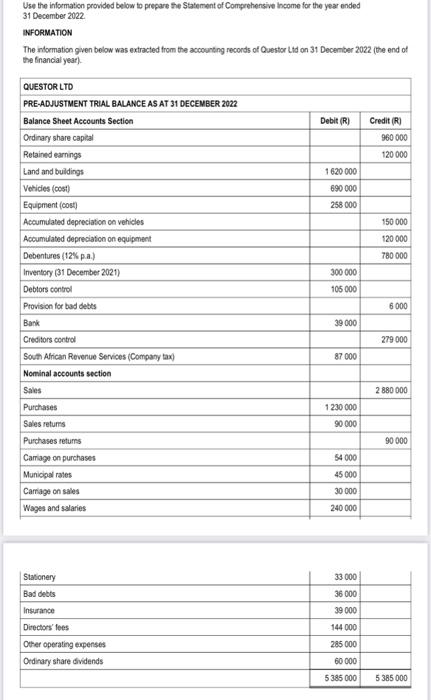

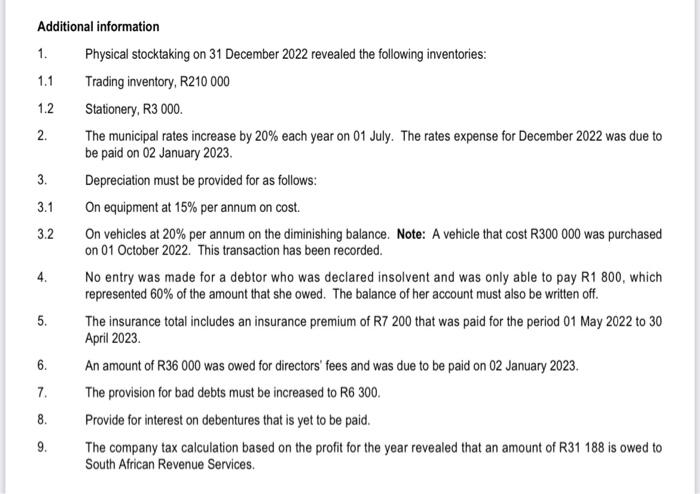

Use the information provided below to prepare the Statement of Comprehensive income for the year ended 31 December 2022. BFORMATION The inlormation given below was extracted from the accounting records of Questor Lid on 31 Decenber 2022 (the end of the financial year). Additional information 1. Physical stocktaking on 31 December 2022 revealed the following inventories: 1.1 Trading inventory, R210 000 1.2 Stationery, R3 000 . 2. The municipal rates increase by 20% each year on 01 July. The rates expense for December 2022 was due to be paid on 02 January 2023. 3. Depreciation must be provided for as follows: 3.1 On equipment at 15% per annum on cost. 3.2 On vehicles at 20% per annum on the diminishing balance. Note: A vehicle that cost R300000 was purchased on 01 October 2022. This transaction has been recorded. 4. No entry was made for a debtor who was declared insolvent and was only able to pay R1 800 , which represented 60% of the amount that she owed. The balance of her account must also be written off. 5. The insurance total includes an insurance premium of R7 200 that was paid for the period 01 May 2022 to 30 April 2023. 6. An amount of R36 000 was owed for directors' fees and was due to be paid on 02 January 2023. 7. The provision for bad debts must be increased to R6300. 8. Provide for interest on debentures that is yet to be paid. 9. The company tax calculation based on the profit for the year revealed that an amount of R31 188 is owed to South African Revenue Services. Use the information provided below to prepare the Statement of Comprehensive income for the year ended 31 December 2022. BFORMATION The inlormation given below was extracted from the accounting records of Questor Lid on 31 Decenber 2022 (the end of the financial year). Additional information 1. Physical stocktaking on 31 December 2022 revealed the following inventories: 1.1 Trading inventory, R210 000 1.2 Stationery, R3 000 . 2. The municipal rates increase by 20% each year on 01 July. The rates expense for December 2022 was due to be paid on 02 January 2023. 3. Depreciation must be provided for as follows: 3.1 On equipment at 15% per annum on cost. 3.2 On vehicles at 20% per annum on the diminishing balance. Note: A vehicle that cost R300000 was purchased on 01 October 2022. This transaction has been recorded. 4. No entry was made for a debtor who was declared insolvent and was only able to pay R1 800 , which represented 60% of the amount that she owed. The balance of her account must also be written off. 5. The insurance total includes an insurance premium of R7 200 that was paid for the period 01 May 2022 to 30 April 2023. 6. An amount of R36 000 was owed for directors' fees and was due to be paid on 02 January 2023. 7. The provision for bad debts must be increased to R6300. 8. Provide for interest on debentures that is yet to be paid. 9. The company tax calculation based on the profit for the year revealed that an amount of R31 188 is owed to South African Revenue Services