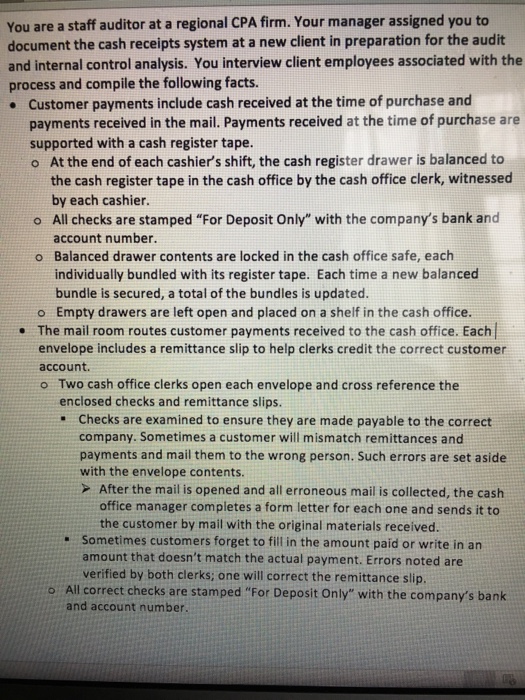

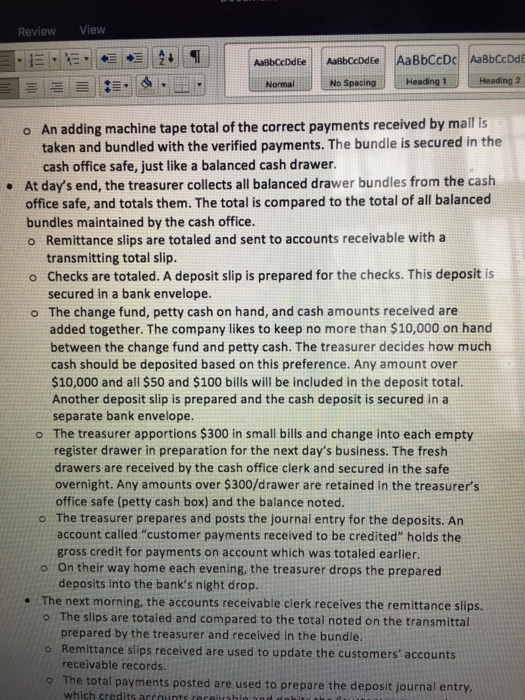

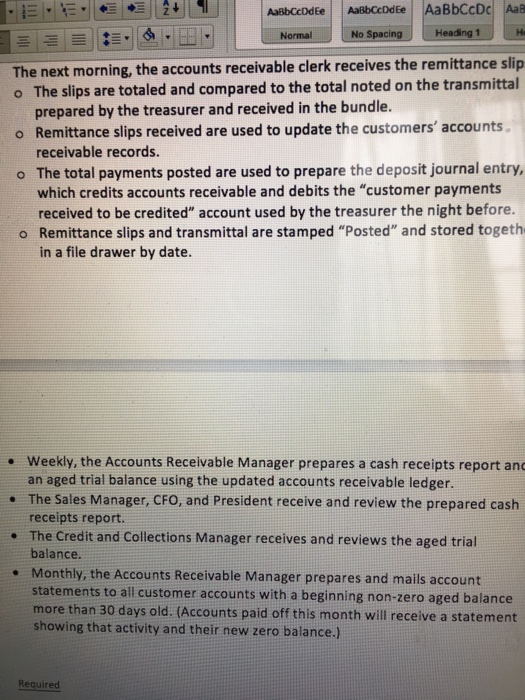

You are a staff auditor at a regional CPA firm. Your manager assigned you to document the cash receipts system at a new client in preparation for the audit and internal control analysis. You interview client employees associated with the process and compile the following facts . Customer payments include cash received at the time of purchase and payments received in the mail. Payments received at the time of purchase are supported with a cash register tape o At the end of each cashier's shift, the cash register drawer is balanced to the cash register tape in the cash office by the cash office clerk, witnessed by each cashier. All checks are stamped "For Deposit Only" with the company's bank and o account number. o Balanced drawer contents are locked in the cash office safe, each individually bundled with its register tape. Each time a new balanced bundle is secured, a total of the bundles is updated. o Empty drawers are left open and placed on a shelf in the cash office . The mail room routes customer payments received to the cash office. Each envelope includes a remittance slip to help clerks credit the correct customer account o Two cash office clerks open each envelope and cross reference the enclosed checks and remittance slips. Checks are examined to ensure they are made payable to the correct company. Sometimes a customer will mismatch remittances and payments and mail them to the wrong person. Such errors are set aside with the envelope contents. After the mail is opened and all erroneous mail is collected, the cash office manager completes a form letter for each one and sends it to the customer by mail with the original materials received. Sometimes customers forget to fill in the amount paid or write in an amount that doesn't match the actual payment. Errors noted are rified by both clerks; one will correct the remittance slip o All correct checks are stamped "For Deposit Only" with the company's bank and account number You are a staff auditor at a regional CPA firm. Your manager assigned you to document the cash receipts system at a new client in preparation for the audit and internal control analysis. You interview client employees associated with the process and compile the following facts . Customer payments include cash received at the time of purchase and payments received in the mail. Payments received at the time of purchase are supported with a cash register tape o At the end of each cashier's shift, the cash register drawer is balanced to the cash register tape in the cash office by the cash office clerk, witnessed by each cashier. All checks are stamped "For Deposit Only" with the company's bank and o account number. o Balanced drawer contents are locked in the cash office safe, each individually bundled with its register tape. Each time a new balanced bundle is secured, a total of the bundles is updated. o Empty drawers are left open and placed on a shelf in the cash office . The mail room routes customer payments received to the cash office. Each envelope includes a remittance slip to help clerks credit the correct customer account o Two cash office clerks open each envelope and cross reference the enclosed checks and remittance slips. Checks are examined to ensure they are made payable to the correct company. Sometimes a customer will mismatch remittances and payments and mail them to the wrong person. Such errors are set aside with the envelope contents. After the mail is opened and all erroneous mail is collected, the cash office manager completes a form letter for each one and sends it to the customer by mail with the original materials received. Sometimes customers forget to fill in the amount paid or write in an amount that doesn't match the actual payment. Errors noted are rified by both clerks; one will correct the remittance slip o All correct checks are stamped "For Deposit Only" with the company's bank and account number