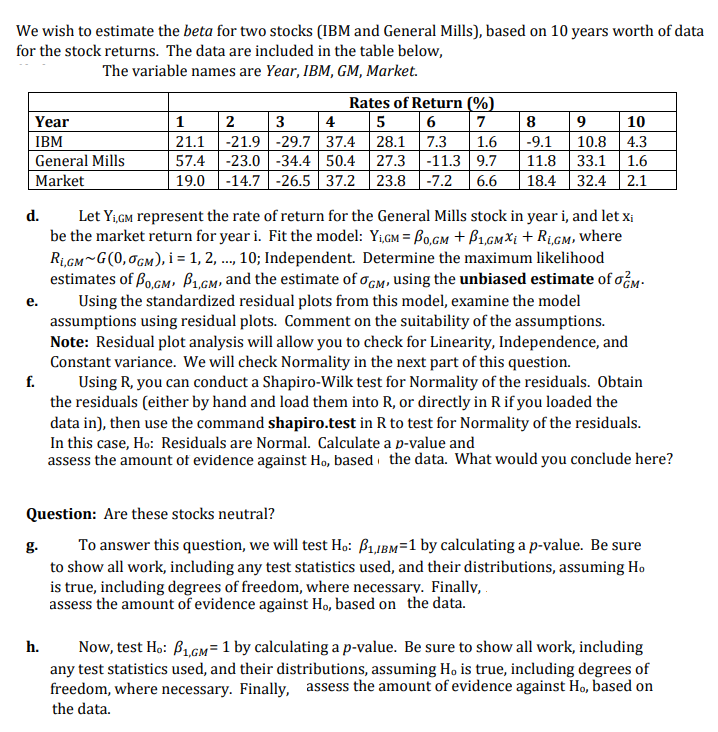

Year IBM GM Market 1 21.1 57.4 19.0 2 -21.9 -23.0 -14.7 3 -29.7 -34.4 -26.5 4 37.4 50.4 37.2 5 28.1 27.3 23.8 6 7.3 -11.3 -7.2 7 1.6 9.7 6.6 8 -9.1 11.8 18.4 9 10.8 33.1 32.4 10 4.3 1.6 2.1

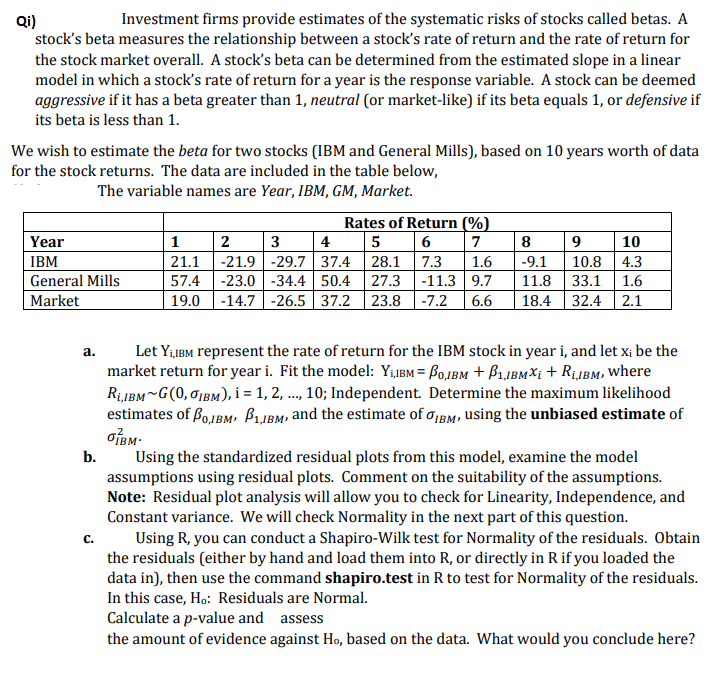

Qi) Investment firms provide estimates of the systematic risks of stocks called betas. A stock's beta measures the relationship between a stock's rate of return and the rate of return for the stock market overall. A stock's beta can be determined from the estimated slope in a linear model in which a stock's rate of return for a year is the response variable. A stock can be deemed aggressive if it has a beta greater than 1, neutral (or market-like) if its beta equals 1, or defensive if its beta is less than 1. We wish to estimate the beta for two stocks (IBM and General Mills), based on 10 years worth of data for the stock returns. The data are included in the table below, The variable names are Year, IBM, GM, Market. Rates of Return (%) Year 1 2 3 4 5 6 7 8 9 10 IBM 21.1 -21.9 -29.7 37.4 28.1 7.3 1.6 -9.1 10.8 4.3 General Mills 57.4 -23.0-34.4 50.4 27.3 -11.3 9.7 11.8 33.1 1.6 Market 19.0 -14.7 -26.5 37.2 23.8-7.2 6.6 18.4 32.4 2.1 a. b. Let Yiibm represent the rate of return for the IBM stock in year i, and let xi be the market return for year i. Fit the model: Y,IBM = B0,1bm + B1,1bmXi + Ri,bm, where R1,1BM~G(0,01BM), i = 1, 2, ..., 10; Independent. Determine the maximum likelihood estimates of Bolbm, B1,1bm, and the estimate of iem, using the unbiased estimate of OM Using the standardized residual plots from this model, examine the model assumptions using residual plots. Comment on the suitability of the assumptions. Note: Residual plot analysis will allow you to check for Linearity, Independence, and Constant variance. We will check Normality in the next part of this question. Using R, you can conduct a Shapiro-Wilk test for Normality of the residuals. Obtain the residuals (either by hand and load them into R, or directly in Rif you loaded the data in), then use the command shapiro.test in R to test for Normality of the residuals. In this case, H.: Residuals are Normal. Calculate a p-value and assess the amount of evidence against Ho, based on the data. What would you conclude here? c. We wish to estimate the beta for two stocks (IBM and General Mills), based on 10 years worth of data for the stock returns. The data are included in the table below, The variable names are Year, IBM, GM, Market. Rates of Return (% Year 1 2 3 4 5 6 7 8 9 10 IBM 21.1 -21.9 -29.737.4 28.1 7.3 1.6 -9.1 10.8 4.3 General Mills 57.4 -23.0-34.4 50.4 27.3 -11.3 9.7 11.8 33.1 1.6 Market 19.0 -14.7 -26.5 37.2 23.8 -7.2 6.6 18.4 32.4 2.1 d. e. Let Yigm represent the rate of return for the General Mills stock in year i, and let Xi be the market return for year i. Fit the model: Yi,GM = Bo,gm + B1,GmXi + Ri,gm, where Rigm~G(0,06m), i = 1, 2, ..., 10; Independent. Determine the maximum likelihood estimates of Bo,gm, B1,0m, and the estimate of Ogm, using the unbiased estimate of om- Using the standardized residual plots from this model, examine the model assumptions using residual plots. Comment on the suitability of the assumptions. Note: Residual plot analysis will allow you to check for Linearity, Independence, and Constant variance. We will check Normality in the next part of this question. Using R, you can conduct a Shapiro-Wilk test for Normality of the residuals. Obtain the residuals (either by hand and load them into R, or directly in R if you loaded the data in), then use the command shapiro.test in R to test for Normality of the residuals. In this case, Ho: Residuals are Normal. Calculate a p-value and assess the amount of evidence against Ho, based the data. What would you conclude here? f. Question: Are these stocks neutral? g. To answer this question, we will test Ho: B1,1bm=1 by calculating a p-value. Be sure to show all work, including any test statistics used, and their distributions, assuming Ho is true, including degrees of freedom, where necessary. Finally, assess the amount of evidence against Ho, based on the data. h. Now, test Ho: B1,5m= 1 by calculating a p-value. Be sure to show all work, including any test statistics used, and their distributions, assuming H, is true, including degrees of freedom, where necessary. Finally, assess the amount of evidence against H., based on the data. Qi) Investment firms provide estimates of the systematic risks of stocks called betas. A stock's beta measures the relationship between a stock's rate of return and the rate of return for the stock market overall. A stock's beta can be determined from the estimated slope in a linear model in which a stock's rate of return for a year is the response variable. A stock can be deemed aggressive if it has a beta greater than 1, neutral (or market-like) if its beta equals 1, or defensive if its beta is less than 1. We wish to estimate the beta for two stocks (IBM and General Mills), based on 10 years worth of data for the stock returns. The data are included in the table below, The variable names are Year, IBM, GM, Market. Rates of Return (%) Year 1 2 3 4 5 6 7 8 9 10 IBM 21.1 -21.9 -29.7 37.4 28.1 7.3 1.6 -9.1 10.8 4.3 General Mills 57.4 -23.0-34.4 50.4 27.3 -11.3 9.7 11.8 33.1 1.6 Market 19.0 -14.7 -26.5 37.2 23.8-7.2 6.6 18.4 32.4 2.1 a. b. Let Yiibm represent the rate of return for the IBM stock in year i, and let xi be the market return for year i. Fit the model: Y,IBM = B0,1bm + B1,1bmXi + Ri,bm, where R1,1BM~G(0,01BM), i = 1, 2, ..., 10; Independent. Determine the maximum likelihood estimates of Bolbm, B1,1bm, and the estimate of iem, using the unbiased estimate of OM Using the standardized residual plots from this model, examine the model assumptions using residual plots. Comment on the suitability of the assumptions. Note: Residual plot analysis will allow you to check for Linearity, Independence, and Constant variance. We will check Normality in the next part of this question. Using R, you can conduct a Shapiro-Wilk test for Normality of the residuals. Obtain the residuals (either by hand and load them into R, or directly in Rif you loaded the data in), then use the command shapiro.test in R to test for Normality of the residuals. In this case, H.: Residuals are Normal. Calculate a p-value and assess the amount of evidence against Ho, based on the data. What would you conclude here? c. We wish to estimate the beta for two stocks (IBM and General Mills), based on 10 years worth of data for the stock returns. The data are included in the table below, The variable names are Year, IBM, GM, Market. Rates of Return (% Year 1 2 3 4 5 6 7 8 9 10 IBM 21.1 -21.9 -29.737.4 28.1 7.3 1.6 -9.1 10.8 4.3 General Mills 57.4 -23.0-34.4 50.4 27.3 -11.3 9.7 11.8 33.1 1.6 Market 19.0 -14.7 -26.5 37.2 23.8 -7.2 6.6 18.4 32.4 2.1 d. e. Let Yigm represent the rate of return for the General Mills stock in year i, and let Xi be the market return for year i. Fit the model: Yi,GM = Bo,gm + B1,GmXi + Ri,gm, where Rigm~G(0,06m), i = 1, 2, ..., 10; Independent. Determine the maximum likelihood estimates of Bo,gm, B1,0m, and the estimate of Ogm, using the unbiased estimate of om- Using the standardized residual plots from this model, examine the model assumptions using residual plots. Comment on the suitability of the assumptions. Note: Residual plot analysis will allow you to check for Linearity, Independence, and Constant variance. We will check Normality in the next part of this question. Using R, you can conduct a Shapiro-Wilk test for Normality of the residuals. Obtain the residuals (either by hand and load them into R, or directly in R if you loaded the data in), then use the command shapiro.test in R to test for Normality of the residuals. In this case, Ho: Residuals are Normal. Calculate a p-value and assess the amount of evidence against Ho, based the data. What would you conclude here? f. Question: Are these stocks neutral? g. To answer this question, we will test Ho: B1,1bm=1 by calculating a p-value. Be sure to show all work, including any test statistics used, and their distributions, assuming Ho is true, including degrees of freedom, where necessary. Finally, assess the amount of evidence against Ho, based on the data. h. Now, test Ho: B1,5m= 1 by calculating a p-value. Be sure to show all work, including any test statistics used, and their distributions, assuming H, is true, including degrees of freedom, where necessary. Finally, assess the amount of evidence against H., based on the data