Question: Consider the monthly log stock returns, in percentages and including dividends, of Merck & Company, Johnson & Johnson, General Electric, General Motors, Ford Motor Company,

Consider the monthly log stock returns, in percentages and including dividends, of Merck & Company, Johnson & Johnson, General Electric, General Motors, Ford Motor Company, and value-weighted index from January 1960 to December 2008; see the file m-mrk2vw. txt of Exercise 8.1 of Chapter 8.

(a) Perform a principal component analysis of the data using the sample covariance matrix.

(b) Perform a principal component analysis of the data using the sample correlation matrix.

(c) Perform a statistical factor analysis on the data. Identify the number of common factors. Obtain estimates of factor loadings using both the principal component and maximum-likelihood methods.

Exercise 8.1:

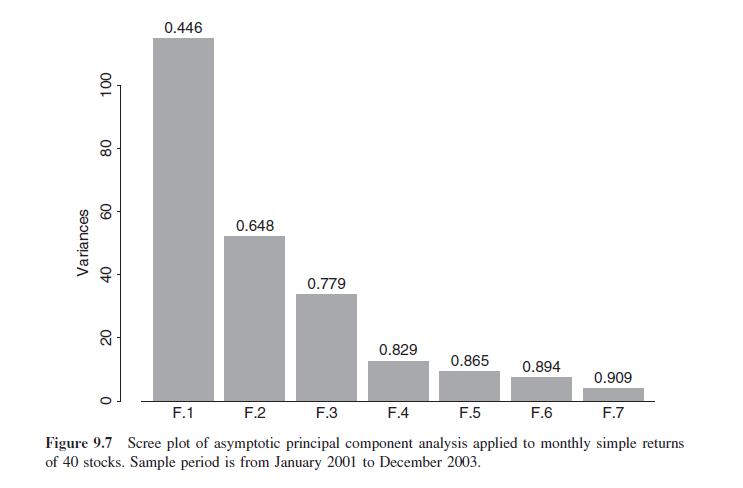

100 60 80 Variances 40 60 20 20 F.1 0.446 0.648 F.2 F.3 0.779 0.829 0.865 0.894 0.909 F.4 F.5 F.6 F.7 Figure 9.7 Scree plot of asymptotic principal component analysis applied to monthly simple returns of 40 stocks. Sample period is from January 2001 to December 2003.

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts