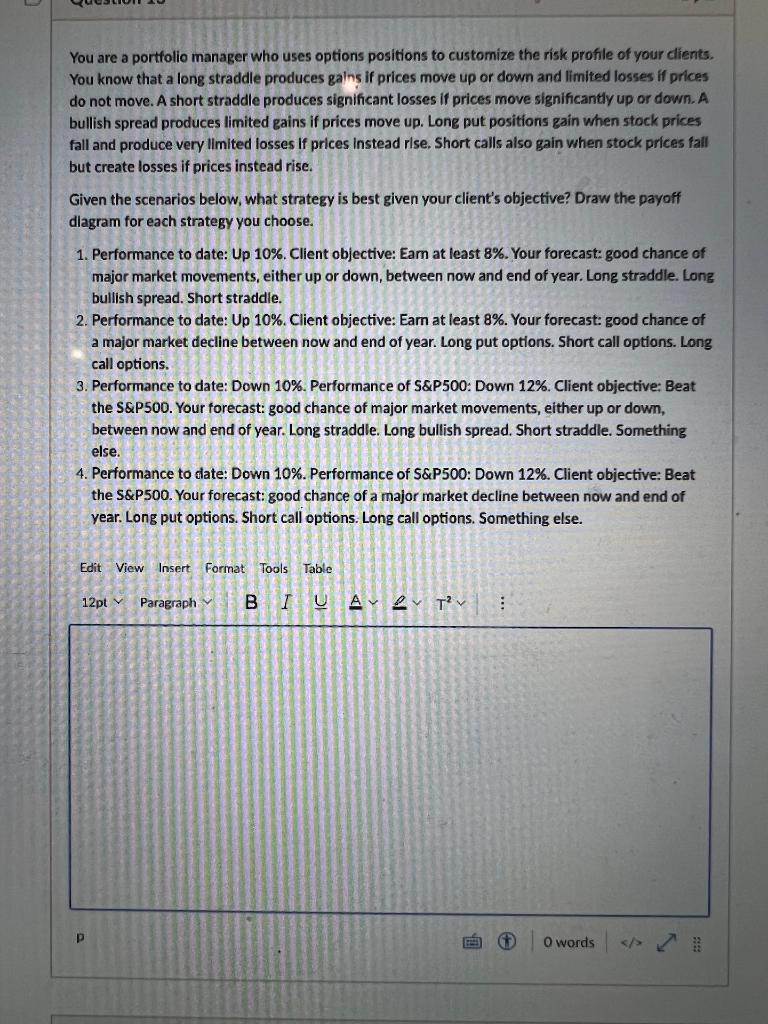

You are a portfolio manager who uses options positions to customize the risk profile of your clients. You know that a long straddle produces gains if prices move up or down and limited losses if prices do not move. A short straddle produces significant losses if prices move significantly up or down. A bullish spread produces limited gains if prices move up. Long put positions gain when stock prices fall and produce very limited losses If prices Instead rise. Short calls also gain when stock prices fall but create losses if prices instead rise. Given the scenarios below, what strategy is best given your client's objective? Draw the payoff diagram for each strategy you choose. 1. Performance to date: Up 10%. Client objective: Eam at least 8%. Your forecast: good chance of major market movements, either up or down, between now and end of year. Long straddle. Long bullish spread. Short straddle. 2. Performance to date: Up 10%. Client objective: Earn at least 8%. Your forecast: good chance of a major market decline between now and end of year. Long put options. Short call options. Long call options. 3. Performance to date: Down 10%. Performance of S&P500: Down 12%. Client objective: Beat the S&P500. Your forecast: good chance of major market movements, either up or down, between now and end of year. Long straddle. Long bullish spread. Short straddle. Something else. 4. Performance to date: Down 10%. Performance of S&P500: Down 12%. Client objective: Beat the S&P500. Your forecast: good chance of a major market decline between now and end of year. Long put options. Short call options. Long call options. Something else. Edit View Insert Format Tools Table 12pt v Paragraph B 1 U ALT : O words You are a portfolio manager who uses options positions to customize the risk profile of your clients. You know that a long straddle produces gains if prices move up or down and limited losses if prices do not move. A short straddle produces significant losses if prices move significantly up or down. A bullish spread produces limited gains if prices move up. Long put positions gain when stock prices fall and produce very limited losses If prices Instead rise. Short calls also gain when stock prices fall but create losses if prices instead rise. Given the scenarios below, what strategy is best given your client's objective? Draw the payoff diagram for each strategy you choose. 1. Performance to date: Up 10%. Client objective: Eam at least 8%. Your forecast: good chance of major market movements, either up or down, between now and end of year. Long straddle. Long bullish spread. Short straddle. 2. Performance to date: Up 10%. Client objective: Earn at least 8%. Your forecast: good chance of a major market decline between now and end of year. Long put options. Short call options. Long call options. 3. Performance to date: Down 10%. Performance of S&P500: Down 12%. Client objective: Beat the S&P500. Your forecast: good chance of major market movements, either up or down, between now and end of year. Long straddle. Long bullish spread. Short straddle. Something else. 4. Performance to date: Down 10%. Performance of S&P500: Down 12%. Client objective: Beat the S&P500. Your forecast: good chance of a major market decline between now and end of year. Long put options. Short call options. Long call options. Something else. Edit View Insert Format Tools Table 12pt v Paragraph B 1 U ALT : O words