Answered step by step

Verified Expert Solution

Question

1 Approved Answer

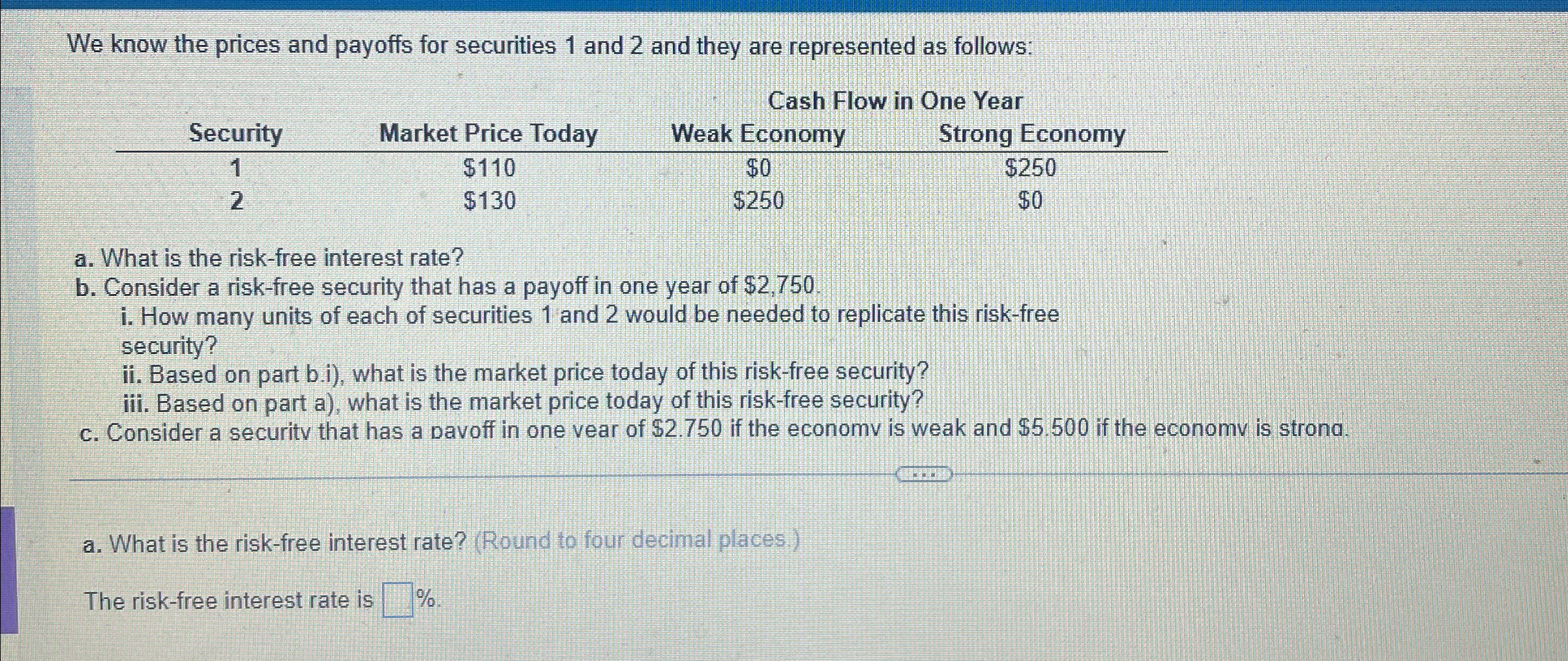

We know the prices and payoffs for securities 1 and 2 and they are represented as follows: Cash Flow in One Year a . What

We know the prices and payoffs for securities and and they are represented as follows:

Cash Flow in One Year

a What is the riskfree interest rate?

b Consider a riskfree security that has a payoff in one year of $

i How many units of each of securities and would be needed to replicate this riskfree

security?

ii Based on part bi what is the market price today of this riskfree security?

iii. Based on part a what is the market price today of this riskfree security?

c Consider a security that has a Davoff in one vear of $ if the economv is weak and $ if the economv is strona.

a What is the riskfree interest rate? Round to four decimal places.

The riskfree interest rate is

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Intermediate Financial Management

Authors: Brigham, Daves

10th Edition

978-1439051764, 1111783659, 9780324594690, 1439051763, 9781111783655, 324594690, 978-1111021573