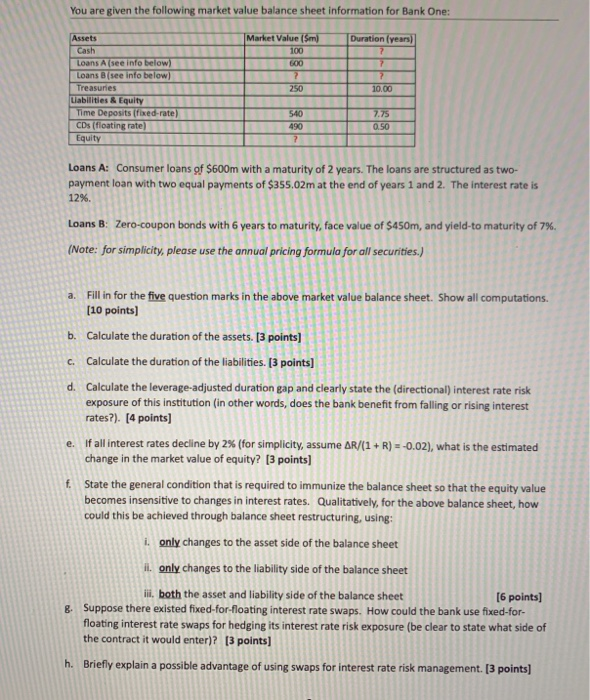

You are given the following market value balance sheet information for Bank One: Assets Cash Loans A (see info below) Loans (see info below) Treasures Liabilities & Equity Time Deposits (fixed-rate) CDs (floating rate) Equity Market Value (Sm 100 600 2 250 Duration (years) 7 7 2 10.00 540 490 7 7.75 0.50 Loans A: Consumer loans of $600m with a maturity of 2 years. The loans are structured as two- payment loan with two equal payments of $355.02m at the end of years 1 and 2. The interest rate is 12%. Loans B: Zero-coupon bonds with 6 years to maturity, face value of $450m, and yield-to maturity of 7%. (Note: for simplicity, please use the annual pricing formula for all securities.) a. Fill in for the five question marks in the above market value balance sheet. Show all computations. [10 points) b. Calculate the duration of the assets. [3 points) c. Calculate the duration of the liabilities. [3 points] d. Calculate the leverage-adjusted duration gap and clearly state the directional) interest rate risk exposure of this institution (in other words, does the bank benefit from falling or rising interest rates?). [4 points) e. If all interest rates decline by 2% (for simplicity, assume AR/(1 + R) = -0.02), what is the estimated change in the market value of equity? (3 points) t. State the general condition that is required to immunize the balance sheet so that the equity value becomes insensitive to changes in interest rates. Qualitatively, for the above balance sheet, how could this be achieved through balance sheet restructuring, using: i. only changes to the asset side of the balance sheet il. only changes to the liability side of the balance sheet ili, both the asset and liability side of the balance sheet [6 points) 8. Suppose there existed fixed-for-floating interest rate swaps. How could the bank use fixed-for- floating interest rate swaps for hedging its interest rate risk exposure (be clear to state what side of the contract it would enter)? (3 points] h. Briefly explain a possible advantage of using swaps for interest rate risk management. [3 points) You are given the following market value balance sheet information for Bank One: Assets Cash Loans A (see info below) Loans (see info below) Treasures Liabilities & Equity Time Deposits (fixed-rate) CDs (floating rate) Equity Market Value (Sm 100 600 2 250 Duration (years) 7 7 2 10.00 540 490 7 7.75 0.50 Loans A: Consumer loans of $600m with a maturity of 2 years. The loans are structured as two- payment loan with two equal payments of $355.02m at the end of years 1 and 2. The interest rate is 12%. Loans B: Zero-coupon bonds with 6 years to maturity, face value of $450m, and yield-to maturity of 7%. (Note: for simplicity, please use the annual pricing formula for all securities.) a. Fill in for the five question marks in the above market value balance sheet. Show all computations. [10 points) b. Calculate the duration of the assets. [3 points) c. Calculate the duration of the liabilities. [3 points] d. Calculate the leverage-adjusted duration gap and clearly state the directional) interest rate risk exposure of this institution (in other words, does the bank benefit from falling or rising interest rates?). [4 points) e. If all interest rates decline by 2% (for simplicity, assume AR/(1 + R) = -0.02), what is the estimated change in the market value of equity? (3 points) t. State the general condition that is required to immunize the balance sheet so that the equity value becomes insensitive to changes in interest rates. Qualitatively, for the above balance sheet, how could this be achieved through balance sheet restructuring, using: i. only changes to the asset side of the balance sheet il. only changes to the liability side of the balance sheet ili, both the asset and liability side of the balance sheet [6 points) 8. Suppose there existed fixed-for-floating interest rate swaps. How could the bank use fixed-for- floating interest rate swaps for hedging its interest rate risk exposure (be clear to state what side of the contract it would enter)? (3 points] h. Briefly explain a possible advantage of using swaps for interest rate risk management. [3 points)