Consider the monthly stock returns of S&P composite index from January 1975 to December 2008 in Exercise

Question:

Consider the monthly stock returns of S\&P composite index from January 1975 to December 2008 in Exercise 1.2. Answer the following questions:

(a) What is the average annual log return over the data span?

(b) Assume that there were no transaction costs. If one invested \(\$ 1.00\) on the S\&P composite index at the beginning of 1975, what was the value of the investment at the end of 2008 ?

Exercise 1.2:

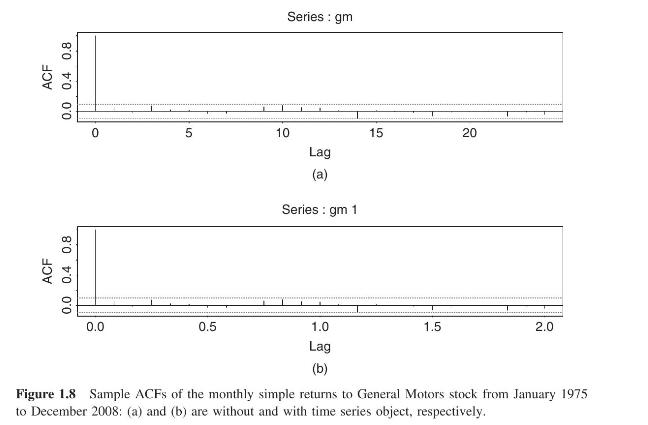

Answer the same questions as in Exercise 1.1 but using monthly stock returns for General Motors (GM), CRSP value-weighted index (VW), CRSP equalweighted index (EW), and S\&P composite index from January 1975 to December 2008. The returns of the indexes include dividend distributions. Data file is m-gm3dx7508.txt (date, gm, vw, ew, sp).

Exercise 1.1:

Consider the daily stock returns of American Express (AXP), Caterpillar (CAT), and Starbucks (SBUX) from January 1999 to December 2008. The

data are simple returns given in the file d-3stocks9908.txt (date, axp, cat, sbux).

Step by Step Answer: