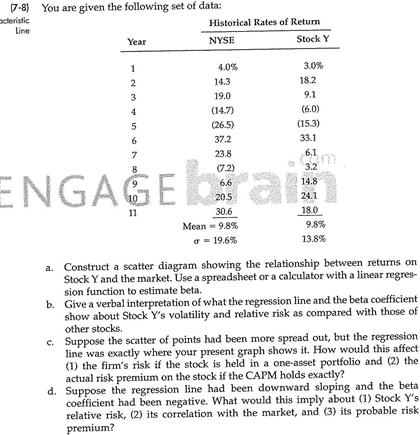

Question: You are given the following set of data; Construct a scatter diagram showing the relationship between returns on Stock Y and the market. Use a

You are given the following set of data; Construct a scatter diagram showing the relationship between returns on Stock Y and the market. Use a spreadsheet or a calculator with a linear regression function to estimate beta. Give a verbal interpretation of what the regression line and the beta coefficient show about Stock Y's volatility and relative risk as compared with those of other stocks. Suppose the scatter of points had been more spread out, but the regression line was exactly where your present graph shows it. How would this affect (1) the firm's risk if the stock is held in a one-asset portfolio and (2) the actual risk premium on the stock if the CAPM holds exactly? Suppose the regression line had been downward sloping and the beta coefficient had been negative. What would this imply about (1) Stock Y's relative risk, (2) its correlation with the market, and (3) its probable risk premium? You are given the following set of data; Construct a scatter diagram showing the relationship between returns on Stock Y and the market. Use a spreadsheet or a calculator with a linear regression function to estimate beta. Give a verbal interpretation of what the regression line and the beta coefficient show about Stock Y's volatility and relative risk as compared with those of other stocks. Suppose the scatter of points had been more spread out, but the regression line was exactly where your present graph shows it. How would this affect (1) the firm's risk if the stock is held in a one-asset portfolio and (2) the actual risk premium on the stock if the CAPM holds exactly? Suppose the regression line had been downward sloping and the beta coefficient had been negative. What would this imply about (1) Stock Y's relative risk, (2) its correlation with the market, and (3) its probable risk premium

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts