What are the free cash flows of the packaging-machine investment if it is purchased now and if it is purchased in 3 years? Should Koh approve the investment?

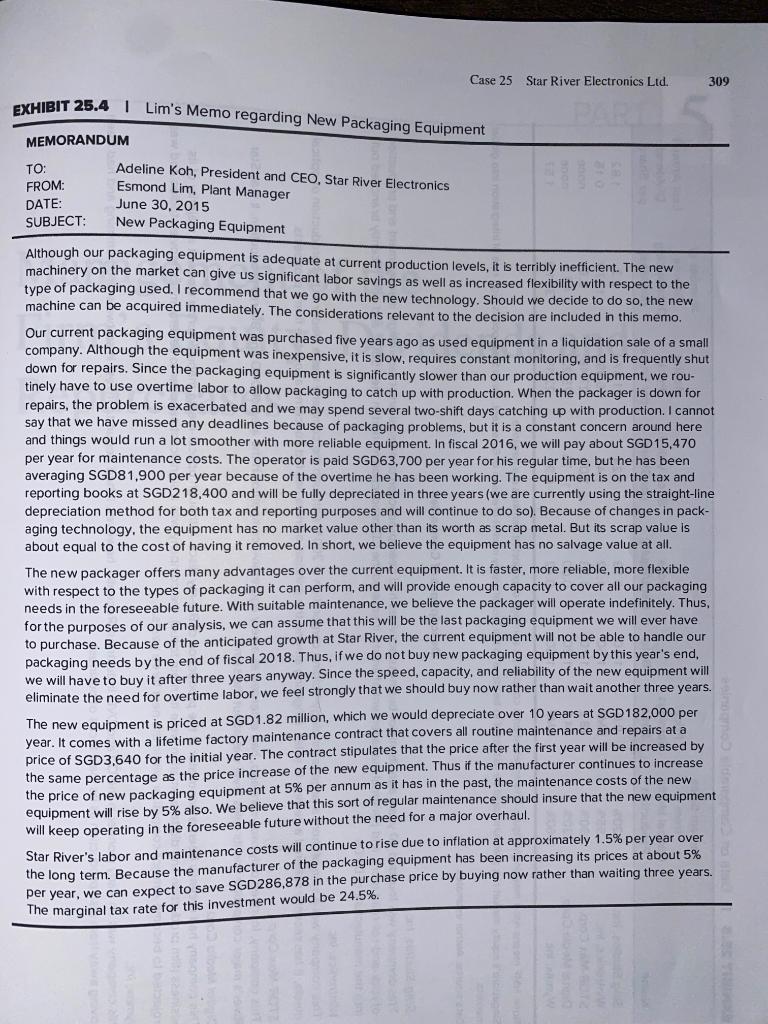

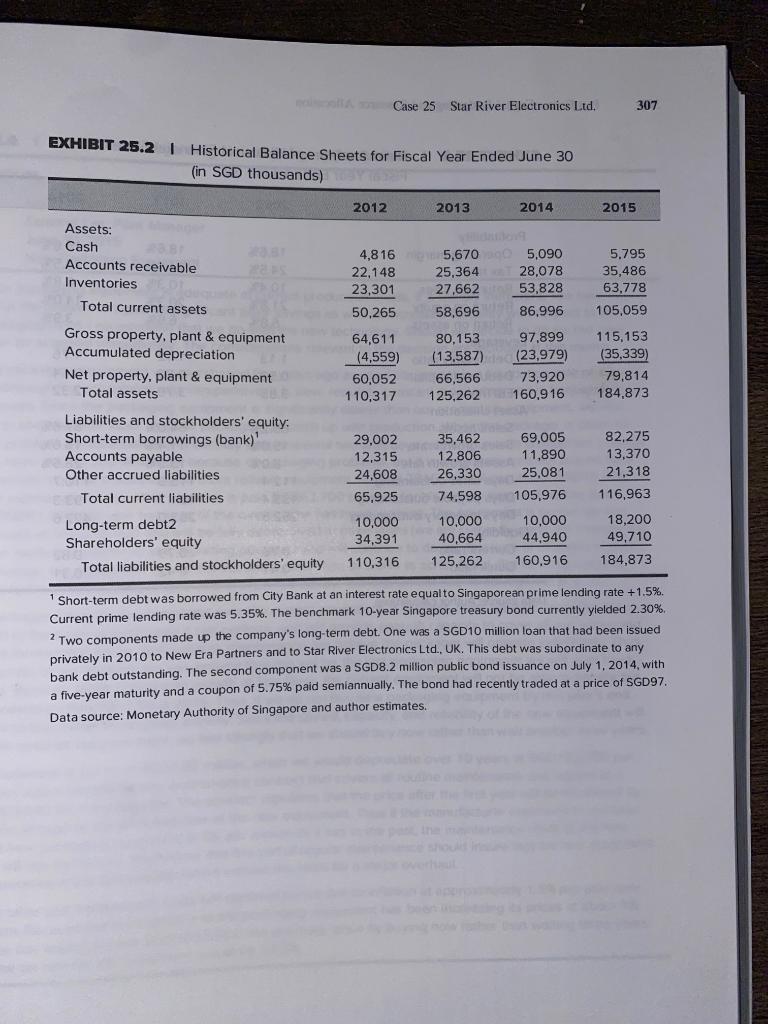

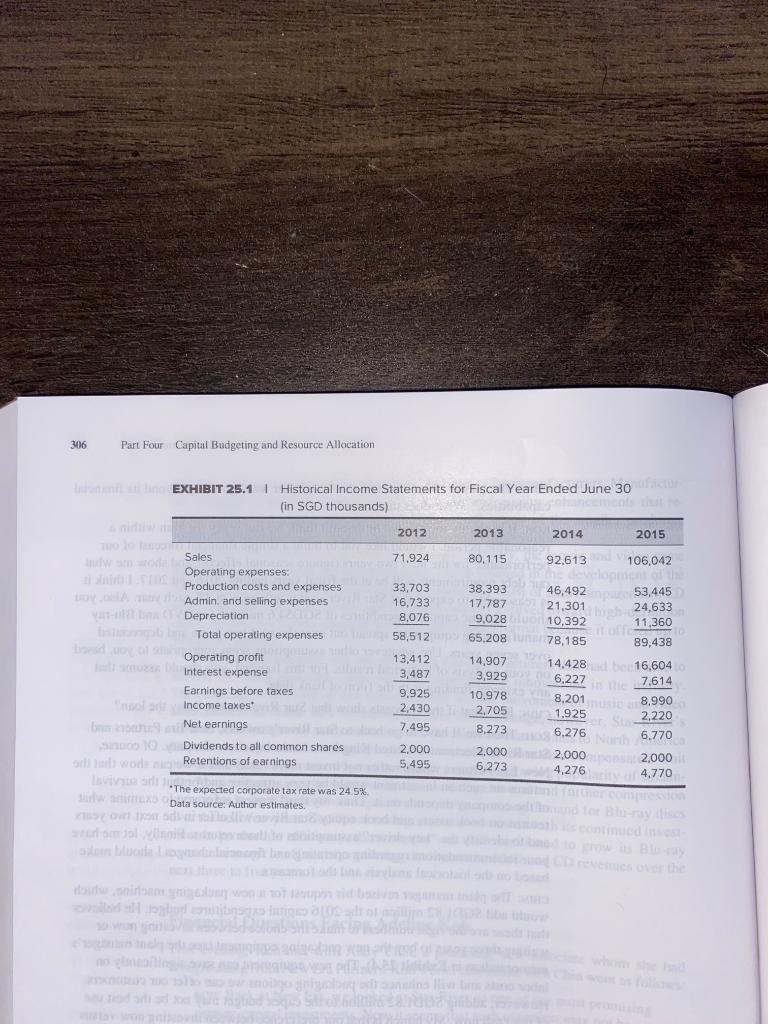

Case 25 Star River Electronics Ltd. 309 EXHIBIT 25.4 Lim's Memo regarding New Packaging Equipment MEMORANDUM TO: FROM DATE: SUBJECT: Adeline Koh, President and CEO, Star River Electronics Esmond Lim, Plant Manager June 30, 2015 New Packaging Equipment Although our packaging equipment is adequate at current production levels, it is terribly inefficient. The new machinery on the market can give us significant labor savings as well as increased flexibility with respect to the type of packaging used. I recommend that we go with the new technology. Should we decide to do so, the new machine can be acquired immediately. The considerations relevant to the decision are included in this memo. Our current packaging equipment was purchased five years ago as used equipment in a liquidation sale of a small company. Although the equipment was inexpensive, it is slow, requires constant monitoring, and is frequently shut down for repairs. Since the packaging equipment is significantly slower than our production equipment, we rou- tinely have to use overtime labor to allow packaging to catch up with production. When the packager is down for repairs, the problem is exacerbated and we may spend several two-shift days catching up with production. I cannot say that we have missed any deadlines because of packaging problems, but it is a constant concern around here and things would run a lot smoother with more reliable equipment. In fiscal 2016, we will pay about SGD15,470 per year for maintenance costs. The operator is paid SGD63,700 per year for his regular time, but he has been averaging SGD81,900 per year because of the overtime he has been working. The equipment is on the tax and reporting books at SGD218,400 and will be fully depreciated in three years (we are currently using the straight-line depreciation method for both tax and reporting purposes and will continue to do so). Because of changes in pack- aging technology, the equipment has no market value other than its worth as scrap metal. But its scrap value is about equal to the cost of having it removed. In short, we believe the equipment has no salvage value at all. The new packager offers many advantages over the current equipment. It is faster, more reliable, more flexible with respect to the types of packaging it can perform, and will provide enough capacity to cover all our packaging needs in the foreseeable future. With suitable maintenance, we believe the packager will operate indefinitely. Thus, for the purposes of our analysis, we can assume that this will be the last packaging equipment we will ever have to purchase. Because of the anticipated growth at Star River, the current equipment will not be able to handle our packaging needs by the end of fiscal 2018. Thus, if we do not buy new packaging equipment by this year's end, we will have to buy it after three years anyway. Since the speed, capacity, and reliability of the new equipment will eliminate the need for overtime labor, we feel strongly that we should buy now rather than wait another three years. The new equipment is priced at SGD1.82 million, which we would depreciate over 10 years at SGD182,000 per year. It comes with a lifetime factory maintenance contract that covers all routine maintenance and repairs at a price of SGD3,640 for the initial year. The contract stipulates that the price after the first year will be increased by the same percentage as the price increase of the new equipment. Thus if the manufacturer continues to increase the price of new packaging equipment at 5% per annum as it has in the past, the maintenance costs of the new equipment will rise by 5% also. We believe that this sort of regular maintenance should insure that the new equipment will keep operating in the foreseeable future without the need for a major overhaul. Star River's labor and maintenance costs will continue to rise due to inflation at approximately 1.5% per year over the long term. Because the manufacturer of the packaging equipment has been increasing its prices at about 5% per year, we can expect to save SGD286,878 in the purchase price by buying now rather than waiting three years. The marginal tax rate for this investment would be 24.5%. Case 25 Star River Electronics Ltd. 307 EXHIBIT 25.2 Historical Balance Sheets for Fiscal Year Ended June 30 (in SGD thousands) 2012 2013 2014 2015 Assets: Cash Accounts receivable Inventories 4,816 22,148 23,301 50,265 Total current assets 5,6700 5,090 25,364 28,078 27,662 53,828 58,696 86,996 80,153 97,899 (13,587) (23,979) 66,566 73.920 125,262 160,916 5.795 35,486 63.778 105,059 115,153 (35,339) 79,814 184,873 64,611 (4,559) 60,052 110,317 Gross property, plant & equipment Accumulated depreciation Net property, plant & equipment Total assets Liabilities and stockholders' equity: Short-term borrowings (bank) Accounts payable Other accrued liabilities Total current liabilities 29,002 12.315 24,608 35,462 12.806 26,330 82,275 13,370 21,318 69,005 11,890 25.081 105,976 10,000 44,940 65,925 74,598 116.963 10,000 34,391 10.000 40,664 18,200 49,710 Long-term debt2 Shareholders' equity Total liabilities and stockholders' equity 110,316 125,262 160.916 184,873 Short-term debt was borrowed from City Bank at an interest rate equalto Singaporean prime lending rate +1.5%. Current prime lending rate was 5.35%. The benchmark 10-year Singapore treasury bond currently yielded 2.30%, 2 Two components made up the company's long-term debt. One was a SGD10 million loan that had been issued privately in 2010 to New Era Partners and to Star River Electronics Ltd., UK. This debt was subordinate to any bank debt outstanding. The second component was a SGD8.2 million public bond issuance on July 1, 2014, with a five-year maturity and a coupon of 5.75% paid semiannually. The bond had recently traded at a price of SGD97. Data source: Monetary Authority of Singapore and author estimates. 306 Part Four Capital Budgeting and Resource Allocation pale EXHIBIT 25.11 Historical Income Statements for Fiscal Year Ended June 30th (in SGD thousands) 2012 2013 2014 2015 71.924 80,115 92,613 106,042 Sales SEOperating expenses: 38,393 17,787 9,028 65,208 Production costs and expenses SNEAdmin and selling expenses Depreciation Total operating expenses Operating profit interest expense Earnings before taxes Income taxes De Net earnings Dividends to all common shares WON Retentions of earnings 33,703 16,733 8,076 58,512 13,412 3,487 9,925 2,430 7,495 2,000 5,495 46,492 53,445 21.301 24,633 10,392 11,360 78,185 89,438 14,428 16,604 6,227 8.990 1.925 6.276 2,000 2,000 4,276 4,770 7.614 14,907 3,929 10,978 2,705 8,273 2,000 6,273 8,201 2,220 6.770 The expected corporate tax rate was 24.5% Data source: Author estimates. do dal pantalla de emocy on mod Case 25 Star River Electronics Ltd. 309 EXHIBIT 25.4 Lim's Memo regarding New Packaging Equipment MEMORANDUM TO: FROM DATE: SUBJECT: Adeline Koh, President and CEO, Star River Electronics Esmond Lim, Plant Manager June 30, 2015 New Packaging Equipment Although our packaging equipment is adequate at current production levels, it is terribly inefficient. The new machinery on the market can give us significant labor savings as well as increased flexibility with respect to the type of packaging used. I recommend that we go with the new technology. Should we decide to do so, the new machine can be acquired immediately. The considerations relevant to the decision are included in this memo. Our current packaging equipment was purchased five years ago as used equipment in a liquidation sale of a small company. Although the equipment was inexpensive, it is slow, requires constant monitoring, and is frequently shut down for repairs. Since the packaging equipment is significantly slower than our production equipment, we rou- tinely have to use overtime labor to allow packaging to catch up with production. When the packager is down for repairs, the problem is exacerbated and we may spend several two-shift days catching up with production. I cannot say that we have missed any deadlines because of packaging problems, but it is a constant concern around here and things would run a lot smoother with more reliable equipment. In fiscal 2016, we will pay about SGD15,470 per year for maintenance costs. The operator is paid SGD63,700 per year for his regular time, but he has been averaging SGD81,900 per year because of the overtime he has been working. The equipment is on the tax and reporting books at SGD218,400 and will be fully depreciated in three years (we are currently using the straight-line depreciation method for both tax and reporting purposes and will continue to do so). Because of changes in pack- aging technology, the equipment has no market value other than its worth as scrap metal. But its scrap value is about equal to the cost of having it removed. In short, we believe the equipment has no salvage value at all. The new packager offers many advantages over the current equipment. It is faster, more reliable, more flexible with respect to the types of packaging it can perform, and will provide enough capacity to cover all our packaging needs in the foreseeable future. With suitable maintenance, we believe the packager will operate indefinitely. Thus, for the purposes of our analysis, we can assume that this will be the last packaging equipment we will ever have to purchase. Because of the anticipated growth at Star River, the current equipment will not be able to handle our packaging needs by the end of fiscal 2018. Thus, if we do not buy new packaging equipment by this year's end, we will have to buy it after three years anyway. Since the speed, capacity, and reliability of the new equipment will eliminate the need for overtime labor, we feel strongly that we should buy now rather than wait another three years. The new equipment is priced at SGD1.82 million, which we would depreciate over 10 years at SGD182,000 per year. It comes with a lifetime factory maintenance contract that covers all routine maintenance and repairs at a price of SGD3,640 for the initial year. The contract stipulates that the price after the first year will be increased by the same percentage as the price increase of the new equipment. Thus if the manufacturer continues to increase the price of new packaging equipment at 5% per annum as it has in the past, the maintenance costs of the new equipment will rise by 5% also. We believe that this sort of regular maintenance should insure that the new equipment will keep operating in the foreseeable future without the need for a major overhaul. Star River's labor and maintenance costs will continue to rise due to inflation at approximately 1.5% per year over the long term. Because the manufacturer of the packaging equipment has been increasing its prices at about 5% per year, we can expect to save SGD286,878 in the purchase price by buying now rather than waiting three years. The marginal tax rate for this investment would be 24.5%. Case 25 Star River Electronics Ltd. 307 EXHIBIT 25.2 Historical Balance Sheets for Fiscal Year Ended June 30 (in SGD thousands) 2012 2013 2014 2015 Assets: Cash Accounts receivable Inventories 4,816 22,148 23,301 50,265 Total current assets 5,6700 5,090 25,364 28,078 27,662 53,828 58,696 86,996 80,153 97,899 (13,587) (23,979) 66,566 73.920 125,262 160,916 5.795 35,486 63.778 105,059 115,153 (35,339) 79,814 184,873 64,611 (4,559) 60,052 110,317 Gross property, plant & equipment Accumulated depreciation Net property, plant & equipment Total assets Liabilities and stockholders' equity: Short-term borrowings (bank) Accounts payable Other accrued liabilities Total current liabilities 29,002 12.315 24,608 35,462 12.806 26,330 82,275 13,370 21,318 69,005 11,890 25.081 105,976 10,000 44,940 65,925 74,598 116.963 10,000 34,391 10.000 40,664 18,200 49,710 Long-term debt2 Shareholders' equity Total liabilities and stockholders' equity 110,316 125,262 160.916 184,873 Short-term debt was borrowed from City Bank at an interest rate equalto Singaporean prime lending rate +1.5%. Current prime lending rate was 5.35%. The benchmark 10-year Singapore treasury bond currently yielded 2.30%, 2 Two components made up the company's long-term debt. One was a SGD10 million loan that had been issued privately in 2010 to New Era Partners and to Star River Electronics Ltd., UK. This debt was subordinate to any bank debt outstanding. The second component was a SGD8.2 million public bond issuance on July 1, 2014, with a five-year maturity and a coupon of 5.75% paid semiannually. The bond had recently traded at a price of SGD97. Data source: Monetary Authority of Singapore and author estimates. 306 Part Four Capital Budgeting and Resource Allocation pale EXHIBIT 25.11 Historical Income Statements for Fiscal Year Ended June 30th (in SGD thousands) 2012 2013 2014 2015 71.924 80,115 92,613 106,042 Sales SEOperating expenses: 38,393 17,787 9,028 65,208 Production costs and expenses SNEAdmin and selling expenses Depreciation Total operating expenses Operating profit interest expense Earnings before taxes Income taxes De Net earnings Dividends to all common shares WON Retentions of earnings 33,703 16,733 8,076 58,512 13,412 3,487 9,925 2,430 7,495 2,000 5,495 46,492 53,445 21.301 24,633 10,392 11,360 78,185 89,438 14,428 16,604 6,227 8.990 1.925 6.276 2,000 2,000 4,276 4,770 7.614 14,907 3,929 10,978 2,705 8,273 2,000 6,273 8,201 2,220 6.770 The expected corporate tax rate was 24.5% Data source: Author estimates. do dal pantalla de emocy on mod