Answered step by step

Verified Expert Solution

Question

1 Approved Answer

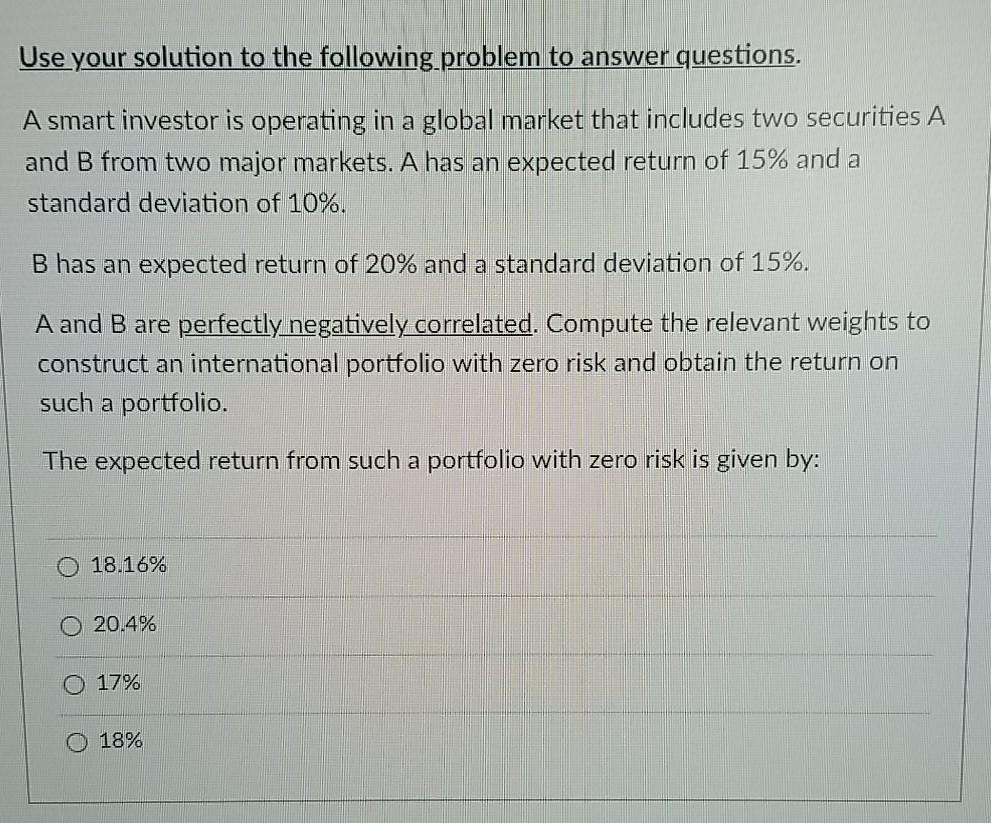

Use your solution to the following problem to answer questions. A smart investor is operating in a global market that includes two securities A and

Use your solution to the following problem to answer questions. A smart investor is operating in a global market that includes two securities A and B from two major markets. A has an expected return of 15% and a standard deviation of 10%. B has an expected return of 20% and a standard deviation of 15%. A and B are perfectly negatively correlated. Compute the relevant weights to construct an international portfolio with zero risk and obtain the return on such a portfolio. The expected return from such a portfolio with zero risk is given by: O 18.16% 20.4% 17% O 18%

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Public Finance An International Perspective

Authors: Joshua E. Greene

1st Edition

9814365041, 978-9814365048