Question

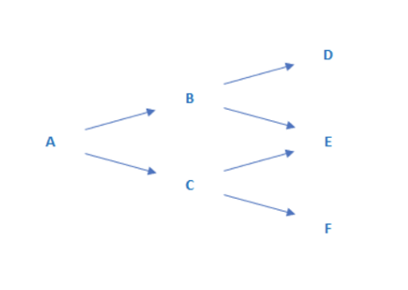

You are using the binomial tree model (drawn and labelled below) to price a 6-month European option on a stock that is currently trading at

You are using the binomial tree model (drawn and labelled below) to price a 6-month European option on a stock that is currently trading at $20. The risk-free interest rate is 2% p.a.c.c. The option values at nodes D and E are 2.25 and 0, respectively; the stock price at node B is $25.

A): Is this a call or a put? (1 mark)

B): Calculate the remaining stock prices and option values that correspond to every node on the tree. Complete working process must be shown for marks. (10 marks)

C): If the option is instead on a futures contract, identify the adjustment you need to make in part (b). (1 mark)

D D

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Using Microcomputers In Managerial Accounting

Authors: George Hildebrand

1st Edition

0938188275, 978-0938188278