Answered step by step

Verified Expert Solution

Question

1 Approved Answer

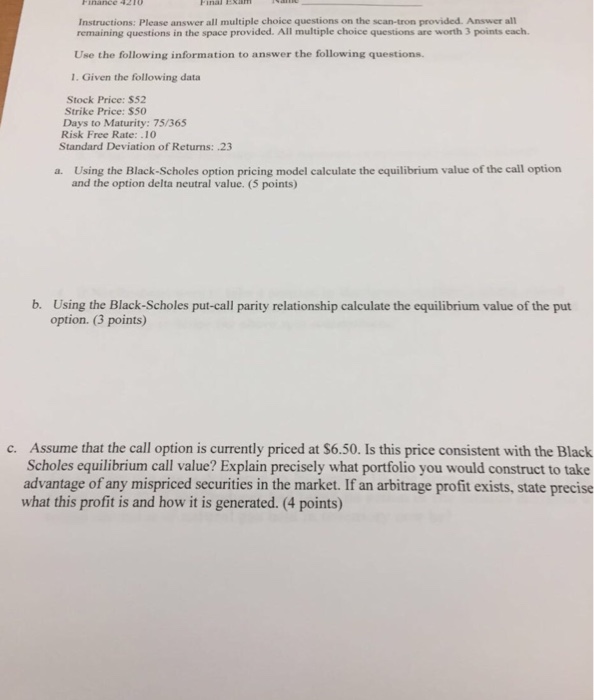

Use the following information to answer the following questions Given the following data Stock Price: $52 Strike Price: $50 Days to Maturity: 75/365 Risk Free

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Derivatives Markets

Authors: Robert L. McDonald

2nd Edition

032128030X, 978-0321280305