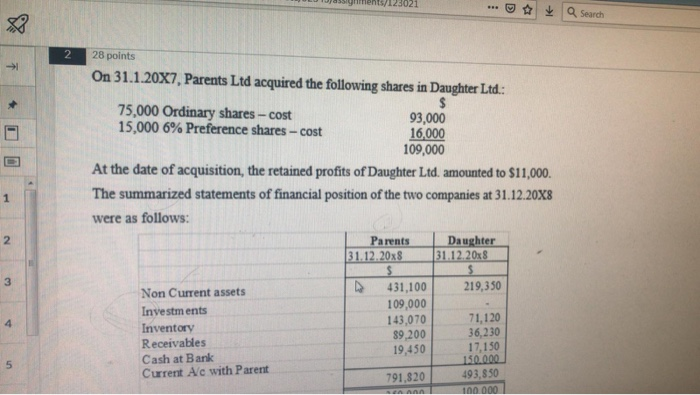

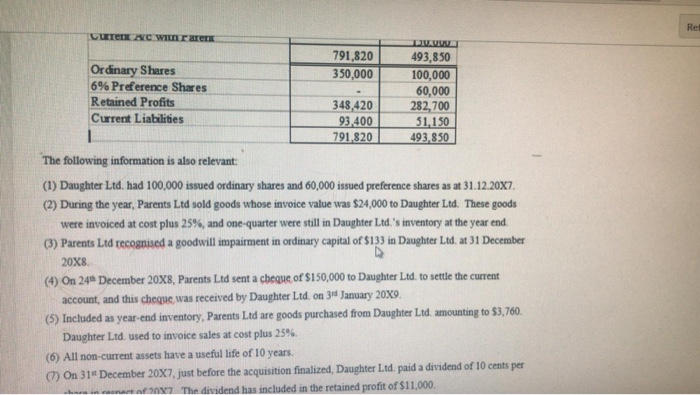

ULU assignment/123021 O Search 2 1 * 1 28 points On 31.1.20X7, Parents Ltd acquired the following shares in Daughter Ltd.: 75,000 Ordinary shares-cost 93,000 15,000 6% Preference shares - cost 109,000 At the date of acquisition, the retained profits of Daughter Ltd. amounted to $11,000. The summarized statements of financial position of the two companies at 31.12.20x8 were as follows: Parents Daughter 31.12.20x8 31.12.20x8 w 219,350 . Non Current assets Investments Inventory Receivables Cash at Bank Current Alc with Parent 431,100 109,000 143,070 89,200 19,450 71,120 36,230 17,150 150.000 493,850 100 000 un 791,820 DIVA 791,820 493,850 Ordinary Shares 350,000 100,000 60,000 Retained Profits 348,420 282,700 Current Liabilities 93,400 51,150 791,820 493,850 The following information is also relevant: (1) Daughter Ltd, had 100,000 issued ordinary shares and 60,000 issued preference shares as at 31.12.20x7. (2) During the year, Parents Ltd sold goods whose invoice value was $24,000 to Daughter Ltd. These goods were invoiced at cost plus 25%, and one-quarter were still in Daughter Ltd.'s inventory at the year end. (3) Parents Ltd recognised a goodwill impairment in ordinary capital of $133 in Daughter Ltd. at 31 December 20X8. (4) On 24 December 20X8, Parents Ltd sent a chegue of $150,000 to Daughter Ltd. to settle the current account, and this cheque was received by Daughter Ltd. on 3rd January 20X9. (5) Included as year end inventory, Parents Ltd are goods purchased from Daughter Lid amounting to $3,760. Daughter Ltd. used to invoice sales at cost plus 25%. (6) All non-current assets have a useful life of 10 years. (7) On 31 December 20X7, just before the acquisition finalized, Daughter Ltd. paid a dividend of 10 cents per in manat The dividend has included in the retained profit of $11,000 ULU assignment/123021 O Search 2 1 * 1 28 points On 31.1.20X7, Parents Ltd acquired the following shares in Daughter Ltd.: 75,000 Ordinary shares-cost 93,000 15,000 6% Preference shares - cost 109,000 At the date of acquisition, the retained profits of Daughter Ltd. amounted to $11,000. The summarized statements of financial position of the two companies at 31.12.20x8 were as follows: Parents Daughter 31.12.20x8 31.12.20x8 w 219,350 . Non Current assets Investments Inventory Receivables Cash at Bank Current Alc with Parent 431,100 109,000 143,070 89,200 19,450 71,120 36,230 17,150 150.000 493,850 100 000 un 791,820 DIVA 791,820 493,850 Ordinary Shares 350,000 100,000 60,000 Retained Profits 348,420 282,700 Current Liabilities 93,400 51,150 791,820 493,850 The following information is also relevant: (1) Daughter Ltd, had 100,000 issued ordinary shares and 60,000 issued preference shares as at 31.12.20x7. (2) During the year, Parents Ltd sold goods whose invoice value was $24,000 to Daughter Ltd. These goods were invoiced at cost plus 25%, and one-quarter were still in Daughter Ltd.'s inventory at the year end. (3) Parents Ltd recognised a goodwill impairment in ordinary capital of $133 in Daughter Ltd. at 31 December 20X8. (4) On 24 December 20X8, Parents Ltd sent a chegue of $150,000 to Daughter Ltd. to settle the current account, and this cheque was received by Daughter Ltd. on 3rd January 20X9. (5) Included as year end inventory, Parents Ltd are goods purchased from Daughter Lid amounting to $3,760. Daughter Ltd. used to invoice sales at cost plus 25%. (6) All non-current assets have a useful life of 10 years. (7) On 31 December 20X7, just before the acquisition finalized, Daughter Ltd. paid a dividend of 10 cents per in manat The dividend has included in the retained profit of $11,000