Answered step by step

Verified Expert Solution

Question

1 Approved Answer

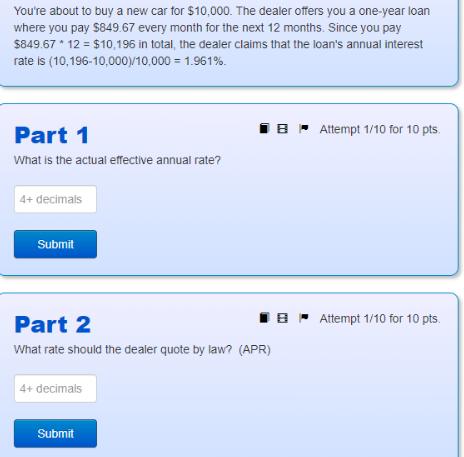

You're about to buy a new car for $10,000. The dealer offers you a one-year loan where you pay $849.67 every month for the

You're about to buy a new car for $10,000. The dealer offers you a one-year loan where you pay $849.67 every month for the next 12 months. Since you pay $849.67* 12 = $10,196 in total, the dealer claims that the loan's annual interest rate is (10,196-10,000)/10,000 = 1.961%. Part 1 What is the actual effective annual rate? 4+ decimals Submit Part 2 What rate should the dealer quote by law? (APR) 4+ decimals Submit BAttempt 1/10 for 10 pts. BAttempt 1/10 for 10 pts.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Part 1 Actual Effective Annual Rate The actual effective annual rate EAR is higher than the quoted r...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Document Format ( 2 attachments)

6643162691a27_952440.pdf

180 KBs PDF File

6643162691a27_952440.docx

120 KBs Word File

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Principles Of Managerial Finance

Authors: Lawrence J. Gitman, Chad J. Zutter

14th Global Edition

1292018208, 978-1292018201