Reconsider the data in Exercise 14.4. Define a new set of transformed variables as the first difference

Question:

Reconsider the data in Exercise 14.4. Define a new set of transformed variables as the first difference of the original variables, \(y_{t}^{\prime}=y_{t}-y_{t-1}\) and \(x_{t}^{\prime}=x_{t}-x_{t-1}\). Regress \(y_{t}^{\prime}\) on \(x_{t}^{\prime}\) through the origin. Compare the estimate of the slope from this first-difference approach with the estimate obtained from the iterative method in Exercise 14.4.

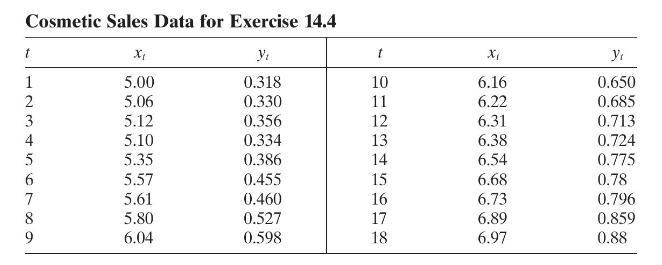

Data From Exercises 14.4

The data in the following table gives the monthly sales for a cosmetics manufacturer (yt) and the corresponding monthly sales for the entire industry (xt). The units of both variables are millions of dollars.

a. Build a simple linear regression model relating company sales to industry sales. Plot the residuals against time. Is there any indication of autocorrelation?

b. Use the Durbin-Watson test to determine if there is positive autocorrelation in the errors. What are your conclusions?

c. Use one iteration of the Cochrane-Orcutt procedure to estimate the model parameters. Compare the standard error of these regression coefficients with the standard error of the least-squares estimates.

d. Test for positive autocorrelation following the first iteration. Has the procedure been successful?

Step by Step Answer:

This question has not been answered yet.

You can Ask your question!

Introduction To Linear Regression Analysis

ISBN: 9781119578727

6th Edition

Authors: Douglas C. Montgomery, Elizabeth A. Peck, G. Geoffrey Vining