urgent please!

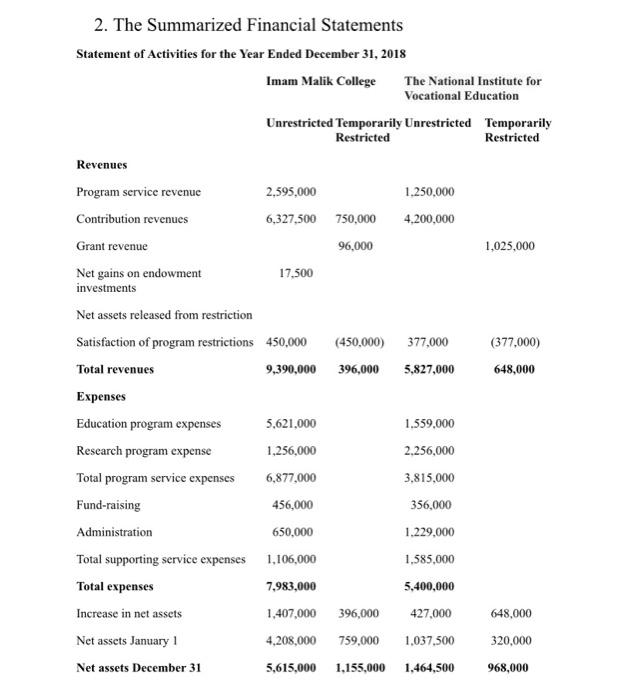

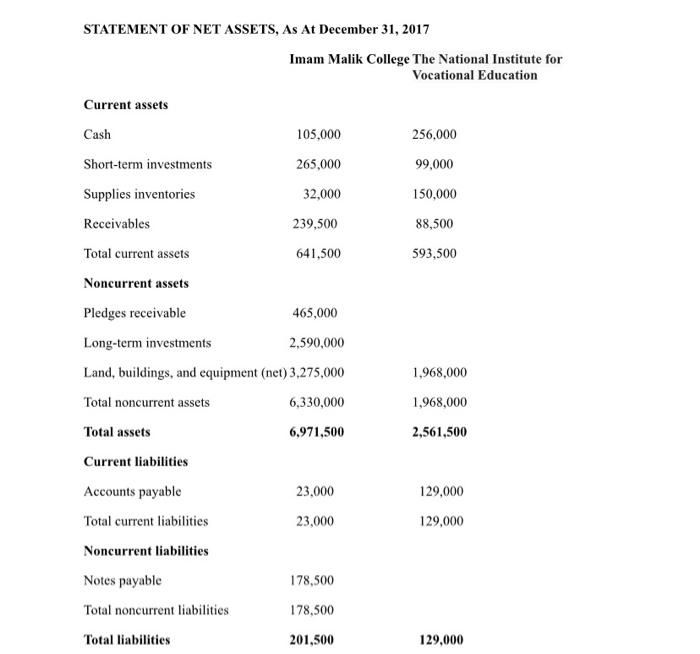

Case Study: Not-for-Profit Organizations: Audit and Performance The National Institute for Vocational Education and Imam Malik College both are offering education on non-profit bases. They generate fund from donations and charity organizations plus rendering limited services and consultancy and charge small fees to cover basic expenditure. The information provided below includes the audit report of one of the institutions (labeled ABC) and the financial statements (except cash flows) for the two not- for-profit organizations. Neither organization has any permanently restricted net assets, which are registered under the names of main donators. 1. Independent Auditors' Report Report on the Financial Statements We have audited the accompanying financial statements of ABC (a nonprofit organization) as of and for the year ended December 31, 20XX, and the related notes to the financial statements, which collectively comprise the Organization's basic financial statements as listed in the table of contents. Management's Responsibility for the Financial Statements Management is responsible for the preparation and fair presentation of these financial statements in accordance with accounting principles generally accepted in the UAE; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of the financial statements that are free from material misstatement, whether due to fraud or error. Auditor's Responsibility Our responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit in accordance with auditing standards generally accepted in the UAE and the standards applicable to financial audits contained in Government Auditing Standards. The financial statements of ABC were not audited in accordance with Government Auditing Standards. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement. An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor's judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the Organization's preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Organization's internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion. Opinion In our opinion, the financial statements referred to above present fairly, in all material respects, the financial position of ABC, as of December 31, 20XX, and the changes in financial position and cash flows for the year then ended in accordance with accounting principles generally accepted. Report on Summarized Comparative Information We have previously audited the Organization's fiscal year 20XX financial statements, and our report dated April XX, 20XX, expressed an unmodified opinion on those audited financial statements. In our opinion, the summarized comparative information presented herein as of and for the year ended December 31, 20XX, is consistent, in all material respects, with the audited financial statements from which it has been derived. Other Matters Required Supplementary Information Accounting principles generally accepted require that the management's discussion and analysis on pages X through Y be presented to supplement the basic financial statements. Such information, although not a part of the financial statements, is required by the Governmental Accounting Standards Board, who considers it to be an essential part of financial reporting for placing the basic financial statements in an appropriate operational, economic, or historical context. We have applied certain limited procedures to the required supplementary information in accordance with auditing standards generally accepted, which consisted of inquiries of management about the methods of preparing the information and comparing the information for consistency with management's responses to our inquiries, the basic financial statements, and other knowledge we obtained during our audit of the basic financial statements. We do not express an opinion or provide any assurance on the information because the limited procedures do not provide us with sufficient evidence to express an opinion or provide any assurance. Other Reporting Required by Government Auditing Standards In accordance with Government Auditing Standards, we have also issued our report dated April XX, 20XX, on our consideration of the Organization's internal control over financial reporting and on our tests of its compliance with certain provisions of laws, regulations, contracts, and grant agreements and other matters. The purpose of that report is to describe the scope of our testing of internal control over financial reporting and compliance and the results of that testing, and not to provide an opinion on internal control over financial reporting or on compliance. That report is an integral part of an audit performed in accordance with Government Auditing Standards in considering the Organization's internal control over financial reporting and compliance. April XX, 20XX 2. The Summarized Financial Statements Statement of Activities for the Year Ended December 31, 2018 Imam Malik College The National Institute for Vocational Education Unrestricted Temporarily Unrestricted Temporarily Restricted Restricted Revenues Program service revenue 2,595,000 1.250,000 Contribution revenues 6,327,500 750,000 4,200,000 Grant revenue 96,000 1,025,000 Net gains on endowment 17.500 investments Net assets released from restriction Satisfaction of program restrictions 450,000 (450.000) 377,000 (377,000) Total revenues 9,390,000 396,000 5,827,000 648,000 Expenses Education program expenses 5,621,000 1.559,000 Research program expense 1,256,000 2.256,000 Total program service expenses 6,877,000 3,815,000 Fund-raising 456,000 356,000 Administration 650,000 1.229,000 Total supporting service expenses 1,106,000 1,585,000 Total expenses 7,983,000 5,400,000 Increase in net assets 1,407,000 396,000 427,000 648,000 Net assets January 1 4,208,000 759,000 1,037,500 320,000 Net assets December 31 5,615,000 1,155,000 1,464,500 968,000 STATEMENT OF NET ASSETS, As At December 31, 2017 Imam Malik College The National Institute for Vocational Education Current assets Cash 105,000 256,000 Short-term investments 265,000 99,000 Supplies inventories 32,000 150,000 Receivables 239,500 88,500 Total current assets 641,500 593,500 Noncurrent assets Pledges receivable 465,000 Long-term investments 2,590,000 Land, buildings, and equipment (net) 3,275,000 1.968,000 Total noncurrent assets 6,330,000 1,968,000 Total assets 6,971,500 2,561,500 Current liabilities 23,000 23,000 129,000 129,000 Accounts payable Total current liabilities Noncurrent liabilities Notes payable Total noncurrent liabilities Total liabilities 178,500 178,500 201,500 129,000 Questions: 1. Provide critical comments on the auditor's report, explaining the strengths and weaknesses of the attached report. 2. If you have been selected to audit both institutions, which audit report and opinion you will submit for each institution. Justify your report. 3. Explain the different types of compliances to be attained in this case and suggest any additional requirements. 4. Calculate the ratios that support the following requirements for both institutions: A. Ability to meet operating expenses from the unrestricted net assets. B. Efficiency of external fund-raising. c Ability to meet short term obligations. D. Assessment of the financial position. e. The level of program expenditure and efficiency, F. Ability to raise and pay debt. G. Explain the self-finance ability of each program. 5. Based on answer of each requirement of 1 above, explain which of the two organizations has the stronger position and performance. Comment and advise the management based on calculated ratios and your own analysis