Answered step by step

Verified Expert Solution

Question

1 Approved Answer

USING EXCEL PLEASE! thanks ? The following information relates to Questions 1-12 Amanda Rodriguez is an alternative investments analyst for a US investment management firm,

USING EXCEL PLEASE! thanks

?

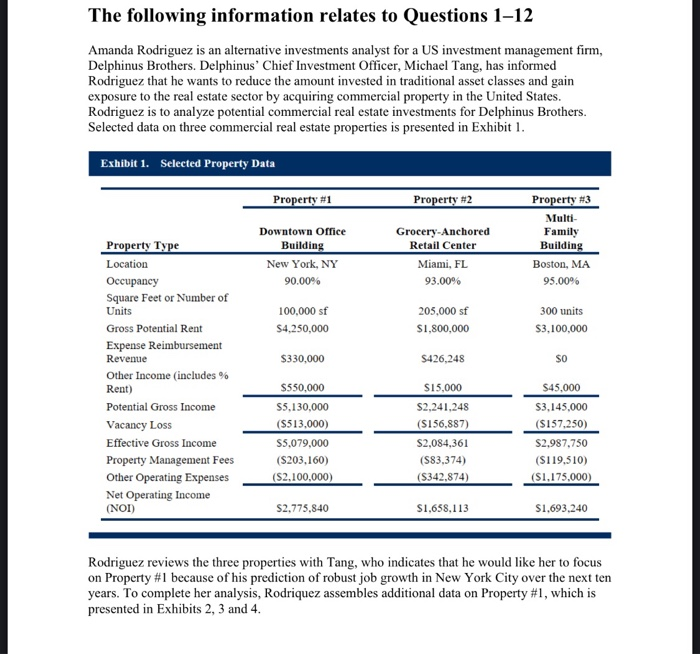

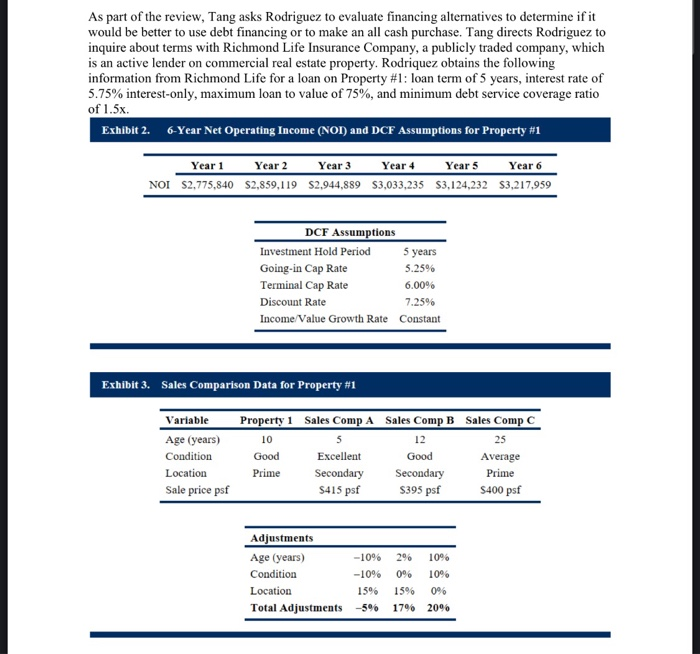

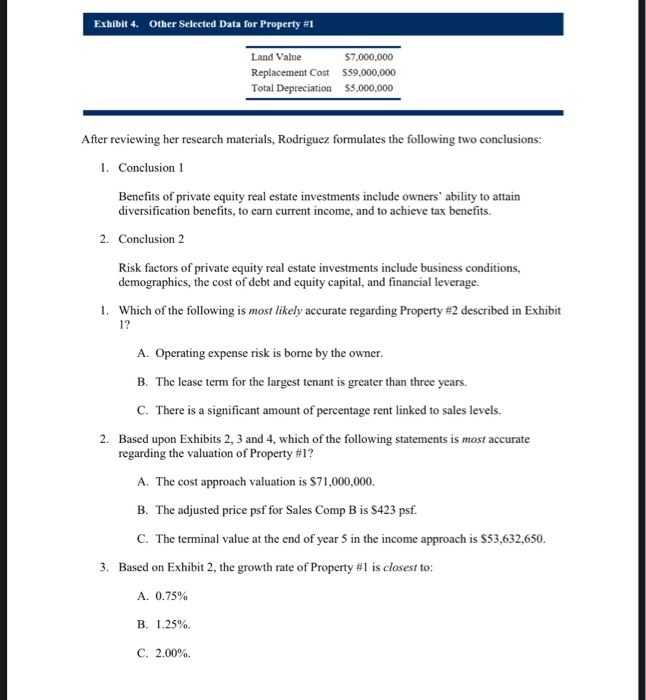

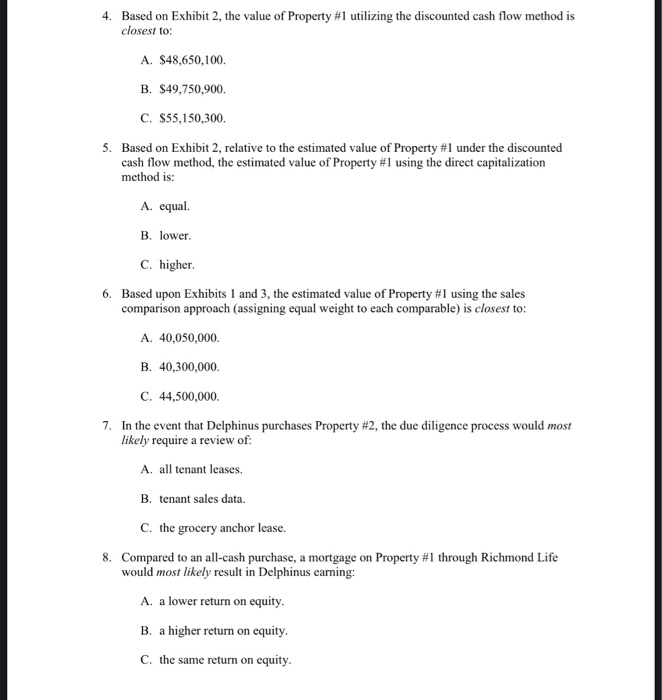

The following information relates to Questions 1-12 Amanda Rodriguez is an alternative investments analyst for a US investment management firm, Delphinus Brothers. Delphinus' Chief Investment Officer, Michael Tang, has informed Rodriguez that he wants to reduce the amount invested in traditional asset classes and gain exposure to the real estate sector by acquiring commercial property in the United States. Rodriguez is to analyze potential commercial real estate investments for Delphinus Brothers. Selected data on three commercial real estate properties is presented in Exhibit 1. Exhibit 1. Selected Property Data Property #1 Property #2 Property #3 Downtown Office Building New York, NY 90.00% Grocery-Anchored Retail Center Miami, FL 93.00% Multi- Family Building Boston, MA 95.00% 100,000 sf $4,250,000 205,000 sf $1,800,000 300 units $3,100,000 $330,000 $426,248 Property Type Location Occupancy Square Feet or Number of Units Gross Potential Rent Expense Reimbursement Revenue Other Income (includes % Rent) Potential Gross Income Vacancy Loss Effective Gross Income Property Management Fees Other Operating Expenses Net Operating Income (NOI) S550.000 SI5,000 $45.000 $2,241,248 (S156.887) $5,130,000 (5513.000) S5,079,000 (S203,160) (S2,100,000) S2,084,361 (583,374) (5342,874) $3,145,000 ($157,250) $2.987,750 (S119.510) (S1.175.000) S2,775,840 $1,658,113 $1.693.240 Rodriguez reviews the three properties with Tang, who indicates that he would like her to focus on Property #1 because of his prediction of robust job growth in New York City over the next ten years. To complete her analysis, Rodriquez assembles additional data on Property #1, which is presented in Exhibits 2, 3 and 4. As part of the review, Tang asks Rodriguez to evaluate financing alternatives to determine if it would be better to use debt financing or to make an all cash purchase. Tang directs Rodriguez to inquire about terms with Richmond Life Insurance Company, a publicly traded company, which is an active lender on commercial real estate property. Rodriquez obtains the following information from Richmond Life for a loan on Property #1: loan term of 5 years, interest rate of 5.75% interest-only, maximum loan to value of 75%, and minimum debt service coverage ratio of 1.5x. Exhibit 2. 6-Year Net Operating Income (NOI) and DCF Assumptions for Property #1 Year 1 Year 2 NOI $2,775,840 $2,859,119 Year 3 Year 4 $2,944,889 $3,033,235 Year 5 $3,124,232 Year 6 $3,217,959 DCF Assumptions Investment Hold Period 5 years Going-in Cap Rate 5.25% Terminal Cap Rate 6.00% Discount Rate 7.25% Income Value Growth Rate Constant Exhibit 3. Sales Comparison Data for Property #1 Variable Property 1 Sales Comp A Sales Comp B Sales Comp C 12 Age (years) Condition Location Sale price psf 10 Good Prime Excellent Secondary $415 psf Good Secondary $395 psf 25 Average Prime S400 psf Adjustments Age (years) Condition Location Total Adjustments -10% -10% 15% -5% 2% 0% 15% 17% 10% 10% 0% 20% Exhibit 4. Other Selected Data for Property #1 Land Value $7,000,000 Replacement Cost S59,000,000 Total Depreciation $5,000,000 After reviewing her research materials, Rodriguez formulates the following two conclusions: 1. Conclusion 1 Benefits of private equity real estate investments include owners' ability to attain diversification benefits, to earn current income, and to achieve tax benefits. 2. Conclusion 2 Risk factors of private equity real estate investments include business conditions, demographics, the cost of debt and equity capital, and financial leverage. 1. Which of the following is most likely accurate regarding Property #2 described in Exhibit A. Operating expense risk is borne by the owner. B. The lease term for the largest tenant is greater than three years. C. There is a significant amount of percentage rent linked to sales levels. 2. Based upon Exhibits 2, 3 and 4, which of the following statements is most accurate regarding the valuation of Property #1? A. The cost approach valuation is $71,000,000. B. The adjusted price psf for Sales Comp B is $423 psf. C. The terminal value at the end of year 5 in the income approach is $53,632,650. 3. Based on Exhibit 2, the growth rate of Property #1 is closest to: A. 0.75% B. 1.25%. C. 2.00% 4. Based on Exhibit 2, the value of Property #1 utilizing the discounted cash flow method is closest to: A. $48,650,100. B. $49,750,900. C. $55,150,300. 5. Based on Exhibit 2, relative to the estimated value o hibit 2, relative to the estimated value of Property #1 under the discounted cash flow method, the estimated value of Property #1 using the direct capitalization method is: A. equal. B. lower. C. higher 6. Based upon Exhibits 1 and 3, the estimated value of Property #1 using the sales comparison approach (assigning equal weight to each comparable) is closest to: A. 40,050,000 B. 40,300,000 C. 44,500,000 7. In the event that Delphinus purchases Property #2, the due diligence process would most likely require a review of: A. all tenant leases. B. tenant sales data. C. the grocery anchor lease. 8. Compared to an all-cash purchase, a mortgage on Property #1 through Richmond Life would most likely result in Delphinus earning: A. a lower return on equity. B. a higher return on equity. C. the same return on equity. 9. Assuming an appraised value of $48,000,000, Richmond Life Insurance Company's maximum loan amount on Property #1 would be closest to: A. $32,000,000. B. $36,000,000. C. $45,000,000. 10. Rodriguez's Conclusion 1 is: A. correct B. incorrect, because tax benefits do not apply to tax-exempt entities. C. incorrect, because private real estate is highly correlated to stocks. 11. Rodriguez's Conclusion 2 is: A. correct. B. incorrect, because inflation is not a risk factor. C. incorrect, because the cost of equity capital is not a risk factor. 12. Richmond Life Insurance Company's potential investment would be most likely described as: A. private real estate debt. B. private real estate equity. C. publicly traded real estate debt. The following information relates to Questions 1-12 Amanda Rodriguez is an alternative investments analyst for a US investment management firm, Delphinus Brothers. Delphinus' Chief Investment Officer, Michael Tang, has informed Rodriguez that he wants to reduce the amount invested in traditional asset classes and gain exposure to the real estate sector by acquiring commercial property in the United States. Rodriguez is to analyze potential commercial real estate investments for Delphinus Brothers. Selected data on three commercial real estate properties is presented in Exhibit 1. Exhibit 1. Selected Property Data Property #1 Property #2 Property #3 Downtown Office Building New York, NY 90.00% Grocery-Anchored Retail Center Miami, FL 93.00% Multi- Family Building Boston, MA 95.00% 100,000 sf $4,250,000 205,000 sf $1,800,000 300 units $3,100,000 $330,000 $426,248 Property Type Location Occupancy Square Feet or Number of Units Gross Potential Rent Expense Reimbursement Revenue Other Income (includes % Rent) Potential Gross Income Vacancy Loss Effective Gross Income Property Management Fees Other Operating Expenses Net Operating Income (NOI) S550.000 SI5,000 $45.000 $2,241,248 (S156.887) $5,130,000 (5513.000) S5,079,000 (S203,160) (S2,100,000) S2,084,361 (583,374) (5342,874) $3,145,000 ($157,250) $2.987,750 (S119.510) (S1.175.000) S2,775,840 $1,658,113 $1.693.240 Rodriguez reviews the three properties with Tang, who indicates that he would like her to focus on Property #1 because of his prediction of robust job growth in New York City over the next ten years. To complete her analysis, Rodriquez assembles additional data on Property #1, which is presented in Exhibits 2, 3 and 4. As part of the review, Tang asks Rodriguez to evaluate financing alternatives to determine if it would be better to use debt financing or to make an all cash purchase. Tang directs Rodriguez to inquire about terms with Richmond Life Insurance Company, a publicly traded company, which is an active lender on commercial real estate property. Rodriquez obtains the following information from Richmond Life for a loan on Property #1: loan term of 5 years, interest rate of 5.75% interest-only, maximum loan to value of 75%, and minimum debt service coverage ratio of 1.5x. Exhibit 2. 6-Year Net Operating Income (NOI) and DCF Assumptions for Property #1 Year 1 Year 2 NOI $2,775,840 $2,859,119 Year 3 Year 4 $2,944,889 $3,033,235 Year 5 $3,124,232 Year 6 $3,217,959 DCF Assumptions Investment Hold Period 5 years Going-in Cap Rate 5.25% Terminal Cap Rate 6.00% Discount Rate 7.25% Income Value Growth Rate Constant Exhibit 3. Sales Comparison Data for Property #1 Variable Property 1 Sales Comp A Sales Comp B Sales Comp C 12 Age (years) Condition Location Sale price psf 10 Good Prime Excellent Secondary $415 psf Good Secondary $395 psf 25 Average Prime S400 psf Adjustments Age (years) Condition Location Total Adjustments -10% -10% 15% -5% 2% 0% 15% 17% 10% 10% 0% 20% Exhibit 4. Other Selected Data for Property #1 Land Value $7,000,000 Replacement Cost S59,000,000 Total Depreciation $5,000,000 After reviewing her research materials, Rodriguez formulates the following two conclusions: 1. Conclusion 1 Benefits of private equity real estate investments include owners' ability to attain diversification benefits, to earn current income, and to achieve tax benefits. 2. Conclusion 2 Risk factors of private equity real estate investments include business conditions, demographics, the cost of debt and equity capital, and financial leverage. 1. Which of the following is most likely accurate regarding Property #2 described in Exhibit A. Operating expense risk is borne by the owner. B. The lease term for the largest tenant is greater than three years. C. There is a significant amount of percentage rent linked to sales levels. 2. Based upon Exhibits 2, 3 and 4, which of the following statements is most accurate regarding the valuation of Property #1? A. The cost approach valuation is $71,000,000. B. The adjusted price psf for Sales Comp B is $423 psf. C. The terminal value at the end of year 5 in the income approach is $53,632,650. 3. Based on Exhibit 2, the growth rate of Property #1 is closest to: A. 0.75% B. 1.25%. C. 2.00% 4. Based on Exhibit 2, the value of Property #1 utilizing the discounted cash flow method is closest to: A. $48,650,100. B. $49,750,900. C. $55,150,300. 5. Based on Exhibit 2, relative to the estimated value o hibit 2, relative to the estimated value of Property #1 under the discounted cash flow method, the estimated value of Property #1 using the direct capitalization method is: A. equal. B. lower. C. higher 6. Based upon Exhibits 1 and 3, the estimated value of Property #1 using the sales comparison approach (assigning equal weight to each comparable) is closest to: A. 40,050,000 B. 40,300,000 C. 44,500,000 7. In the event that Delphinus purchases Property #2, the due diligence process would most likely require a review of: A. all tenant leases. B. tenant sales data. C. the grocery anchor lease. 8. Compared to an all-cash purchase, a mortgage on Property #1 through Richmond Life would most likely result in Delphinus earning: A. a lower return on equity. B. a higher return on equity. C. the same return on equity. 9. Assuming an appraised value of $48,000,000, Richmond Life Insurance Company's maximum loan amount on Property #1 would be closest to: A. $32,000,000. B. $36,000,000. C. $45,000,000. 10. Rodriguez's Conclusion 1 is: A. correct B. incorrect, because tax benefits do not apply to tax-exempt entities. C. incorrect, because private real estate is highly correlated to stocks. 11. Rodriguez's Conclusion 2 is: A. correct. B. incorrect, because inflation is not a risk factor. C. incorrect, because the cost of equity capital is not a risk factor. 12. Richmond Life Insurance Company's potential investment would be most likely described as: A. private real estate debt. B. private real estate equity. C. publicly traded real estate debt Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Personal Finance

Authors: Jack Kapoor

6th Edition

0072350849, 9780072350845