Answered step by step

Verified Expert Solution

Question

1 Approved Answer

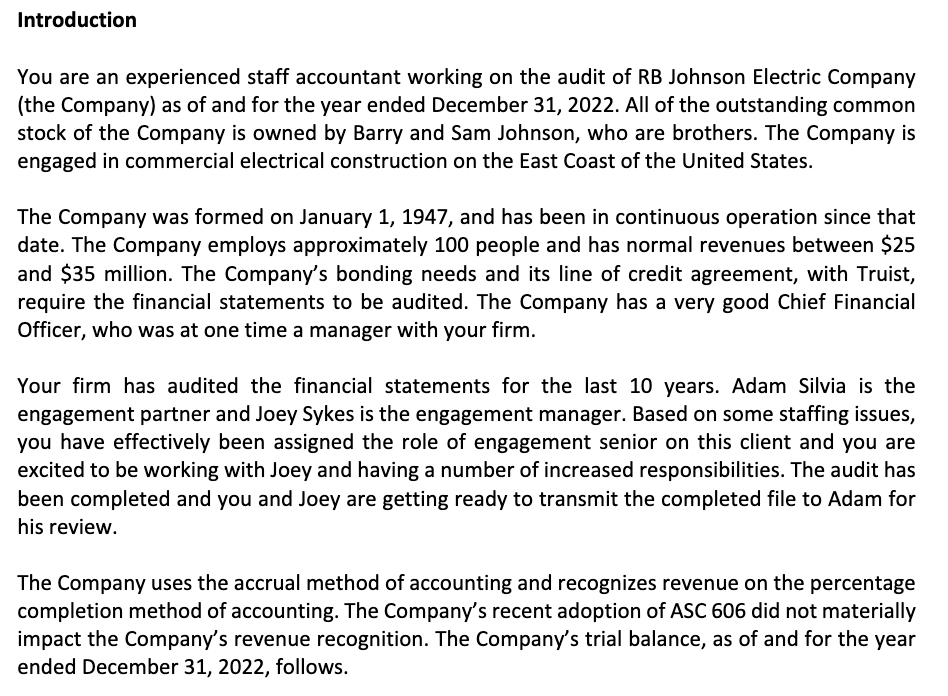

You are an experienced staff accountant working on the audit of RB Johnson Electric Company (the Company) as of and for the year ended December

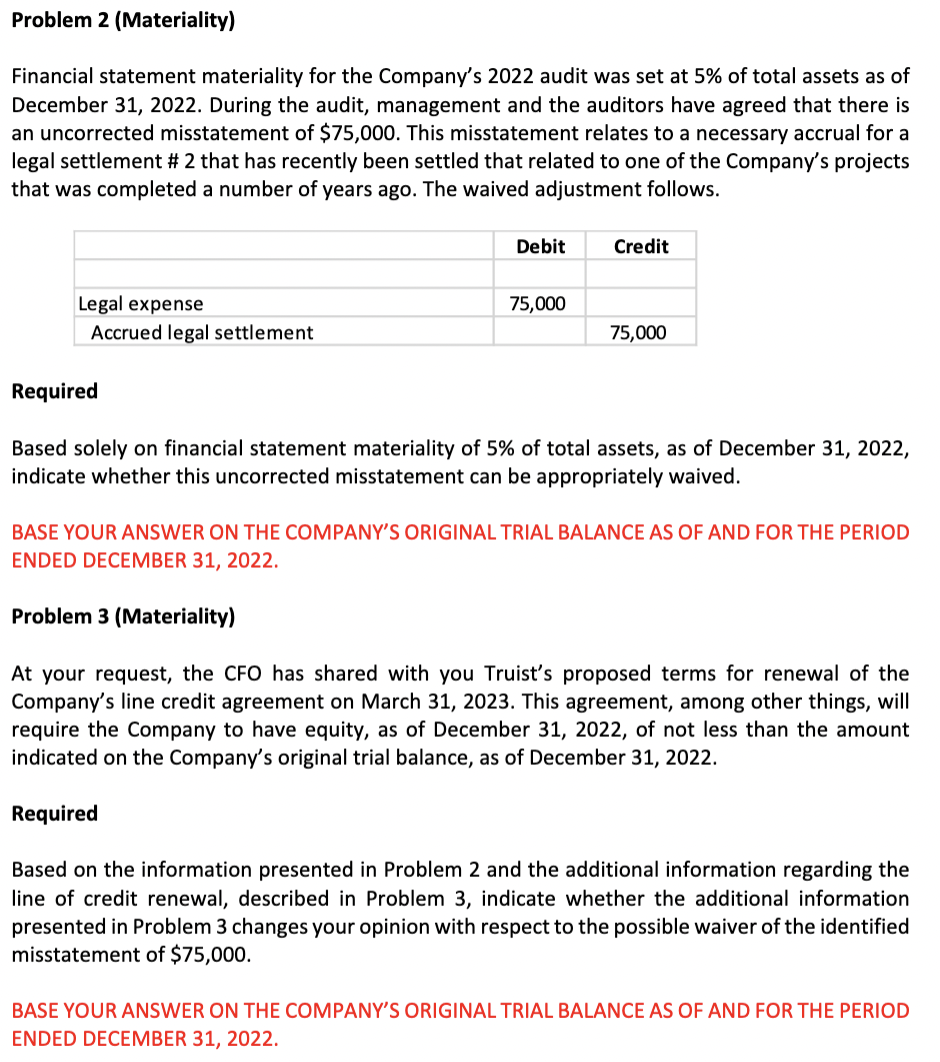

You are an experienced staff accountant working on the audit of RB Johnson Electric Company (the Company) as of and for the year ended December 31, 2022. All of the outstanding common stock of the Company is owned by Barry and Sam Johnson, who are brothers. The Company is engaged in commercial electrical construction on the East Coast of the United States. The Company was formed on January 1, 1947, and has been in continuous operation since that date. The Company employs approximately 100 people and has normal revenues between \$25 and $35 million. The Company's bonding needs and its line of credit agreement, with Truist, require the financial statements to be audited. The Company has a very good Chief Financial Officer, who was at one time a manager with your firm. Your firm has audited the financial statements for the last 10 years. Adam Silvia is the engagement partner and Joey Sykes is the engagement manager. Based on some staffing issues, you have effectively been assigned the role of engagement senior on this client and you are excited to be working with Joey and having a number of increased responsibilities. The audit has been completed and you and Joey are getting ready to transmit the completed file to Adam for his review. The Company uses the accrual method of accounting and recognizes revenue on the percentage completion method of accounting. The Company's recent adoption of ASC 606 did not materially impact the Company's revenue recognition. The Company's trial balance, as of and for the year ended December 31, 2022, follows. Financial statement materiality for the Company's 2022 audit was set at 5% of total assets as of December 31, 2022. During the audit, management and the auditors have agreed that there is an uncorrected misstatement of $75,000. This misstatement relates to a necessary accrual for a legal settlement \# 2 that has recently been settled that related to one of the Company's projects that was completed a number of years ago. The waived adjustment follows. Required Based solely on financial statement materiality of 5% of total assets, as of December 31,2022 , indicate whether this uncorrected misstatement can be appropriately waived. BASE YOUR ANSWER ON THE COMPANY'S ORIGINAL TRIAL BALANCE AS OF AND FOR THE PERIOD ENDED DECEMBER 31, 2022. Problem 3 (Materiality) At your request, the CFO has shared with you Truist's proposed terms for renewal of the Company's line credit agreement on March 31, 2023. This agreement, among other things, will require the Company to have equity, as of December 31, 2022, of not less than the amount indicated on the Company's original trial balance, as of December 31, 2022. Required Based on the information presented in Problem 2 and the additional information regarding the line of credit renewal, described in Problem 3, indicate whether the additional information presented in Problem 3 changes your opinion with respect to the possible waiver of the identified misstatement of $75,000. BASE YOUR ANSWER ON THE COMPANY'S ORIGINAL TRIAL BALANCE AS OF AND FOR THE PERIOD ENDED DECEMBER 31, 2022

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

International Auditing Standards In The United States Comparing And Understanding Standards For ISA And PCAOB

Authors: Asokan Anandarajan

1st Edition

1606496123, 978-1606496121