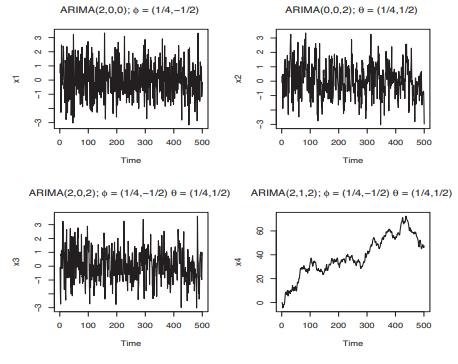

Question: As seen from Figure 5.13, there may be very little visual difference in ARMA models with different values of the coefficients. ARIMA models with (d>0)

As seen from Figure 5.13, there may be very little visual difference in ARMA models with different values of the coefficients. ARIMA models with \(d>0\) are generally nonstationary, however.

(a) Generate 500 values of an \(\operatorname{ARIMA}(2,1,2)\) process with Gaussian innovations and produce a time series plot of the differenced values.

Does the differenced series appear to be stationary?

(b) Now fit both the original series and the differenced series using auto. arima with both the AIC and the BIC. What models are chosen?

Figure 5.13:

x1 -1 0 1 2 3 ARIMA(2,0,0); = (1/4,-1/2) 0 100 200 300 400 500 Time x2 -3 -1 0 1 2 3 ARIMA(0,0,2); 0 = (1/4,1/2) 100 200 300 400 500 Time ARIMA(2,0,2); 0 = (1/4,-1/2) = (1/4,1/2) ARIMA(2,1,2); = (1/4,-1/2) = (1/4,1/2) x3 -3 -1 0 1 2 3 100 200 300 Time x4 40 & 09 400 500 0 100 200 300 400 500 Time

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts