Answered step by step

Verified Expert Solution

Question

1 Approved Answer

urgently required please check another question. uploaded again QUESTION 3 (12 MARKS) You are a fund manager for high net-wealth clients. One of your clients

urgently required

please check another question. uploaded again

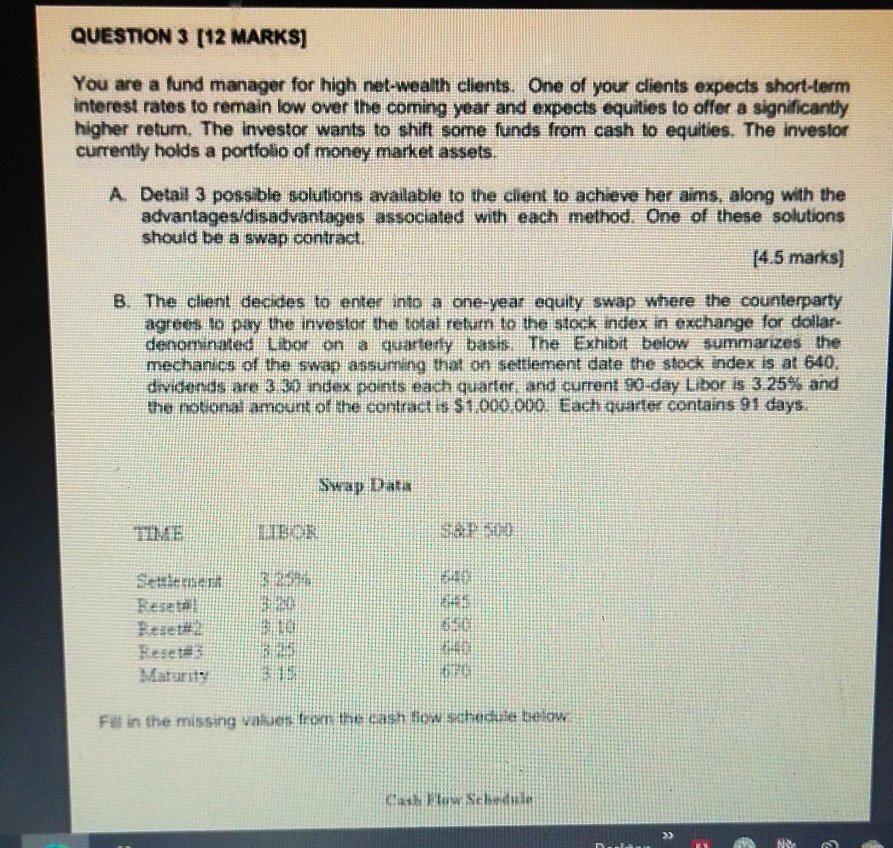

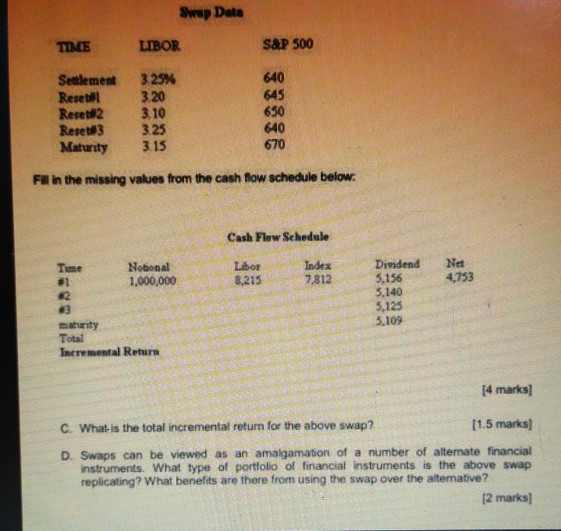

QUESTION 3 (12 MARKS) You are a fund manager for high net-wealth clients. One of your clients expects short-term interest rates to remain low over the coming year and expects equities to offer a significantly higher retum. The investor wants to shift some funds from cash to equities. The investor currently holds a portfolio of money market assets. A Detail 3 possible solutions available to the client to achieve her aims, along with the advantages/disadvantages associated with each method. One of these solutions should be a swap contract, [4.5 marks] B. The client decides to enter into a one-year equity swap where the counterparty agrees to pay the investor the total return to the stock index in exchange for dollar. denominated Libor on a quarterly basis. The Exhibit below summarizes the mechanics of the swap assuming that on settlement date the stock index is at 640. dividends are 3.30 index points each quarter, and current 90-day Libor is 3.25% and the notional amount of the contract it $1.000.000. Each quarter contains 91 days Swap Data TIME DO Set CHE F# in the missing values on the cash flow schedule biellow Claw. Se >>> Swap Data TIME LIBOR S&P 500 Settlement 3.25% Resell 320 Resetil2 3.10 Reset 3 3.25 Maturity 3.15 640 645 650 640 670 Fill in the missing values from the cash flow schedule below. Cash Flow Schedule Time 21 62 Notional 1.000.000 Libor 8,215 Index 7,812 Net 4.753 Dividend 5.156 5.140 5.125 5.109 maturity Total Incremental Return [4 marks] C. What is the total incremental return for the above swap? [1.5 marks] D. Swaps can be viewed as an amalgamation of a number of alternate financial instruments. What type of portfolio of financial instruments is the above swap replicating? What benefits are there from using the swap over the alternative? [2 marks QUESTION 3 (12 MARKS) You are a fund manager for high net-wealth clients. One of your clients expects short-term interest rates to remain low over the coming year and expects equities to offer a significantly higher retum. The investor wants to shift some funds from cash to equities. The investor currently holds a portfolio of money market assets. A Detail 3 possible solutions available to the client to achieve her aims, along with the advantages/disadvantages associated with each method. One of these solutions should be a swap contract, [4.5 marks] B. The client decides to enter into a one-year equity swap where the counterparty agrees to pay the investor the total return to the stock index in exchange for dollar. denominated Libor on a quarterly basis. The Exhibit below summarizes the mechanics of the swap assuming that on settlement date the stock index is at 640. dividends are 3.30 index points each quarter, and current 90-day Libor is 3.25% and the notional amount of the contract it $1.000.000. Each quarter contains 91 days Swap Data TIME DO Set CHE F# in the missing values on the cash flow schedule biellow Claw. Se >>> Swap Data TIME LIBOR S&P 500 Settlement 3.25% Resell 320 Resetil2 3.10 Reset 3 3.25 Maturity 3.15 640 645 650 640 670 Fill in the missing values from the cash flow schedule below. Cash Flow Schedule Time 21 62 Notional 1.000.000 Libor 8,215 Index 7,812 Net 4.753 Dividend 5.156 5.140 5.125 5.109 maturity Total Incremental Return [4 marks] C. What is the total incremental return for the above swap? [1.5 marks] D. Swaps can be viewed as an amalgamation of a number of alternate financial instruments. What type of portfolio of financial instruments is the above swap replicating? What benefits are there from using the swap over the alternative? [2 marksStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Restructuring And Innovation In Banking

Authors: Claudio Scardovi

1st Edition

331940203X, 978-3319402031