Answered step by step

Verified Expert Solution

Question

1 Approved Answer

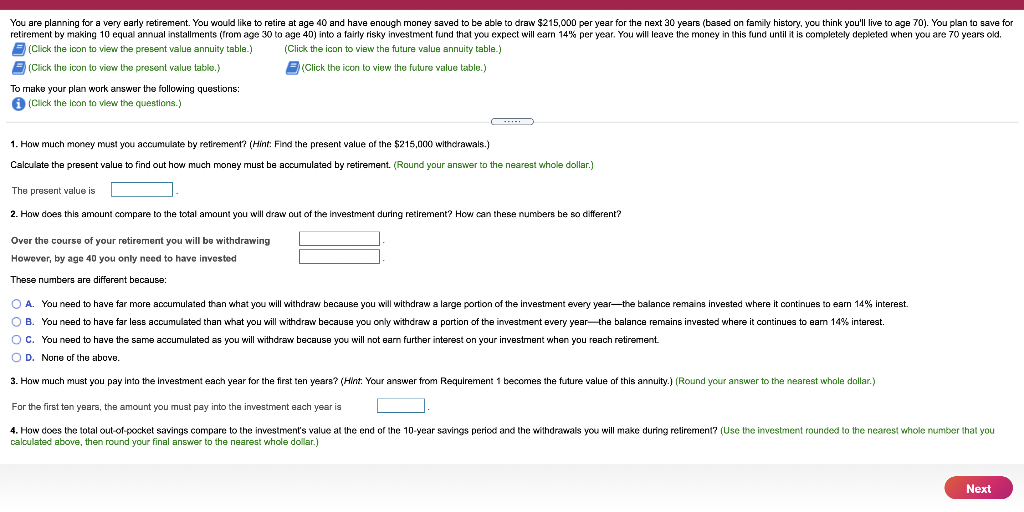

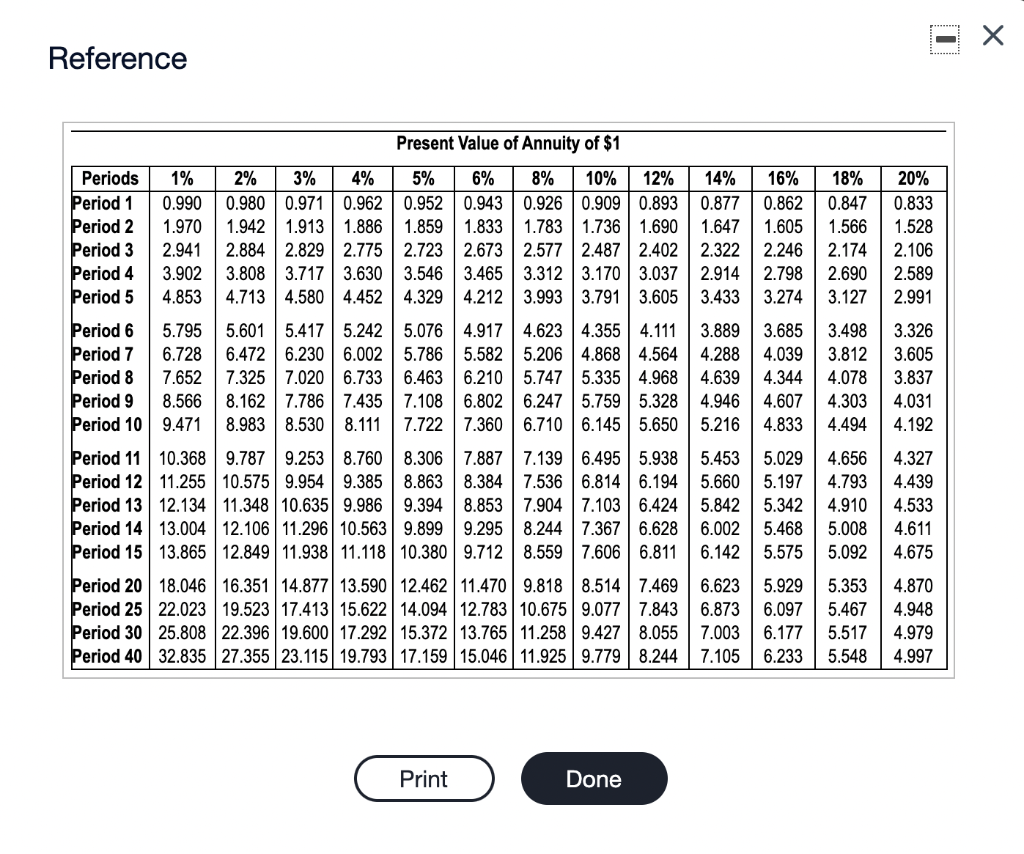

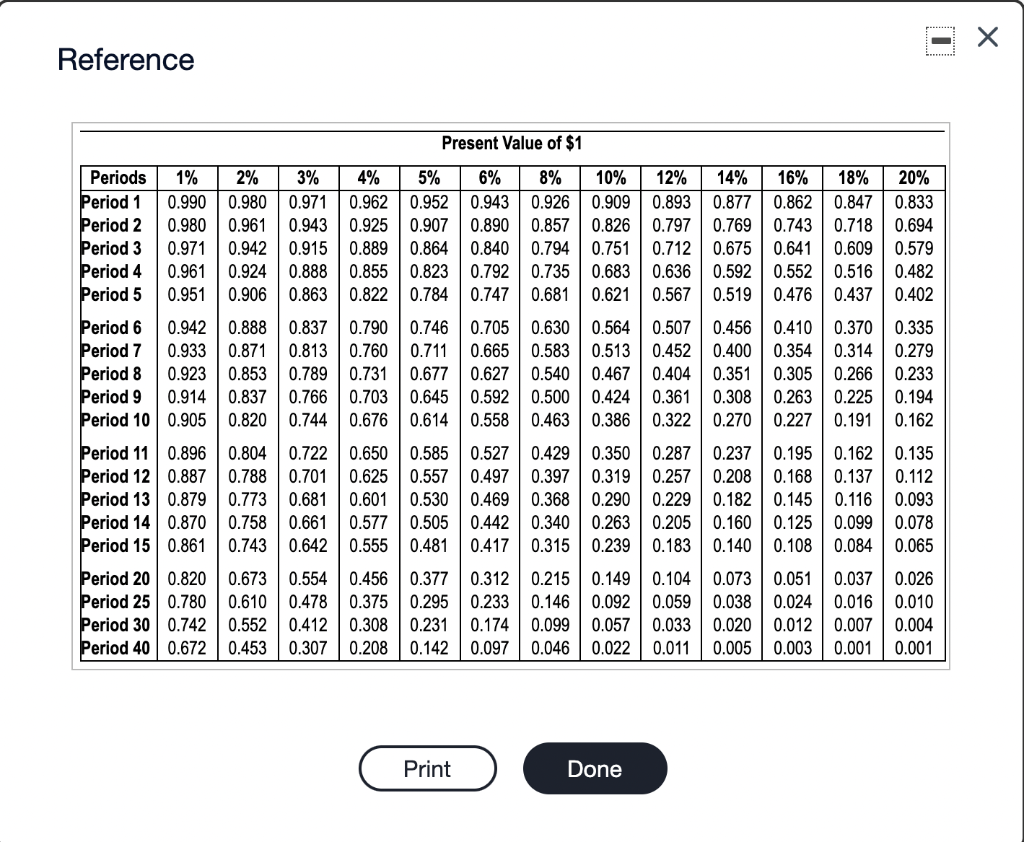

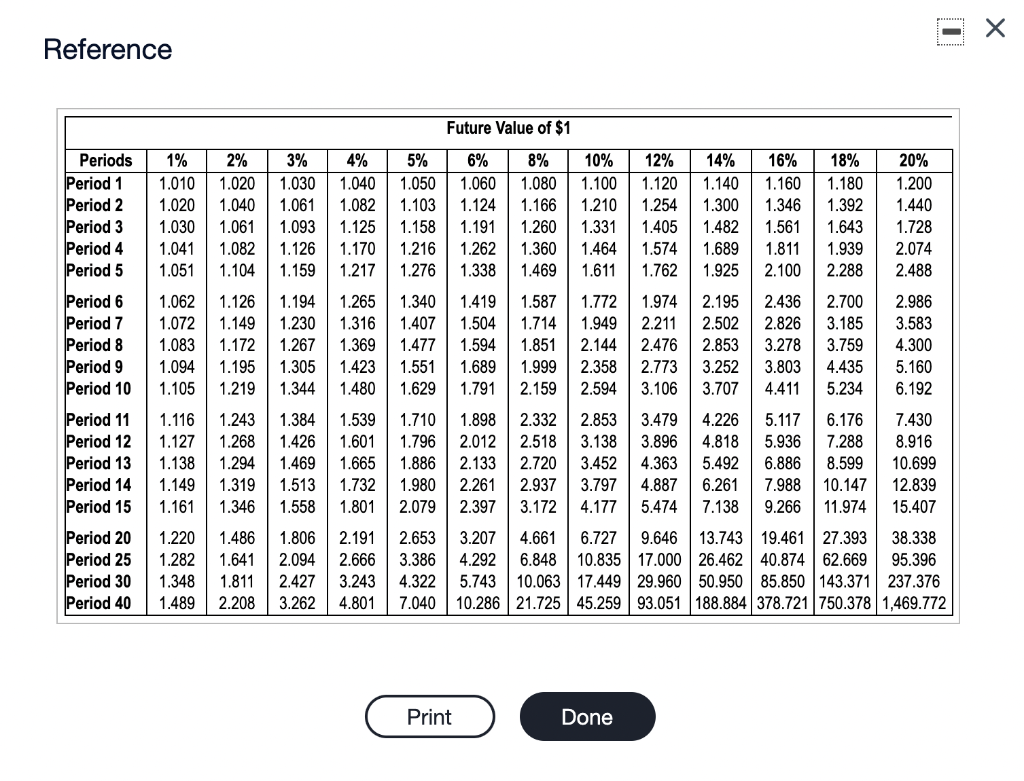

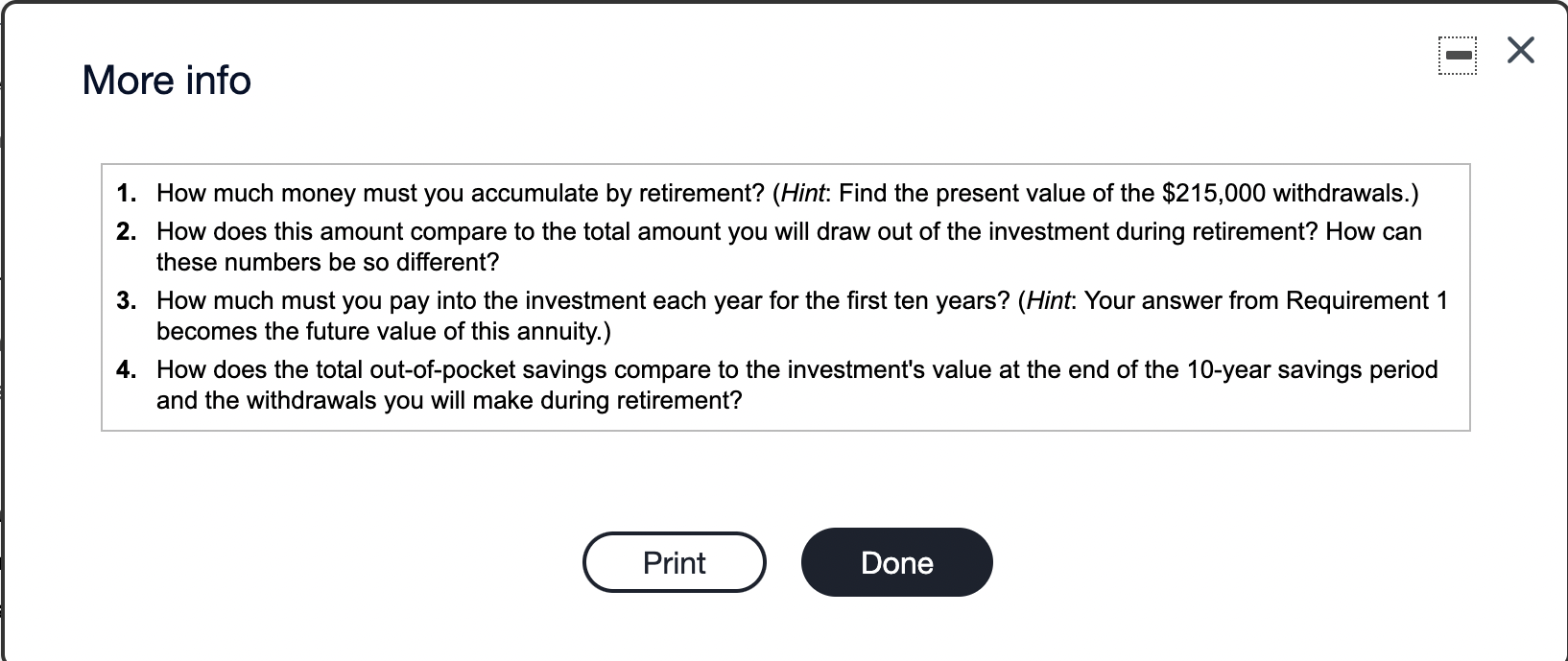

You are planning for a very early retirement. You would like to retire at age 40 and have enough money saved to be able to

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Accounting For Governments From Budget To Audit How Governments Plan Raise Spend And Then Account For Their Use Of Citizens Money In The 21st Century

Authors: Michael Parry, Jesse Hughes

1st Edition

1092763112, 978-1092763110