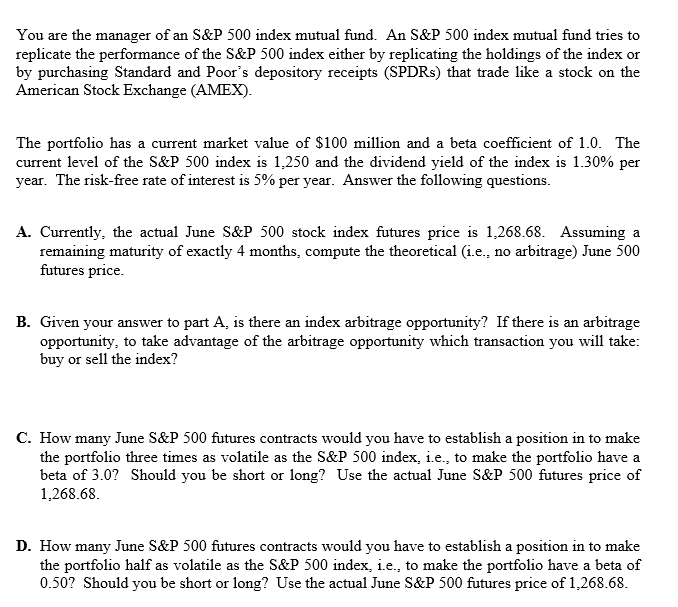

You are the manager of an S&P500 index mutual fund. An S\&P 500 index mutual fund tries to replicate the performance of the S\&P 500 index either by replicating the holdings of the index or by purchasing Standard and Poor's depository receipts (SPDRs) that trade like a stock on the American Stock Exchange (AMEX). The portfolio has a current market value of $100 million and a beta coefficient of 1.0. The current level of the S\&P 500 index is 1,250 and the dividend yield of the index is 1.30% per year. The risk-free rate of interest is 5% per year. Answer the following questions. A. Currently, the actual June S\&P 500 stock index futures price is 1,268.68. Assuming a remaining maturity of exactly 4 months, compute the theoretical (i.e., no arbitrage) June 500 futures price. B. Given your answer to part A, is there an index arbitrage opportunity? If there is an arbitrage opportunity, to take advantage of the arbitrage opportunity which transaction you will take: buy or sell the index? C. How many June S\&P 500 futures contracts would you have to establish a position in to make the portfolio three times as volatile as the S\&P 500 index, i.e., to make the portfolio have a beta of 3.0 ? Should you be short or long? Use the actual June S\&P 500 futures price of 1,268.68 D. How many June S\&P 500 futures contracts would you have to establish a position in to make the portfolio half as volatile as the S\&P 500 index, i.e., to make the portfolio have a beta of 0.50 ? Should you be short or long? Use the actual June S\&P 500 futures price of 1,268.68. You are the manager of an S&P500 index mutual fund. An S\&P 500 index mutual fund tries to replicate the performance of the S\&P 500 index either by replicating the holdings of the index or by purchasing Standard and Poor's depository receipts (SPDRs) that trade like a stock on the American Stock Exchange (AMEX). The portfolio has a current market value of $100 million and a beta coefficient of 1.0. The current level of the S\&P 500 index is 1,250 and the dividend yield of the index is 1.30% per year. The risk-free rate of interest is 5% per year. Answer the following questions. A. Currently, the actual June S\&P 500 stock index futures price is 1,268.68. Assuming a remaining maturity of exactly 4 months, compute the theoretical (i.e., no arbitrage) June 500 futures price. B. Given your answer to part A, is there an index arbitrage opportunity? If there is an arbitrage opportunity, to take advantage of the arbitrage opportunity which transaction you will take: buy or sell the index? C. How many June S\&P 500 futures contracts would you have to establish a position in to make the portfolio three times as volatile as the S\&P 500 index, i.e., to make the portfolio have a beta of 3.0 ? Should you be short or long? Use the actual June S\&P 500 futures price of 1,268.68 D. How many June S\&P 500 futures contracts would you have to establish a position in to make the portfolio half as volatile as the S\&P 500 index, i.e., to make the portfolio have a beta of 0.50 ? Should you be short or long? Use the actual June S\&P 500 futures price of 1,268.68