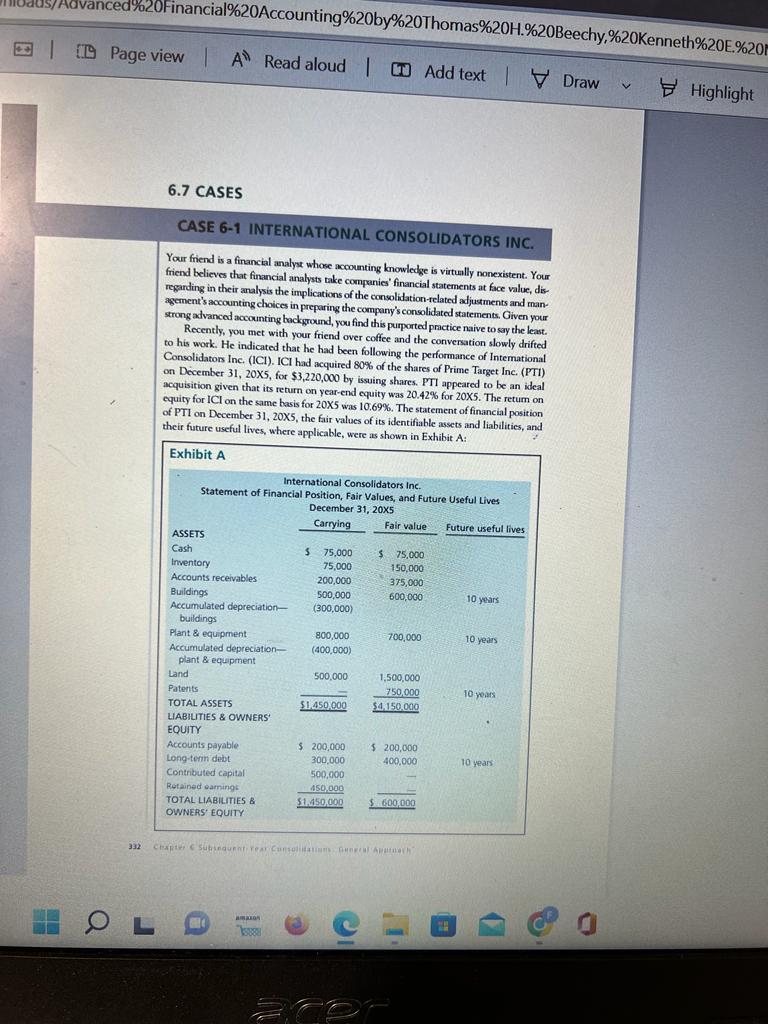

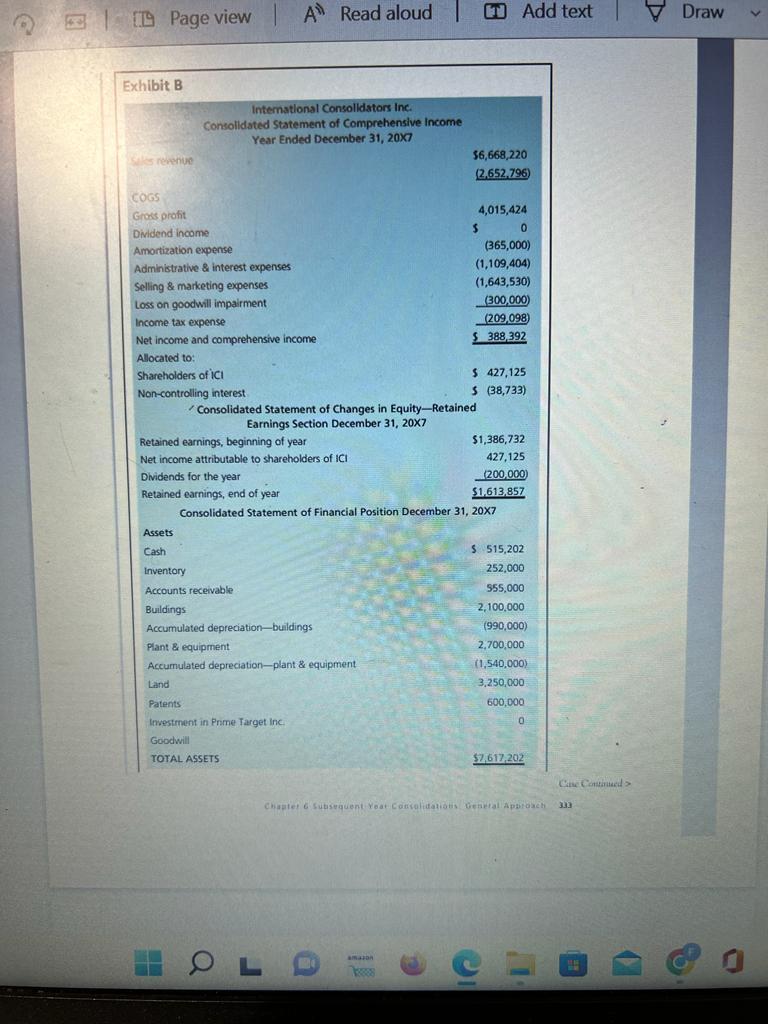

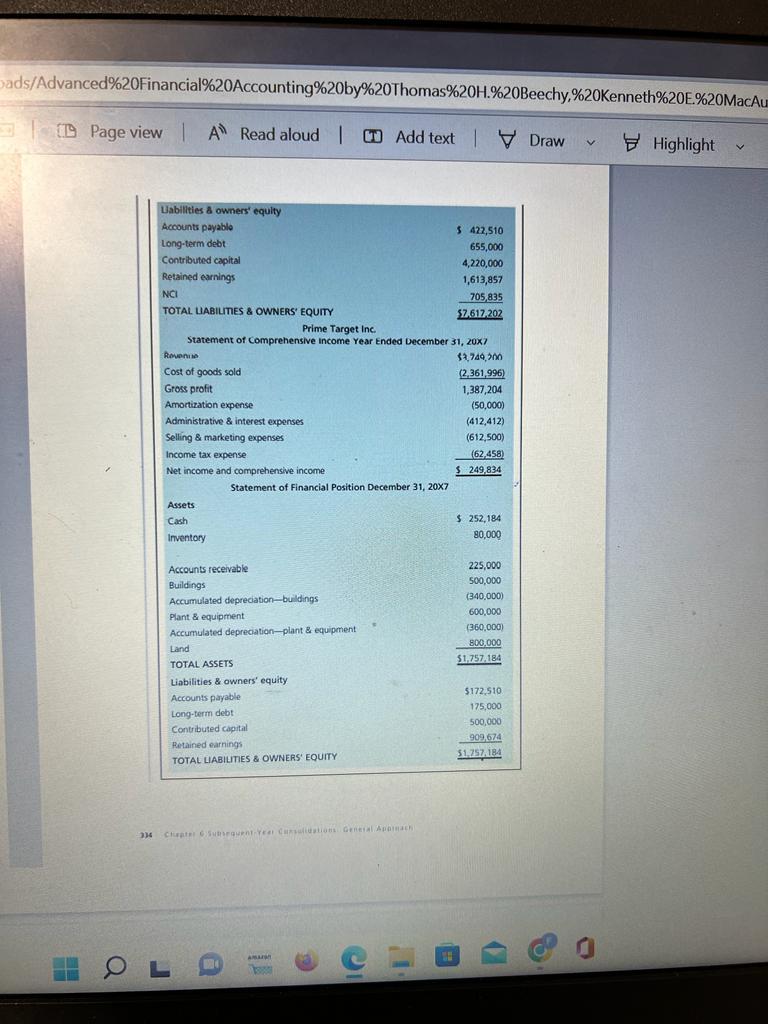

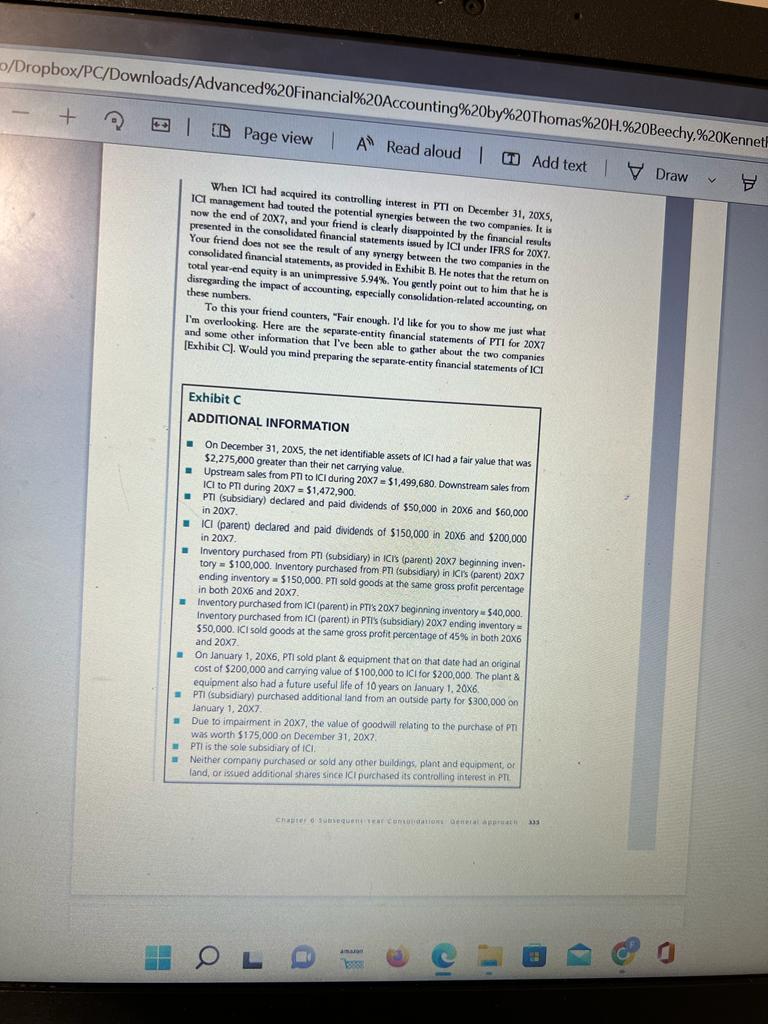

Your friend is a financial analys whose accounting knowledge is virtually nonexistent. Your friend believes that financial analysts take companies' financial statements at face value, disregarding in their analysis the implications of the consolidation-related adjustments and management's accounting choices in preparing the company's consolidated statements. Given your strong advanced accounting background, you find this purported practice naive to say the least. Recently, you met with your friend over coffee and the conversation slowly drifted to his work. He indicated that he had been following the performance of Intemational Consolidators Inc. (ICI). ICI had acquired 80% of the shares of Prime Target Inc. (PTI) on December 31,205, for $3,220,000 by issuing shares. PTI appeared to be an ideal acquisition given that its return on year-end equity was 20.42% for 205. The return on equity for ICl on the same basis for 205 was 10.69%. The statement of financial position of PTI on December 31, 20X5, the fair values of its identifiable assets and liabilities, and their future useful lives, where applicable, were as shown in Exhibit A: Exhibit B Intemational Consolidators inc. Consolidated Statement of Comprehensive income Year Ended December 31, 20X7 1) 10 When ICl had acquired its controlling interest in PT on December 31,205, ICl management had touted the potential synergies between the two companies. It is now the end of 207, and your friend is clearly disappointed by the financial resules Your friend does not see the reselt of atatements issued by ICl under IFRS for 20X7. consolidated financial statements, as provided synergy between the two companies in the total year-end equity is an unimpressive 5.940. You these numbers. To this your friend counters, "Fair enough. I'd like for you to show me just what I'm overlooking. Here are the separate-entity funancial statements of PTI for 20X7 and some other information that l've been able to gather about the two companies [Exhibit C]. Would you mind preparing the separate-entity financial statements of ICl Exhibit C ADDITIONAL INFORMATION On December 31, 20X5, the net identifiable assets of ICI had a fair yalue that was $2,275,000 greater than their net carrying value. Upstream sales from PTI to ICI during 207=$1,499,680. Downstream sales from ICl to PTI during 207=51,472,900. PTI (subsidiary) declared and paid dividends of $50,000 in 206 and $60,000 in 207. E ICl (parent) declared and paid dividends of $150,000 in 206 and $200,000 in 207. = Inventory purchased from PTI (subsidiary) in IC/'s (parent) 207 beginning inven. tory =5100,000. Inventory purchased from. PT (subsidiary) in ICls (parent) 207 ending inventory =$150,000. PTI sold goods at the same gross profit percentage in both 206 and 207. Inventory purchased from ICI (parent) in PTIs 207 beginning inventory =540,000. Inventory purchased from iCl (parent) in PTI's (subsidiary) 207 ending inventory = $50,000. ICI sold goods at the same gross profit percentage of 45% in both 206 and 207. - On January 1,206, Phi sold plant \& equipment that on that date had an original cost of $200,000 and carrying value of $100,000 to ICl for $200,000. The plant & equipment also had a future useful life of 10 years on lanuary 1,206. PTI (subsidiary) purchased additional fand from an outside party for $300,000 on Jansary 1, 20x7. Due to impairment in 207, the value of goodwill relating to the purchase of PI was worth 5175,000 on December 31,207. PII is the sole subsidrary of ICI. a Neither company purchased or sold any other buildings, plant and equipment, or land, of issued additional shares since ICI purchasedt its controlling interest in PI?. Your friend is a financial analys whose accounting knowledge is virtually nonexistent. Your friend believes that financial analysts take companies' financial statements at face value, disregarding in their analysis the implications of the consolidation-related adjustments and management's accounting choices in preparing the company's consolidated statements. Given your strong advanced accounting background, you find this purported practice naive to say the least. Recently, you met with your friend over coffee and the conversation slowly drifted to his work. He indicated that he had been following the performance of Intemational Consolidators Inc. (ICI). ICI had acquired 80% of the shares of Prime Target Inc. (PTI) on December 31,205, for $3,220,000 by issuing shares. PTI appeared to be an ideal acquisition given that its return on year-end equity was 20.42% for 205. The return on equity for ICl on the same basis for 205 was 10.69%. The statement of financial position of PTI on December 31, 20X5, the fair values of its identifiable assets and liabilities, and their future useful lives, where applicable, were as shown in Exhibit A: Exhibit B Intemational Consolidators inc. Consolidated Statement of Comprehensive income Year Ended December 31, 20X7 1) 10 When ICl had acquired its controlling interest in PT on December 31,205, ICl management had touted the potential synergies between the two companies. It is now the end of 207, and your friend is clearly disappointed by the financial resules Your friend does not see the reselt of atatements issued by ICl under IFRS for 20X7. consolidated financial statements, as provided synergy between the two companies in the total year-end equity is an unimpressive 5.940. You these numbers. To this your friend counters, "Fair enough. I'd like for you to show me just what I'm overlooking. Here are the separate-entity funancial statements of PTI for 20X7 and some other information that l've been able to gather about the two companies [Exhibit C]. Would you mind preparing the separate-entity financial statements of ICl Exhibit C ADDITIONAL INFORMATION On December 31, 20X5, the net identifiable assets of ICI had a fair yalue that was $2,275,000 greater than their net carrying value. Upstream sales from PTI to ICI during 207=$1,499,680. Downstream sales from ICl to PTI during 207=51,472,900. PTI (subsidiary) declared and paid dividends of $50,000 in 206 and $60,000 in 207. E ICl (parent) declared and paid dividends of $150,000 in 206 and $200,000 in 207. = Inventory purchased from PTI (subsidiary) in IC/'s (parent) 207 beginning inven. tory =5100,000. Inventory purchased from. PT (subsidiary) in ICls (parent) 207 ending inventory =$150,000. PTI sold goods at the same gross profit percentage in both 206 and 207. Inventory purchased from ICI (parent) in PTIs 207 beginning inventory =540,000. Inventory purchased from iCl (parent) in PTI's (subsidiary) 207 ending inventory = $50,000. ICI sold goods at the same gross profit percentage of 45% in both 206 and 207. - On January 1,206, Phi sold plant \& equipment that on that date had an original cost of $200,000 and carrying value of $100,000 to ICl for $200,000. The plant & equipment also had a future useful life of 10 years on lanuary 1,206. PTI (subsidiary) purchased additional fand from an outside party for $300,000 on Jansary 1, 20x7. Due to impairment in 207, the value of goodwill relating to the purchase of PI was worth 5175,000 on December 31,207. PII is the sole subsidrary of ICI. a Neither company purchased or sold any other buildings, plant and equipment, or land, of issued additional shares since ICI purchasedt its controlling interest in PI