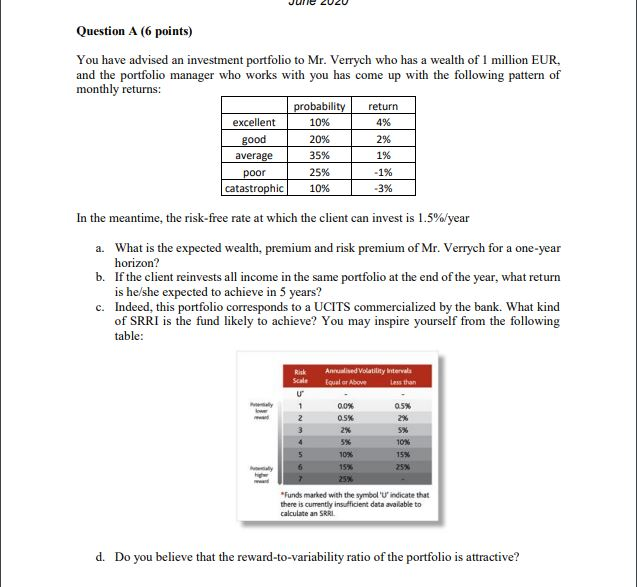

Question

You have advised an investment portfolio to Mr. Verrych who has a wealth of 1 million EUR, and the portfolio manager who works with you

You have advised an investment portfolio to Mr. Verrych who has a wealth of 1 million EUR, and the portfolio manager who works with you has come up with the following pattern of monthly returns:

In the meantime, the risk-free rate at which the client can invest is 1.5%/year

a. What is the expected wealth, premium and risk premium of Mr. Verrych for a one-year horizon?

b. If the client reinvests all income in the same portfolio at the end of the year, what return is he/she expected to achieve in 5 years?

c. Indeed, this portfolio corresponds to a UCITS commercialized by the bank. What kind of SRRI is the fund likely to achieve? You may inspire yourself from the following table:

d. Do you believe that the reward-to-variability ratio of the portfolio is attractive?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

IRS Audit Protection And Survival Guide Bars And Restaurants

Authors: Gerald F. Bernard, Daniel J. Baran

1st Edition

0471166375, 978-0471166375