- Why does the current outstanding debt value have to be subtracted from the enterprise value to get to price per share?

- In the first half of this case, the portfolio manager, Kimi Ford, has already performed the Discounted Cash Flow analysis herself, and arrived at an equity value per share of $37.27. What is the cost of capital that she uses to get this stock price?

- Kimi Ford then asks her assistant, Joanna Cohen, to estimate Nikes cost of capital, a single number in the DCF analysis. Why is this number so crucial in corporate valuation?

- To estimate the cost of capital, the finance industry looks at cost of debt (rd), cost of equity (re), and the weights of debt and equity (D% and E%), i.e., Weighted Average Cost of Capital. Lets first look at the weights. Assume that the book value of debt is a close proxy for the market value of debt (this is actually a result of Question 8).

What is the book value (Year of 2001) of shareholders equity? What is D% and E%?

What is the current market value of shareholders equity? What is D% and E%?

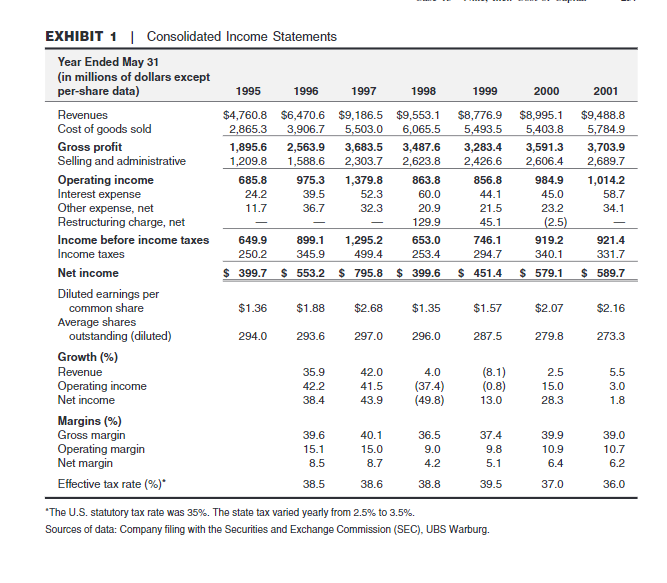

2001 $9,488.8 5,784.9 3,703.9 2,689.7 1,014.2 58.7 34.1 921.4 331.7 $ 589.7 EXHIBIT 1 | Consolidated Income Statements Year Ended May 31 (in millions of dollars except per-share data) 1995 1996 1997 1998 1999 2000 Revenues $4,760.8 $6,470.6 $9,186.5 $9,553.1 $8,776.9 $8,995.1 Cost of goods sold 2,865.3 3,906.7 5,503.0 6,065.5 5,493.5 5,403.8 Gross profit 1,895.6 2,563.9 3,683.5 3,487.6 3,283.4 3,591.3 Selling and administrative 1,209.8 1,588.6 2,303.7 2,623.8 2,426.6 2,606.4 Operating income 685.8 975.3 1,379.8 863.8 856.8 984.9 Interest expense 24.2 39.5 52.3 60.0 44.1 45.0 Other expense, net 11.7 36.7 32.3 20.9 21.5 23.2 Restructuring charge, net 129.9 45.1 (2.5) Income before income taxes 649.9 899.1 1,295.2 653.0 746.1 9192 Income taxes 250.2 345.9 499.4 253.4 294.7 340.1 Net income $ 399.7 $ 553.2 $ 795.8 $ 399.6 $ 451.4 $ 579.1 Diluted earnings per common share $1.36 $1.88 $2.68 $1.35 $1.57 $2.07 Average shares outstanding (diluted) 294.0 293.6 297.0 296.0 287.5 279.8 Growth (%) Revenue 35.9 42.0 4.0 (8.1) 2.5 Operating income 42.2 41.5 (37.4) (0.8) 15.0 Net income 38.4 43.9 (49.8) 13.0 28.3 Margins (%) Gross margin 39.6 40.1 36.5 37.4 39.9 Operating margin 15.1 15.0 9.0 9.8 10.9 Net margin 8.5 8.7 4.2 5.1 6.4 Effective tax rate (%) 38.5 38.6 38.8 39.5 37.0 "The U.S. statutory tax rate was 35%. The state tax varied yearly from 2.5% to 3.5%. Sources of data: Company filing with the Securities and Exchange Commission (SEC), UBS Warburg. $2.16 273.3 5.5 3.0 1.8 39.0 10.7 6.2 36.0 Nike, Inc.: Cost of Capital On July 5, 2001, Kimi Ford, a portfolio manager at NorthPoint Group, a mutual-fund management firm, pored over analysts' write-ups of Nike, Inc., the athletic-shoe man- ufacturer. Nike's share price had declined significantly from the beginning of the year. Ford was considering buying some shares for the fund she managed, the NorthPoint Large-Cap Fund, which invested mostly in Fortune 500 companies, with an emphasis on value investing. Its top holdings included ExxonMobil, General Motors, McDonald's, 3M, and other large-cap, generally old-economy stocks. While the stock market had declined over the last 18 months, the NorthPoint Large-Cap Fund had performed extremely well. In 2000, the fund earned a return of 20.7%, even as the S&P 500 fell 10.1%. At the end of June 2001, the fund's year-to-date returns stood at 6.4% versus -7.3% for the S&P 500. Only a week earlier, on June 28, 2001, Nike had held an analysts' meeting to dis- close its fiscal-year 2001 results. The meeting, however, had another purpose: Nike management wanted to communicate a strategy for revitalizing the company. Since 1997, its revenues had plateaued at around $9 billion, while net income had fallen from almost $800 million to $580 million (see Exhibit 1). Nike's market share in U.S. athletic shoes had fallen from 48%, in 1997, to 42% in 2000. In addition, recent supply-chain issues and the adverse effect of a strong dollar had negatively affected revenue. At the meeting, management revealed plans to address both top-line growth and operating performance. To boost revenue, the company would develop more athletic- shoe products in the midpriced segmenta segment that Nike had overlooked in recent years. Nike also planned to push its apparel line, which, under the recent leadership of 'Nike's fiscal year ended in May. Douglas Robson, Just Do... Something: Nike's insularity and Foot-Dragging Have It Running in Place," Business Week, (2 July 2001). Sneakers in this segment sold for $70 $90 a pair, 2001 $9,488.8 5,784.9 3,703.9 2,689.7 1,014.2 58.7 34.1 921.4 331.7 $ 589.7 EXHIBIT 1 | Consolidated Income Statements Year Ended May 31 (in millions of dollars except per-share data) 1995 1996 1997 1998 1999 2000 Revenues $4,760.8 $6,470.6 $9,186.5 $9,553.1 $8,776.9 $8,995.1 Cost of goods sold 2,865.3 3,906.7 5,503.0 6,065.5 5,493.5 5,403.8 Gross profit 1,895.6 2,563.9 3,683.5 3,487.6 3,283.4 3,591.3 Selling and administrative 1,209.8 1,588.6 2,303.7 2,623.8 2,426.6 2,606.4 Operating income 685.8 975.3 1,379.8 863.8 856.8 984.9 Interest expense 24.2 39.5 52.3 60.0 44.1 45.0 Other expense, net 11.7 36.7 32.3 20.9 21.5 23.2 Restructuring charge, net 129.9 45.1 (2.5) Income before income taxes 649.9 899.1 1,295.2 653.0 746.1 9192 Income taxes 250.2 345.9 499.4 253.4 294.7 340.1 Net income $ 399.7 $ 553.2 $ 795.8 $ 399.6 $ 451.4 $ 579.1 Diluted earnings per common share $1.36 $1.88 $2.68 $1.35 $1.57 $2.07 Average shares outstanding (diluted) 294.0 293.6 297.0 296.0 287.5 279.8 Growth (%) Revenue 35.9 42.0 4.0 (8.1) 2.5 Operating income 42.2 41.5 (37.4) (0.8) 15.0 Net income 38.4 43.9 (49.8) 13.0 28.3 Margins (%) Gross margin 39.6 40.1 36.5 37.4 39.9 Operating margin 15.1 15.0 9.0 9.8 10.9 Net margin 8.5 8.7 4.2 5.1 6.4 Effective tax rate (%) 38.5 38.6 38.8 39.5 37.0 "The U.S. statutory tax rate was 35%. The state tax varied yearly from 2.5% to 3.5%. Sources of data: Company filing with the Securities and Exchange Commission (SEC), UBS Warburg. $2.16 273.3 5.5 3.0 1.8 39.0 10.7 6.2 36.0 Nike, Inc.: Cost of Capital On July 5, 2001, Kimi Ford, a portfolio manager at NorthPoint Group, a mutual-fund management firm, pored over analysts' write-ups of Nike, Inc., the athletic-shoe man- ufacturer. Nike's share price had declined significantly from the beginning of the year. Ford was considering buying some shares for the fund she managed, the NorthPoint Large-Cap Fund, which invested mostly in Fortune 500 companies, with an emphasis on value investing. Its top holdings included ExxonMobil, General Motors, McDonald's, 3M, and other large-cap, generally old-economy stocks. While the stock market had declined over the last 18 months, the NorthPoint Large-Cap Fund had performed extremely well. In 2000, the fund earned a return of 20.7%, even as the S&P 500 fell 10.1%. At the end of June 2001, the fund's year-to-date returns stood at 6.4% versus -7.3% for the S&P 500. Only a week earlier, on June 28, 2001, Nike had held an analysts' meeting to dis- close its fiscal-year 2001 results. The meeting, however, had another purpose: Nike management wanted to communicate a strategy for revitalizing the company. Since 1997, its revenues had plateaued at around $9 billion, while net income had fallen from almost $800 million to $580 million (see Exhibit 1). Nike's market share in U.S. athletic shoes had fallen from 48%, in 1997, to 42% in 2000. In addition, recent supply-chain issues and the adverse effect of a strong dollar had negatively affected revenue. At the meeting, management revealed plans to address both top-line growth and operating performance. To boost revenue, the company would develop more athletic- shoe products in the midpriced segmenta segment that Nike had overlooked in recent years. Nike also planned to push its apparel line, which, under the recent leadership of 'Nike's fiscal year ended in May. Douglas Robson, Just Do... Something: Nike's insularity and Foot-Dragging Have It Running in Place," Business Week, (2 July 2001). Sneakers in this segment sold for $70 $90 a pair