Answered step by step

Verified Expert Solution

Question

1 Approved Answer

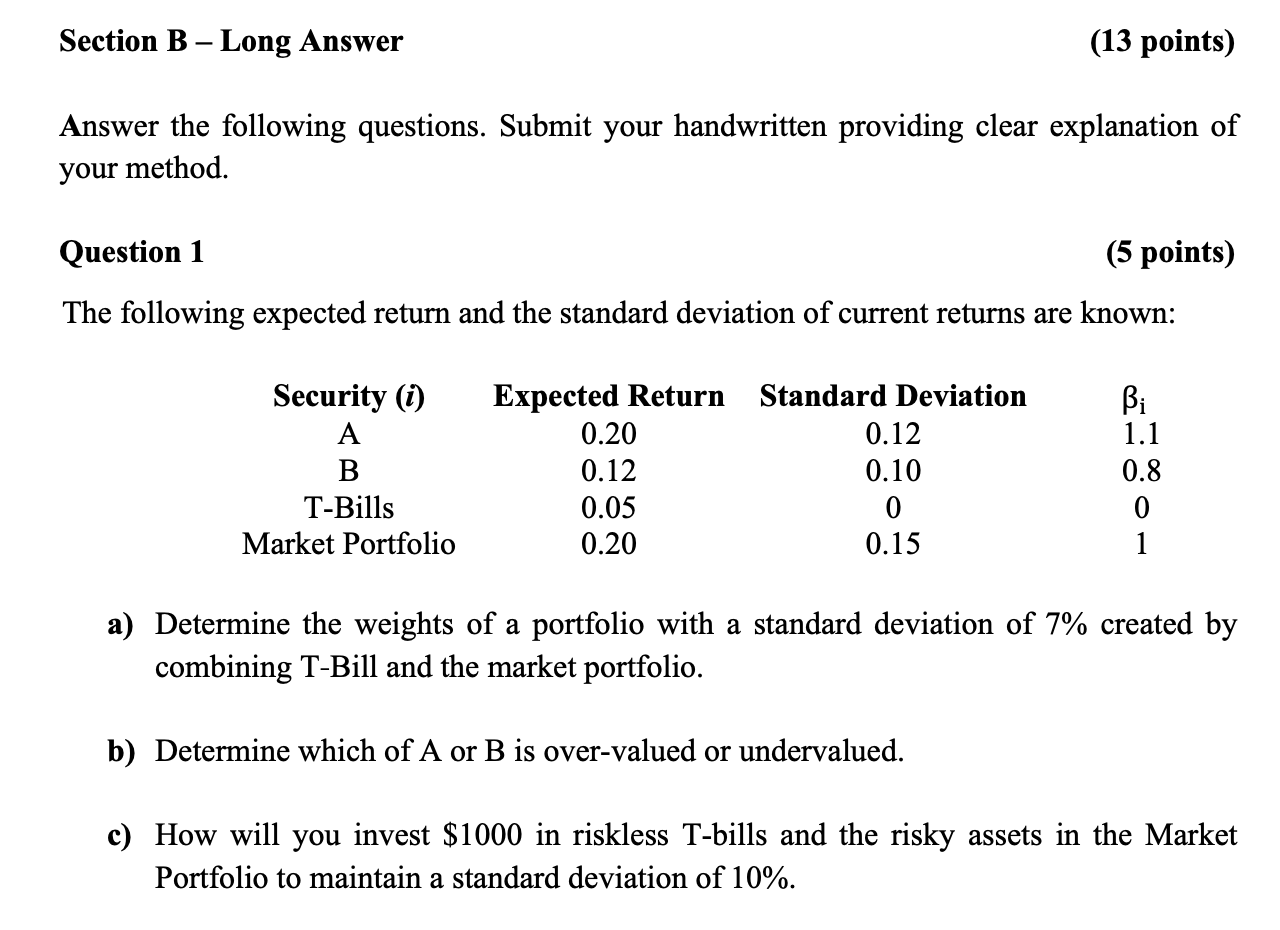

Without Excel and with process Section B - Long Answer (13 points) Answer the following questions. Submit your handwritten providing clear explanation of your method.

Without Excel and with process

Without Excel and with process

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Project Financing Financial Instruments And Risk Management

Authors: Frank J Fabozzi, Carmel De Nahlik

1st Edition

9811231494, 9789811231490