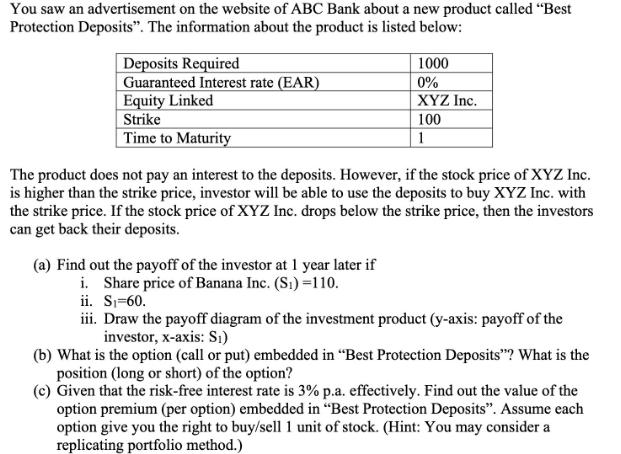

You saw an advertisement on the website of ABC Bank about a new product called Best Protection Deposits. The information about the product is

You saw an advertisement on the website of ABC Bank about a new product called "Best Protection Deposits". The information about the product is listed below: Deposits Required Guaranteed Interest rate (EAR) Equity Linked Strike Time to Maturity 1000 0% XYZ Inc. 100 1 The product does not pay an interest to the deposits. However, if the stock price of XYZ Inc. is higher than the strike price, investor will be able to use the deposits to buy XYZ Inc. with the strike price. If the stock price of XYZ Inc. drops below the strike price, then the investors can get back their deposits. (a) Find out the payoff of the investor at 1 year later if i. Share price of Banana Inc. (S) =110. ii. S-60. iii. Draw the payoff diagram of the investment product (y-axis: payoff of the investor, x-axis: S) (b) What is the option (call or put) embedded in "Best Protection Deposits"? What is the position (long or short) of the option? (c) Given that the risk-free interest rate is 3% p.a. effectively. Find out the value of the option premium (per option) embedded in "Best Protection Deposits". Assume each option give you the right to buy/sell 1 unit of stock. (Hint: You may consider a replicating portfolio method.)

Step by Step Solution

3.36 Rating (165 Votes )

There are 3 Steps involved in it

Step: 1

a i If S1110 the investor can use the deposits to buy XYZ Inc with the strike price of 100 and then ...

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Authors: Gerald E. Whittenburg, Martha Altus Buller, Steven L Gill

31st Edition

1111972516, 978-1285586618, 1285586611, 978-1285613109, 978-1111972516