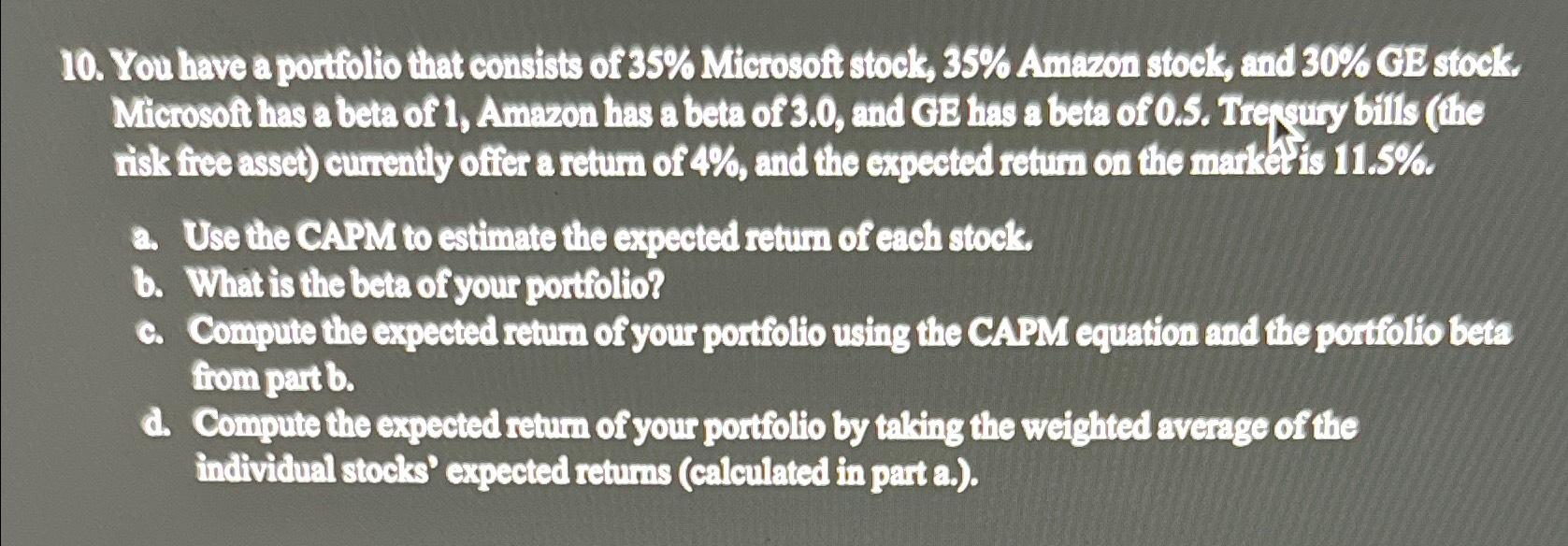

Question

You have a portiolio that consists of 35% Microsoft stock, 35% Amaron stock, and 30% GE stock Merosot has a beta of 1, Amazon has

You have a portiolio that consists of

35%Microsoft stock,

35%Amaron stock, and

30%GE stock Merosot has a beta of 1, Amazon has a beta of 3.0, and GB has a beta of O.5. Treggury bills (the risk free asset) currently ofier a return of

4%, and the expected retum on the mark it is

11.5%.\ a. Use the CAPM to estimate the expected retum of each stock\ b. What is the beta of your portiolio?\ c. Compute the expected return of your portiolio using the CAPM equation and the portifitio beta from partb.\ a. Compute the expected retum of your portiflio by taking the weighted average of the individual stocks' expected returns (calculated in part a.).

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Advanced Finance Theories

Authors: Ser-Huang Poon

1st Edition

9814460370, 978-9814460378