Answered step by step

Verified Expert Solution

Question

1 Approved Answer

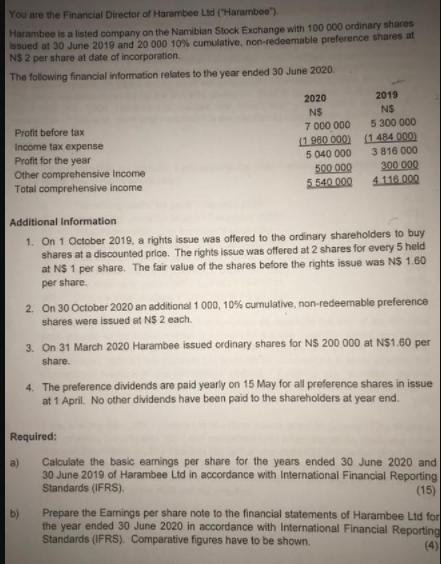

You are the Financial Director of Harambee Ltd (Haramboo) Harambee is a listed company on the Namibian Stock Exchange with 100 000 ordinary shares

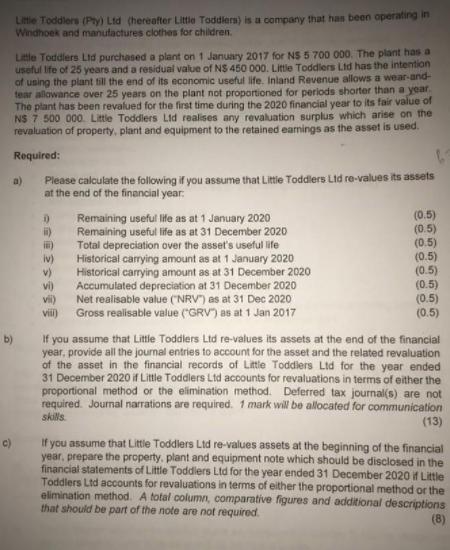

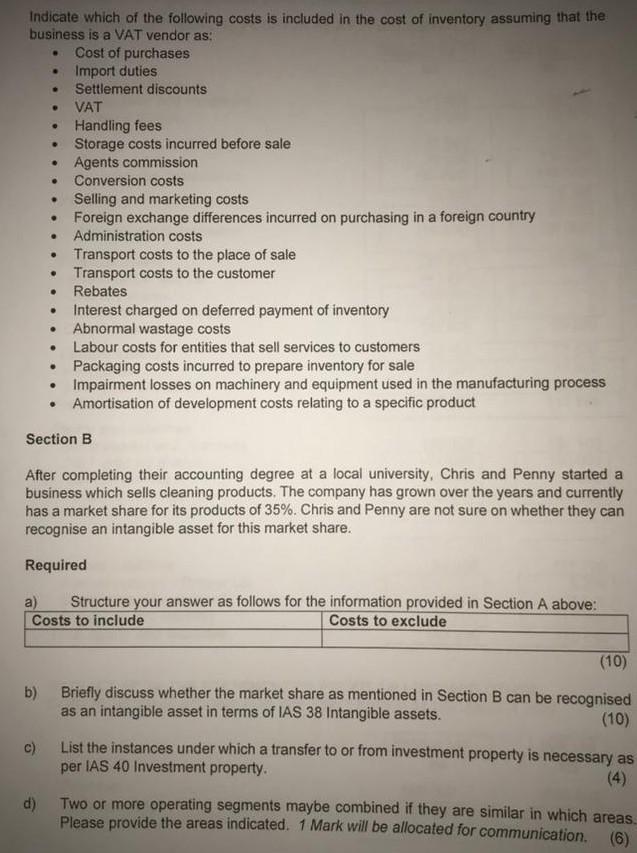

You are the Financial Director of Harambee Ltd ("Haramboo) Harambee is a listed company on the Namibian Stock Exchange with 100 000 ordinary shares issued at 30 June 2019 and 20 000 10% cumulative, non-redeemable preference shares at N$ 2 per share at date of incorporation The following financial information relates to the year ended 30 June 2020. Profit before tax Income tax expense Profit for the year Other comprehensive Income Total comprehensive income a) 2020 NS 7 000 000 (1.980 000) 5 040 000 Additional Information 1. On 1 October 2019, a rights issue was offered to the ordinary shareholders to buy shares at a discounted price. The rights issue was offered at 2 shares for every 5 held at N$ 1 per share. The fair value of the shares before the rights issue was N$ 1.60 per share. b) 500 000 5.540 000 Required: 2019 NS 5 300 000 (1.484.000) 3 816 000 300 000 4.116.000 2. On 30 October 2020 an additional 1 000, 10% cumulative, non-redeemable preference shares were issued at NS 2 each. 3. On 31 March 2020 Harambee issued ordinary shares for NS 200 000 at N$1.60 per share. 4. The preference dividends are paid yearly on 15 May for all preference shares in issue at 1 April. No other dividends have been paid to the shareholders at year end. Calculate the basic earnings per share for the years ended 30 June 2020 and 30 June 2019 of Harambee Ltd in accordance with International Financial Reporting Standards (IFRS). (15) Prepare the Earnings per share note to the financial statements of Harambee Ltd for the year ended 30 June 2020 in accordance with International Financial Reporting Standards (IFRS). Comparative figures have to be shown. (4) c) Little Toddlers (Pty) Ltd (hereafter Little Toddlers) is a company that has been operating in Windhoek and manufactures clothes for children. Little Toddlers Ltd purchased a plant on 1 January 2017 for NS 5 700 000. The plant has a useful life of 25 years and a residual value of N$ 450 000. Little Toddlers Ltd has the intention of using the plant till the end of its economic useful life. Inland Revenue allows a wear-and- tear allowance over 25 years on the plant not proportioned for periods shorter than a year. The plant has been revalued for the first time during the 2020 financial year to its fair value of NS 7 500 000. Little Toddlers Ltd realises any revaluation surplus which arise on the revaluation of property, plant and equipment to the retained eamings as the asset is used. Required: b) a) 6 Please calculate the following if you assume that Little Toddlers Ltd re-values its assets at the end of the financial year: D) ii) ii) (iv) v) vi) vii) viii) Remaining useful life as at 1 January 2020 Remaining useful life as at 31 December 2020 Total depreciation over the asset's useful life Historical carrying amount as at 1 January 2020 Historical carrying amount as at 31 December 2020 Accumulated depreciation at 31 December 2020 Net realisable value (NRV") as at 31 Dec 2020 Gross realisable value ("GRV) as at 1 Jan 2017 (0.5) (0.5) (0.5) (0.5) (0.5) (0.5) (0.5) (0.5) If you assume that Little Toddlers Ltd re-values its assets at the end of the financial year, provide all the journal entries to account for the asset and the related revaluation of the asset in the financial records of Little Toddlers Ltd for the year ended 31 December 2020 if Little Toddlers Ltd accounts for revaluations in terms of either the proportional method or the elimination method. Deferred tax journal(s) are not required. Journal narrations are required. 1 mark will be allocated for communication skills. (13) If you assume that Little Toddlers Ltd re-values assets at the beginning of the financial year, prepare the property, plant and equipment note which should be disclosed in the financial statements of Little Toddlers Ltd for the year ended 31 December 2020 if Little Toddlers Ltd accounts for revaluations in terms of either the proportional method or the elimination method. A total column, comparative figures and additional descriptions that should be part of the note are not required. (8) Indicate which of the following costs is included in the cost of inventory assuming that the business is a VAT vendor as: Cost of purchases Import duties . . c) . d) . Conversion costs . Selling and marketing costs Foreign exchange differences incurred on purchasing in a foreign country . . . Rebates Interest charged on deferred payment of inventory Abnormal wastage costs Labour costs for entities that sell services to customers Settlement discounts VAT Handling fees Storage costs incurred before sale Agents commission . Administration costs Transport costs to the place of sale Transport costs to the customer Section B Packaging costs incurred to prepare inventory for sale Impairment losses on machinery and equipment used in the manufacturing process Amortisation of development costs relating to a specific product After completing their accounting degree at a local university, Chris and Penny started a business which sells cleaning products. The company has grown over the years and currently has a market share for its products of 35%. Chris and Penny are not sure on whether they can recognise an intangible asset for this market share. Required a) Structure your answer as follows for the information provided in Section A above: Costs to include Costs to exclude (10) b) Briefly discuss whether the market share as mentioned in Section B can be recognised as an intangible asset in terms of IAS 38 Intangible assets. (10) List the instances under which a transfer to or from investment property is necessary as per IAS 40 Investment property. Two or more operating segments maybe combined if they are similar in which areas. Please provide the areas indicated. 1 Mark will be allocated for communication. (6)

Step by Step Solution

★★★★★

3.54 Rating (161 Votes )

There are 3 Steps involved in it

Step: 1

Answer Question 1 Calculation of Earnings Per Share EPS for Harambee Ltd Year Ended 30 June 2020 Profit for the Year N5040000 Weighted Average Ordinary Shares Outstanding Ordinary Shares as of 30 June ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Transport Operations

Authors: Allen Stuart

2nd Edition

978-0470115398, 0470115394