Answered step by step

Verified Expert Solution

Question

1 Approved Answer

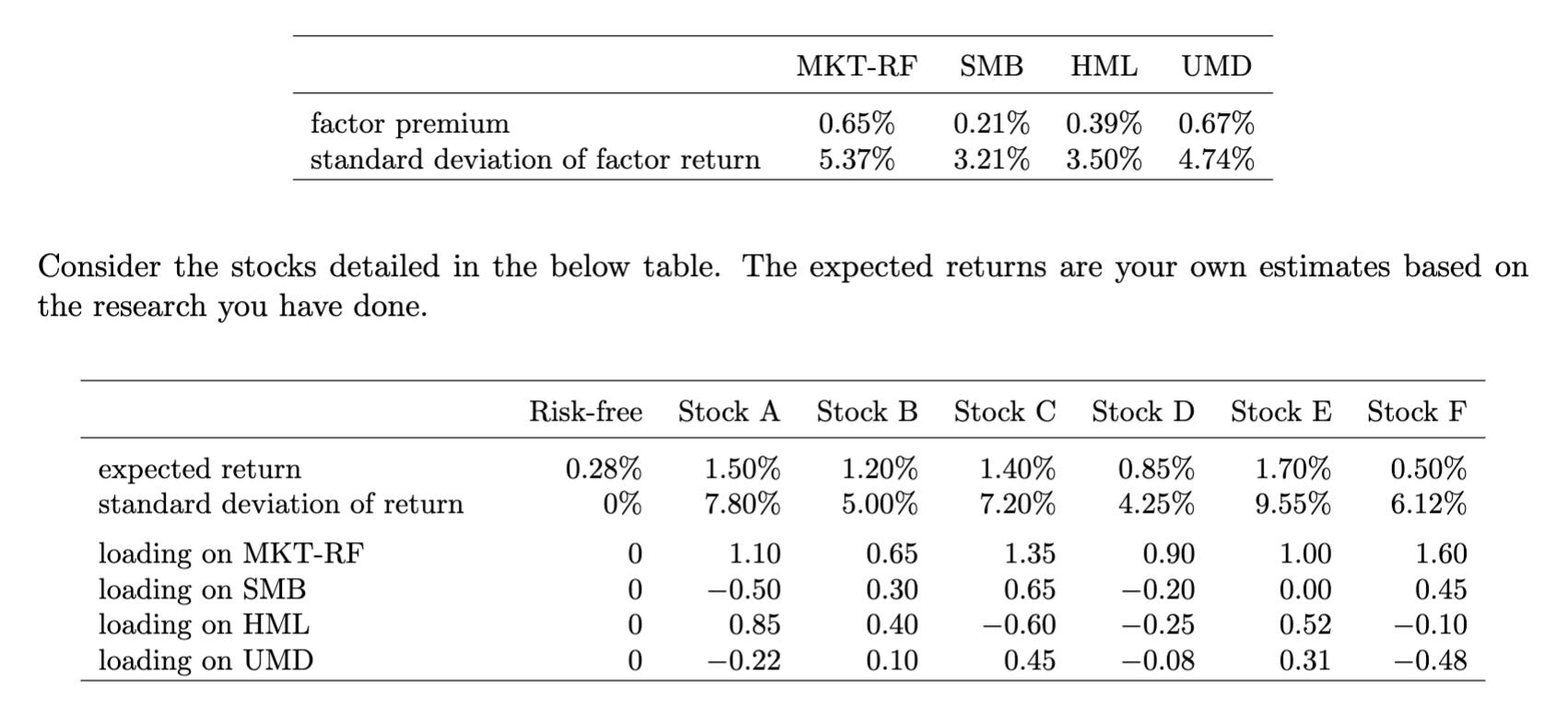

What is the alpha of each stock? factor premium MKT-RF SMB HML UMD 0.65% 0.21% 0.39% 0.67% standard deviation of factor return 5.37% 3.21% 3.50%

What is the alpha of each stock?

factor premium MKT-RF SMB HML UMD 0.65% 0.21% 0.39% 0.67% standard deviation of factor return 5.37% 3.21% 3.50% 4.74% Consider the stocks detailed in the below table. The expected returns are your own estimates based on the research you have done. Risk-free Stock A Stock B Stock C Stock D Stock E Stock F expected return 0.28% 1.50% 1.20% 1.40% 0.85% 1.70% 0.50% standard deviation of return 0% 7.80% 5.00% 7.20% 4.25% 9.55% 6.12% loading on MKT-RF 0 1.10 0.65 1.35 0.90 1.00 1.60 loading on SMB 0 -0.50 0.30 0.65 -0.20 0.00 0.45 loading on HML 0 0.85 0.40 -0.60 -0.25 0.52 -0.10 loading on UMD 0 -0.22 0.10 0.45 -0.08 0.31 -0.48

Step by Step Solution

★★★★★

3.54 Rating (161 Votes )

There are 3 Steps involved in it

Step: 1

To calculate the alpha of each stock we can use th...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Principles of Finance

Authors: Scott Besley, Eugene F. Brigham

6th edition

9781305178045, 1285429648, 1305178041, 978-1285429649