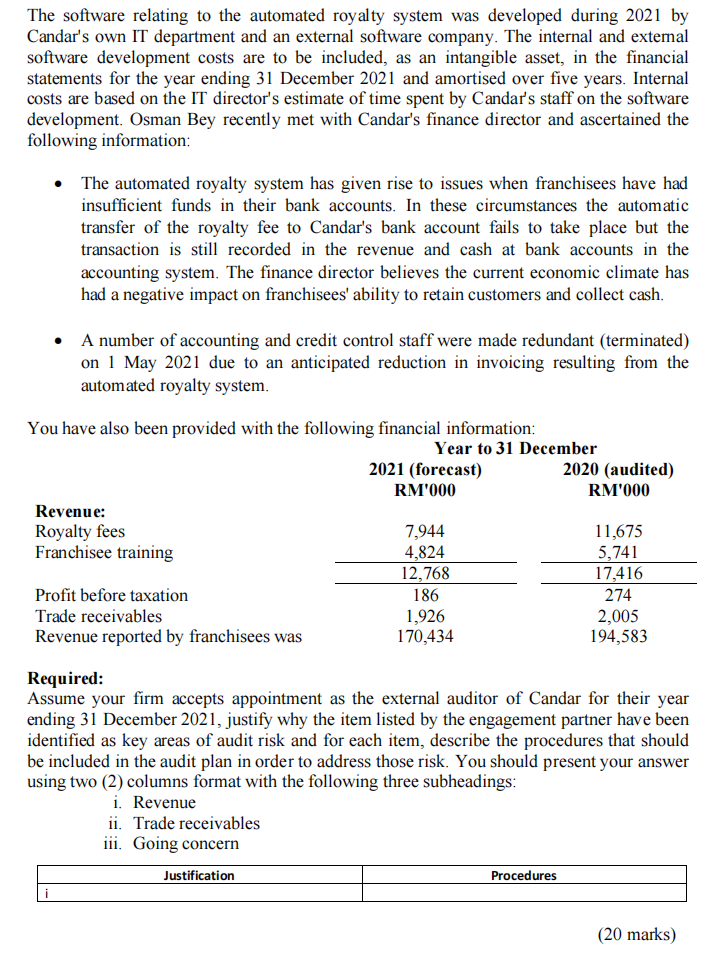

Your firm has recently been approached by the directors of Candar Berhad (Candar) to accept appointment as its external auditor for the year ending 31 December 2021. Osman Bey, the partner responsible for considering whether your firm should accept the engagement, has requested that you help him by considering the following key areas of audit risk as part of your firm's preliminary risk assessment: (1) Revenue (2) Trade receivables (3) Intangible assets software development costs The principal activity of Candar is the provision of professional cleaning services, through UK franchise operators (franchisees), to commercial customers who operate from retail and office premises. Candar earns revenue from franchisees through: royalty fees based upon a percentage of each franchisee's revenue during the term of the franchise agreement; and charges made for the provision of training to franchisees and their staff. Royalty fees are received by Candar each month and range from 4% to 8% of franchisee revenue depending on the franchise agreement. Until 30 April 2021, each franchisee reported its monthly revenue to Candar's accounts department which prepared an invoice for the royalty fee due. On 1 May 2021 Candar implemented an automated royalty system integrated with each franchisee's accounting system to improve the collection days. The monthly revenue of each franchisee is automatically transmitted to Candar's royalty system which calculates the royalty fee due. The royalty system then notifies each franchisee's bank of the amount due and the cash is automatically transferred to Candar's bank account on the same day. The accounts department no longer prepares invoices in respect of royalty payments. The royalty system is integrated with Candar's accounting system which records the royalty fees in the revenue and cash at bank accounts when the franchisee's bank is notified of the amount due. Invoices for training are prepared manually on completion of the training. The amount invoiced is based on the total number of hours spent on training by Candar's instructors and standard hourly rates, which vary according to the level of training provided. Instructors record their time against a unique franchisee code on a weekly timesheet. Timesheets are emailed by instructors to Candar's training sales team who record the hours of training provided against each unique franchisee code in the sales system. Each instructor informs the accounts department, by email, when the training is complete. The accounts department then prepares an invoice for the training based on the records maintained by the training sales team. No checks for the completeness of timesheets or the accuracy of invoices are carried out. Any hours recorded but not invoiced at 31 December are recognised in the year-end financial statements as accrued income. The software relating to the automated royalty system was developed during 2021 by Candar's own IT department and an external software company. The internal and external software development costs are to be included, as an intangible asset, in the financial statements for the year ending 31 December 2021 and amortised over five years. Internal costs are based on the IT director's estimate of time spent by Candar's staff on the software development. Osman Bey recently met with Candar's finance director and ascertained the following information: The automated royalty system has given rise to issues when franchisees have had insufficient funds in their bank accounts. In these circumstances the automatic transfer of the royalty fee to Candar's bank account fails to take place but the transaction is still recorded in the revenue and cash at bank accounts in the accounting system. The finance director believes the current economic climate has had a negative impact on franchisees' ability to retain customers and collect cash. A number of accounting and credit control staff were made redundant (terminated) on 1 May 2021 due to an anticipated reduction in invoicing resulting from the automated royalty system. You have also been provided with the following financial information: Year to 31 December 2021 (forecast) 2020 (audited) RM'000 RM'000 Revenue: Royalty fees 7,944 11,675 Franchisee training 4,824 5,741 12,768 17,416 Profit before taxation 186 274 Trade receivables 1,926 2,005 Revenue reported by franchisees was 170,434 194,583 Required: Assume your firm accepts appointment as the external auditor of Candar for their year ending 31 December 2021, justify why the item listed by the engagement partner have been identified as key areas of audit risk and for each item, describe the procedures that should be included in the audit plan in order to address those risk. You should present your answer using two (2) columns format with the following three subheadings: i. Revenue ii. Trade receivables iii. Going concern Justification Procedures i (20 marks)