Question

We look at the situation where the market return is 13% (and you may assume the risk free rate is 3%): a) Assume that the

We look at the situation where the market return is 13% (and you may assume the risk free rate is 3%):

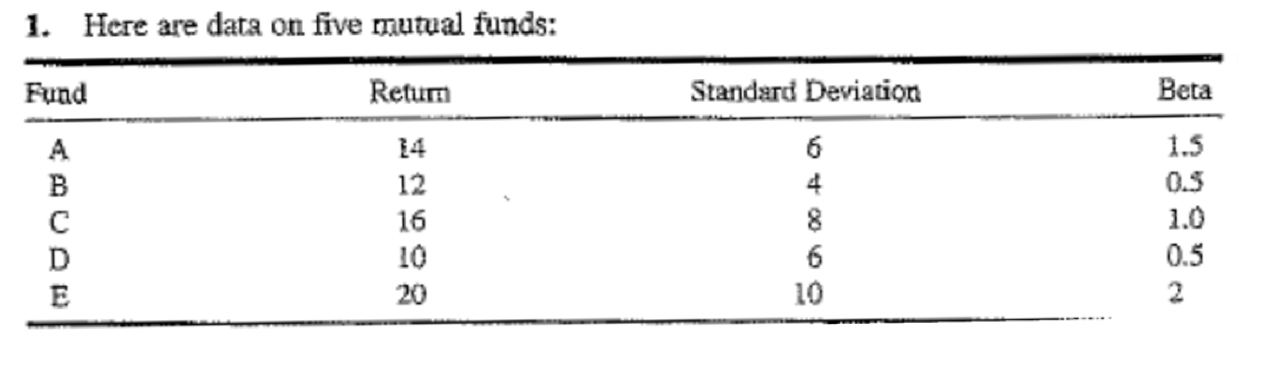

a) Assume that the zero beta form of the CAPM is appropriate. What is the differential return for the funds shown above if the zero beta return is 4%.

b) For funds A & B (above), how much would the return on B have to change to reverse the ranking using the rewardtovariability measure?

1. Here are data on five mutual funds: Fund Retum Standard Deviation Beta A B D E 12 16 10 20 6 4 8 6 10 1.5 0.5 1.0 0.5Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Study Guide To Accompany Corporate Finance

Authors: Jonathan Berk, Peter DeMarzo, Mark Simonson

1st Edition

0321388682, 9780321388681