Using Table 7.3 and linear interpolation in discount factors, for a ($ 1 mathrm{M}) 1 -year swap

Question:

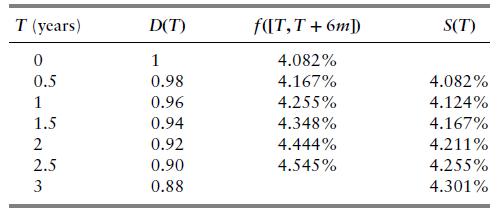

Using Table 7.3 and linear interpolation in discount factors, for a \(\$ 1 \mathrm{M}\) 1 -year swap with semiannual fixed rate of \(4 \%\) per annum and quarterly floating leg based on 3-month rates

(a) Compute the value of the semiannual fixed leg.

(b) Compute the value of the quarterly floating leg via discounting the forward 3-month rates.

(c) Compute the value of the floating leg via replication.

(d) What is the value of the swap to the fixed-rate receiver?

Table 7.3

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Answered By

Somshukla Chakraborty

I have a teaching experience of more than 4 years by now in diverse subjects like History,Geography,Political Science,Sociology,Business Enterprise,Economics,Environmental Management etc.I teach students from classes 9-12 and undergraduate students.I boards I handle are IB,IGCSE, state boards,ICSE, CBSE.I am passionate about teaching.Full satisfaction of the students is my main goal.

I have completed my graduation and master's in history from Jadavpur University Kolkata,India in 2012 and I have completed my B.Ed from the same University in 2013. I have taught in a reputed school of Kolkata (subjects-History,Geography,Civics,Political Science) from 2014-2016.I worked as a guest lecturer of history in a college of Kolkata for 2 years teaching students of 1st ,2nd and 3rd year. I taught Ancient and Modern Indian history there.I have taught in another school in Mohali,Punjab teaching students from classes 9-12.Presently I am working as an online tutor with concept tutors,Bangalore,India(Carve Niche Pvt.Ltd.) for the last 1year and also have been appointed as an online history tutor by Course Hero(California,U.S) and Vidyalai.com(Chennai,India).

2+ Reviews

10+ Question Solved

Related Book For

Mathematical Techniques In Finance An Introduction Wiley Finance

ISBN: 9781119838401

1st Edition

Authors: Amir Sadr

Question Posted: