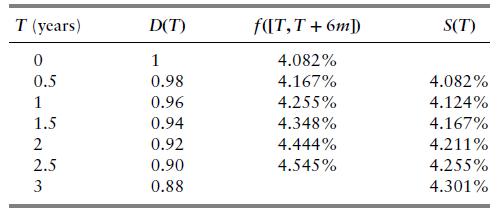

Using Table 7.3 and linear interpolation in discount factors (a) Calculate the spot and quarterly forward 3-month

Question:

Using Table 7.3 and linear interpolation in discount factors

(a) Calculate the spot and quarterly forward 3-month simple (add-on) rates, \(f\left(\left[T_{i}, T_{i+1}ight]ight)\) for \(T_{0}=0, T_{1}=3 m, \ldots, T_{12}=2 y 9 m\).

(b) Calculate the 2-year forward swap rate, 3 -month forward with semiannual payments on the fixed leg.

(c) Calculate the value to the fixed-rate receiver of a \(\$ 1 \mathrm{M} 3\)-month into 2 -year forward swap with semiannual fixed rate of \(3 \%\) per annum.

(d) What is the value of the above swap to the fixed-rate payer?

Table 7.3

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Answered By

Antony Sang

I am a research and academic writer whose work is outstanding. I always have my customer's interests at heart. Time is an important factor in our day to day life so I am always time conscious. Plagiarism has never been my thing whatsoever. I give best Research Papers, Computer science and IT papers, Lab reports, Law, programming, Term papers, English and literature, History, Math, Accounting, Business Studies, Finance, Economics, Business Management, Chemistry, Biology, Physics, Anthropology, Sociology, Psychology, Nutrition, Creative Writing, Health Care, Nursing, and Articles.

2+ Reviews

10+ Question Solved

Related Book For

Mathematical Techniques In Finance An Introduction Wiley Finance

ISBN: 9781119838401

1st Edition

Authors: Amir Sadr

Question Posted: