Answered step by step

Verified Expert Solution

Question

1 Approved Answer

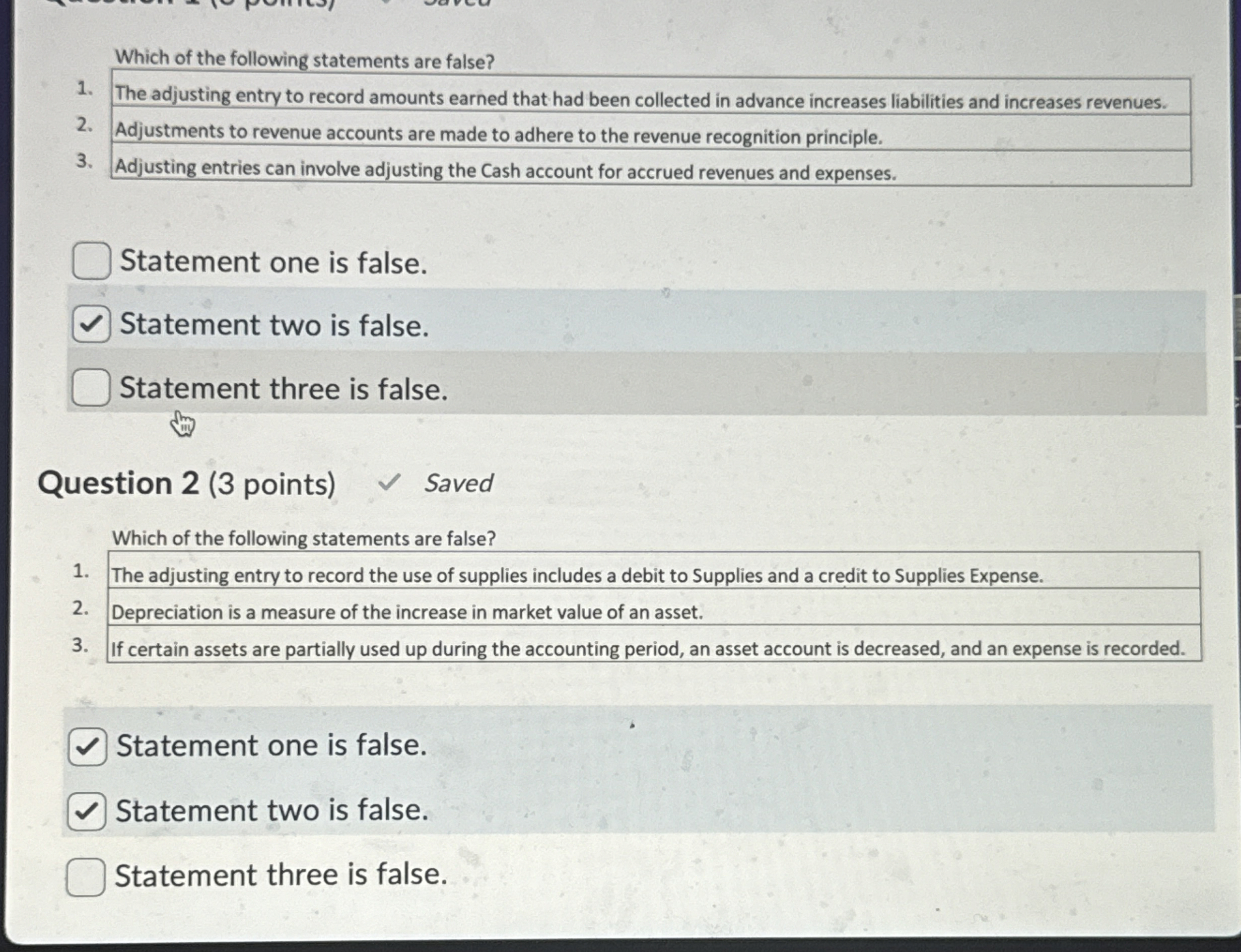

Which of the following statements are false? The adjusting entry to record amounts earned that had been collected in advance increases liabilities and increases revenues.

Which of the following statements are false?

The adjusting entry to record amounts earned that had been collected in advance increases liabilities and increases revenues.

Adjustments to revenue accounts are made to adhere to the revenue recognition principle.

Adjusting entries can involve adjusting the Cash account for accrued revenues and expenses.

Statement one is false.

Statement two is false.

Statement three is false.

Question points

Saved

Which of the following statements are false?

The adjusting entry to record the use of supplies includes a debit to Supplies and a credit to Supplies Expense.

Depreciation is a measure of the increase in market value of an asset.

If certain assets are partially used up during the accounting period, an asset account is decreased, and an expense is recorded.

Statement one is false.

Statement two is false.

Statement three is false.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Cornerstones of Financial and Managerial Accounting

Authors: Rich Jones, Mowen, Hansen, Heitger

1st Edition

9780538751292, 324787359, 538751290, 978-0324787351