New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

financial accounting

Financial Accounting 1st Edition Dhanesh K. Khatri - Solutions

Dinesh Limited was acquired by Kamlesh Limited for which Kamlesh issued 85,000 equity shares of face value ₹10, each having market price ₹13 per share on the stock exchange. Apart from this, Kamlesh paid ₹1 per share for every equity share of Dinesh. Dinesh has total 1,70,000 equity shares of

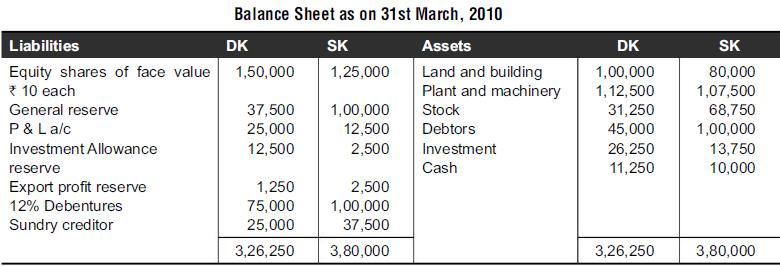

DK Limited and SK Limited amalgamated on 1st April, 2010. All the assets and liabilities of both the companies were acquired by newly established company DS Limited. The following was the balance sheet of both the companies on 1st April, 2010:DS agreed to issued required number of equity shares of

When acquiring company takes all the assets and liabilities at the book value and discharges the purchase consideration by issuing its shares, then it is to be accounted for by using(a) Pooling of interest method(b) Purchase method(c) Any of these as it is subjective(d) None of these

Three companies Dee, Pee and Cee having 10,000; 15,000 and 20,000 equity shares, respectively, of face value of ₹10 each were combined together and all the assets and liabilities of these companies were acquired by a newly formed company namely DPC. DPC issued shares to each of these companies in

Under purchase method of amalgamation, if net asset value exceeds the amount of purchase consideration, then it results into(a) Goodwill(b) Capital reserve(c) Adjustment in general reserve(d) None of these

DXK Limited was acquired by KXD Limited for which KXD agrees to issue 50,000 equity shares of face value ₹10 each having market price ₹23 per share on the stock exchange, apart from this KXD paid ₹2 per share for every equity share of DXK. DXK has total 70,000 equity shares of ₹10 each.

Under purchase method of amalgamation, if net asset value is less than the amount of purchase consideration, then it results into(a) Goodwill(b) Capital reserve(c) Adjustment in general reserve(D) None of these

Taking the case of previous example if KXD incurred ₹30,000 as expenses in issuing equity shares pursuant to business combination and it also incurred an additional expense ₹20,000 as liquidation expenses of DXK. Further to it KXD has legal depart which devoted a total time of one month to

How have amalgamation and demerger been defined under Income Tax Act, 1961? What are the taxation provisions for it?

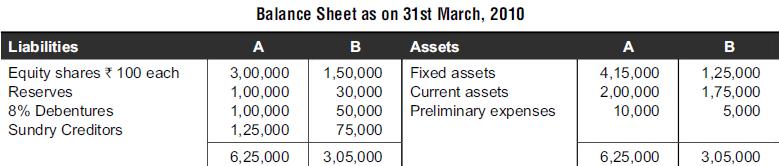

The following are the balance sheets of A and B as on 31st March, 2010:Goodwill of A and goodwill of B are to be valued at ₹60,000 and ₹20,000, respectively. A purchased B for which it agreed to issue requisite number of equity shares of face value ₹100, each at a premium of ₹25 each.

Joint venture, co-ownership of assets, and acquisition of assets of group of assets that does not constitute a separately identifiable legal business entity are not considered as(a) Amalgamation in the nature of merger(b) Amalgamation in the nature of purchase(c) Either of these(d) Neither of

Write short notes on the following:(a) Reverse acquisition(b) Slump sales under income tax act, 1961(c) Goodwill vs. negative goodwill(d) Pooling of interest vs. purchase method of accounting(e) Contingent consideration

When there exists the provision for contingent consideration, the allocation period shall not exceed(a) Twelve months(b) Six months(c) Three months(d) None of these

In a demerger or amalgamation, the maximum period for which accumulated losses and unabsorbed losses can be carried forward is(a) Five years(b) Eight years(c) Two years(d) None of these

Amalgamation and demerger expense should be recognized as(a) Expensed in the year of amalgamation or demerger(b) Amortized over a period of five years from the date of amalgamation or demerger(c) Amortized over a period of eight years from the date of amalgamation or demerger(d) None of these

Show direct posting to ledger account for the following transactions and prepare trial balance:(i) Ramesh started business with cash ₹2,50,000(ii) Deposited cash into bank ₹1,20,000(iii) Purchased furniture for ₹35,000 in cash(iv) Purchased goods from Deepak of ₹15,000 in cash(v) Purchased

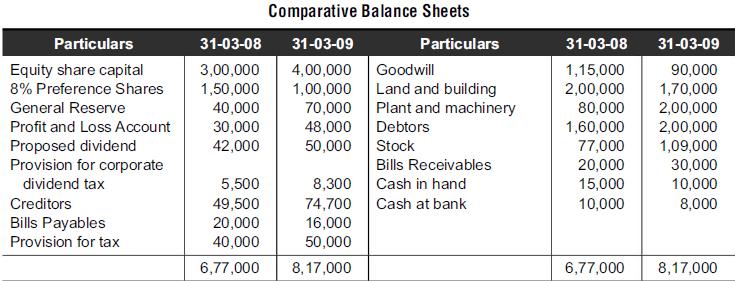

The following is the summary of balance sheet of Deepak Plastics Ltd for the year ending March 31, 2009. Prepare fund flow statement. Also draw inferences.Additional Information:(i) ₹35,000 has been provided as provision for income tax during the year 2008-09.(ii) Depreciation of ₹50,000 and

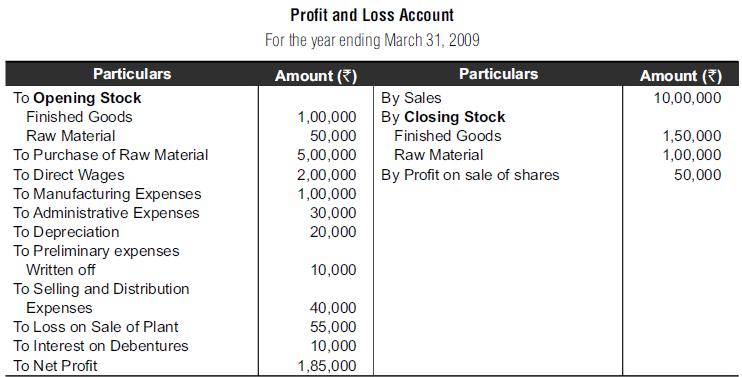

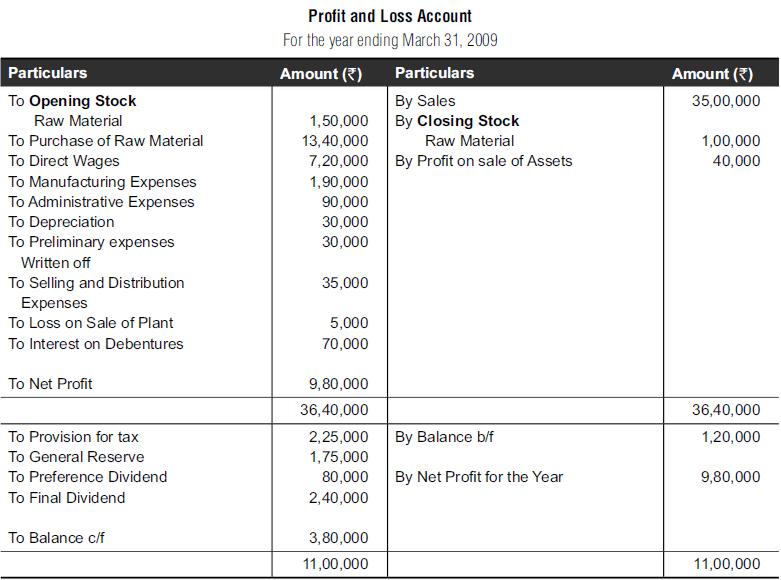

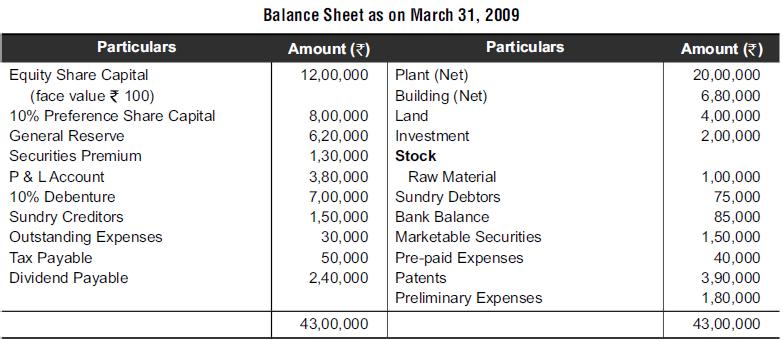

The following is the profit and loss account and balance sheet of Sach International Ltd. Redraft these for the purpose of ratio analysis and calculate profitability ratios based on sales. Particulars To Opening Stock Finished Goods Raw Material To Purchase of Raw Material To Direct Wages To

Firms A and B are identical with respect to their working except the difference in leverage. X is an unleveraged firm and Y is a leveraged firm. Total capital invested in each of the company is ₹10,00,000; the debt and equity in Y is in equal ratio with rate of interest on debt 12%. EBIT of both

Total liabilities of a firm is ₹100 lakh and current ratio is 1.5:1. If fixed assets and other non-current assets are to the tune of ₹70 lakh and debt-equity ratio being 4:1. What would be the long-term liabilities?

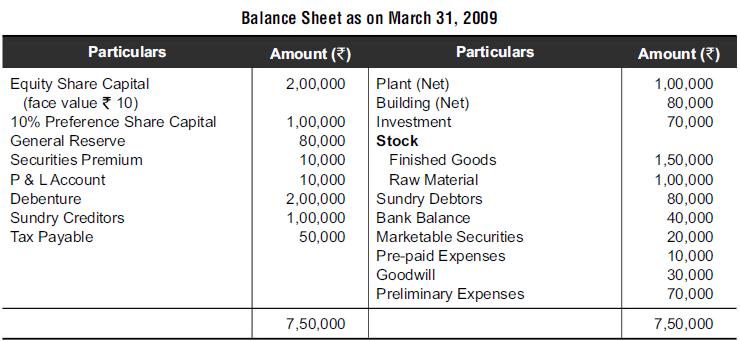

Calculate financial ratio from the following income statement and balance sheet: Particulars To Opening Stock Raw Material To Purchase of Raw Material To Direct Wages To Manufacturing Expenses To Administrative Expenses To Depreciation To Preliminary expenses Written off To Selling and

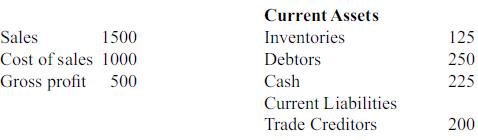

From the following financial statement, calculate(i) Current ratio (ii) Acid test ratio (iii) Inventory turnover (iv) Average debt collection period (v) Average creditors’ payment period 1500 Sales Cost of sales 1000 Gross profit 500 Current Assets Inventories Debtors Cash Current

Current ratio is say 1.5: 1, total of balance sheet being ₹22 lakh. The amount of Fixed assets + Non-current Assets is ₹10 lakh. What would be the current liabilities?

Calculate market-related ratio using the data of Examples 7 and 8 market price per share can be taken as ₹125 and equity dividend ₹40,000Data from Example 7The following is the profit and loss account and balance sheet of Sach International Ltd. Redraft these for the purpose of ratio analysis

The following facts have been extracted from the annual accounts of Zeta Ltd:Net sales ₹30 lakh, EBIT ₹6 lakh, equity net worth ₹18 lakh, long-term debt 6 lakh, short-term interest bearing debt ₹2 lakh. Total interest payment ₹1.5 lakh.If tax rate is 30%, then calculate(i) ROIC and (ii)

Calculate ratios from the following details: Facts Extracted from Annual Report of L & T Ltd (in crore) L & T Balance Sheet Fixed Assets Investments Current Assets Stock S. Debtors Pre-paid Expenses Marketable Sec. Cash & Bank Balance Loan & Advances Accrued Interest Intangible & Fictitious

The following are the actual ratios of Gypsy Ltd and the corresponding standards: Ratio Current ratio Liquid ratio Gross profit margin Operating profit margin Net profit margin Creditor payment period Inventory turnover Debtors collection period Fixed asset turnover ratio Debt: equity ratio Return

From the following details, prepare fund flow statement:Additional Information:Balance of accumulated depreciation account as on previous year was ₹16,000 and as at the end of current year was ₹19,000. (A) Assets Fixed Assets (net) Debtors Inventory Prepaid rent Cash Balance Total Assets (B)

The following additional information and balance sheet are of Sigma Ltd:Additional Information(i) During the current year dividend paid was ₹52,000 tax paid was ₹24,000.(ii) During the current year one machine having original cost ₹20,000 and accumulated depreciation ₹17,000 was sold for

The following records have been extracted from the stores ledger of VXI Ltd:Prepare stock register under continuous inventory valuation system using(a) LIFO,(b) FIFO,(c) simple average of prices and(d) weighted average of prices method. Date 02/01/08 21/01/08 31/01/08 10/02/08 15/03/08 Purchase

Danish departmental stores reported the facts about the grocery items that it had opening stock of sales value ₹1,47,500 (cost ₹1,20,400) during the year company purchased the items for which total cost of acquisition was ₹18,45,600 with a normal selling price of ₹20,82,700. Sales at normal

The following records have been extracted from the stores ledger of Manglam Enterprises Ltd:Find out value of closing inventory under periodic system using (a) LIFO, (b) FIFO, (c) Simple average of prices (d) Weighted average of prices method.

The following facts have been extracted from the books of Truth International Corporation:Sales during the year ₹1,34,70,000, the opening stock at cost was ₹61,25,000 and company made a purchase of ₹56,38,000. Certain goods costing ₹94,000 were damaged by fire and considered as abnormal

Sach Organics Ltd could not complete the valuation of inventory on March 31, 2009; however, it valued the inventory on April 9, 2009. The relevant facts extracted from the accounting records for the period April 1, 2009 to April 9, 2009 were as follows:Sales ₹65,76,000; purchase ₹28,33,000:

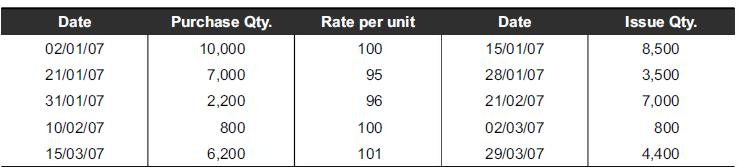

The following records have been extracted from the stores ledger of DXL Ltd:Prepare stock register under continuous inventory valuation system using(a) LIFO,(b) FIFO,(c) simple average of prices and(d) weighted average of prices method. Date 02/01/07 21/01/07 31/01/07 10/02/07 15/03/07 Purchase

Kumar Silk Mills reported these facts about the silk items—opening stock of sales value ₹2,00,000 (cost ₹1,80,400) during the year company purchased the items for which total cost of acquisition was ₹22,55,600 with a normal selling price of ₹25,15,000. Sales at normal selling price during

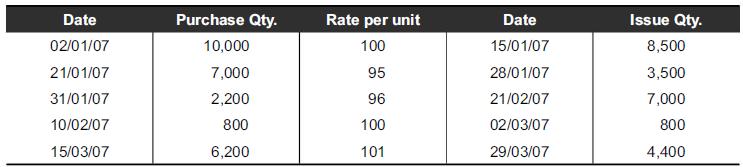

The following records have been extracted from the stores ledger of DXL Ltd:Find out value of closing inventory under periodic system using(a) LIFO,(b) FIFO,(c) Simple Average of Prices and(d) Weighted Average of Prices method. Date 02/01/07 21/01/07 31/01/07 10/02/07 15/03/07 Purchase

The following records have been extracted from the stock ledger of XXL Ltd:The opening inventory was 3,000 units costing ₹92 per unit. Till last year, the company used to follow LIFO method under periodic inventory valuation system, during the current year it was changed to FIFO. Find out the

The following facts have been extracted from the books of Faith International Corporation:Sales during the year ₹2,54,90,000, the opening stock at cost was ₹81,25,000 and company made a purchase of ₹1,16,39,000. Certain goods costing ₹1,94,000 were damaged by fire and considered as abnormal

Opening stock of an item in the godown is 2,000 units costing ₹22 per unit, during the year, the following purchase was made:10,000 units @ ₹25; 6,000 units @ ₹24 ; 9,000 units @ ₹23 During the year, 24,500 units were sold. Find out value of closing inventory under periodic system using

Spares likely to be consumed over the useful life of a fixed asset are(a) To be capitalized(b) To be expensed(c) A subjective matter(d) None of these

Write short notes on the following:(a) Pre-commissioning costs(b) Internally generated goodwill(c) Impairment of assets(d) Reversal of impairment loss

The following facts have been extracted from the books of accounts of Rolta Enterprises Ltd (REL):The company acquired new plant and machinery costing ₹22,50,000 and spent ₹1,30,000 as carriage and ₹1,20,000 as installation charges to install it. To finance it company raised a loan of

Spares likely to be consumed for routine repairs and maintenance are(a) To be capitalized(b) To be expensed(c) A subjective matter(d) None of these

The following facts have been extracted from the books of accounts of Reliable Enterprises Ltd (REL):The company acquired a new plant and machinery costing ₹ 12,00,000 and spent ₹ 30,000 as carriage and ₹ 20,000 as installation charges to install it. To finance it, the company raised a

How is inventory valued as per AS-02? Discuss.

Zeta Ltd (ZL) has acquired a boiler on hire purchase scheme for this company paid ₹70,000 as down payment and rest of the amount is to be paid in 48 equal monthly installments of ₹10,000 each. The title to boiler will be transferred in the favour of ZL on the payment of last installment. The

Safety equipment and environment protection tools do not generate any cash inflow, then these should be(a) Capitalized(b) Expensed(c) Recognized as deferred revenue expense

Zeta Ltd (ZL) has acquired a boiler on hire purchase scheme for this company paid ₹ 3,50,000 as down payment and rest of the amount is to be paid in 36 equal monthly installments of ₹ 20,000 each. The title to boiler will be transferred in the favour of ZL on the payment of last

Explain the term ‘investment and investment property’. How is it recognized in the books of accounts?

On April 1, 2008 a machine was purchased for ₹170,000. Estimated useful life of machine is three years with an estimate of salvage value ₹17,000 at the end. If company provides depreciation as per straight line method then calculate the amount of depreciation for each of the three years.

₹50,000 was spent as routine administrative expenses and ₹45,000 as specially for the acquisition of a machine, the cost of machine acquired is ₹95,000. The machine is to be recognized initially at(a) 95,000(b) 1,90,000(c) 1,40,000(d) 1,00,000

Kite Ltd (KL) has acquired a boiler on hire purchase scheme for this company paid ₹ 3,50,000 as down payment and rest of the amount is to be paid in 36 equal monthly installments of ₹ 20,000 each. The title to boiler will be transferred in the favour of ZL on the payment of last

On April 1, 2009 a transport company purchased ten truck tyres costing a total amount of ₹6,00,000 with an estimated total mileage from each of the tyre of 1,20,000 kilometres with a zero salvage value at the end. However, the company will spend ₹10,000 per tyre on repairs and maintenance after

A plant was installed by paying 3,00,000 to a vendor. For this purpose, the company incurred pre-commissioning expenses of 75,000, of which 60% could have been avoided had this plant not been installed. The initially recognized value of plant is(a) 3,75,000(b) 3,45,000(c) 3,30,000(d) 3,60,000

On April 1, 2008 a machine was purchased for ₹ 70,000. Estimated useful life of machine is three years with an estimate of salvage value ₹7,000 at the end. If the company provides depreciation as per straight line method then calculate the amount of depreciation for each of the three years.

On April 1, 2007 a machine was purchased for ₹9,00,000. Estimated useful life of machine is six years with an estimate of zero salvage value at the end. Till the year 2008–09 depreciation was charged as per SLM and from the year 2009–10 the method of charging depreciation was changed to WDV

Land and development cost incurred by a company in constructing a project, which comprises certain land development expenses, is irrelevant even if such project is not commissioned. Then how should these be recognized?(a) It is to be capitalized.(b) It is to be expensed.(c) Either of

Ramesh Ltd (RL) has a machine with carrying amount ₹4,50,000 and Kapil Ltd (KL) has a machine with carrying amount ₹4,35,000. Both the companies decide to exchange these machines for the mutual benefit. The active market value of the machines is ₹4,95,000 and ₹ 4,78,000, respectively.

On April 1, 2009 a furnace was purchased for ₹ 2,70,000. Estimated useful life of this furnace is 25,000 hours with an estimate of salvage value ₹ 20,000 at the end. During the year 2009–10, the furnace was put to use for 4,100 hours and during 2009–10 it was used for 4,250 hours of

A business enterprise obtaining fixed asset by the exchange of another fixed asset which has significant commercial substance should recognize the asset initial at(a) Fair value of asset given up(b) Replacement value(c) Carrying cost of asset given up(d) Fair value of asset acquired

As on April 1, 2009 the carrying amount of ATM (automated teller machine) of a bank is ₹8,50,000. By considering internal and external indicators company recognizes impairment loss. The net sales value is assessed ₹5,25,000 and value in use is calculated as ₹6,80,000. Show how this ATM is to

On April 1, 2008, a machine was purchased for ₹ 70,000. Estimated useful life of machine is three with an estimate of salvage value ₹ 15,000 at the end. If company provides depreciation as per written down value method using 40% p.a. as the depreciation rate, then calculate the amount of

A plant constructed at a cost of ₹40,00,000 in the year 2003 was considered for revaluation in the year 2006 and its net book value was enhance by ₹4,10,000 resulting into revaluation reserve. In the year 2008, an impairment loss of ₹3,40,000 is recognized. How such loss is to be recognized

A company running educational programs receives education set—an equipment at no cost from Government; under government grant it does not has active market value, it should be initially recognized at(a) Money spent by government(b) Active market value of similar item(c) Nominal value(d) None

On April 1, 2009, a transport company purchased 20 truck tyres costing a total amount of ₹ 6,60,000 with an estimated total mileage from each of the tyre of 1,00,000 kilometres with a salvage value of ₹ 3,000 per tyre at the end. During the years 2009–10 and 2010–11, each of the tyre

According to AS-10, how foreign currency difference is accounted for(a) It is expensed(b) It is capitalized(c) Neither of these(d) Either of these

On April 1, 2007, a machine was purchased for ₹ 70,000. Estimated useful life of machine is five years with an estimate of zero salvage value at the end. Company provides depreciation @ 20% p.a. as per straight line method. Till the year 2008–09, the depreciation was charged as per SLM and

According to AS-16 how foreign currency difference is accounted for(a) It is expensed(b) It is capitalized(c) Neither of these(d) Either of these

Masters Ltd is engaged in the development of education equipment and educational methods. It carries research and development activities to bring improvement in the teaching methodologies. It incurred ₹ 100 crore on general research work and another 70 crore to be allocated equally to research

How should the relocation cost incurred to safeguard the plant and machinery be recognized?(a) It is expensed(b) It is capitalized(c) Either of these(d) Neither of these

Cupla Ltd, manufacturing speciality drugs, purchases patent from Hexa Ltd at a cost of ₹ 9,00,000. The patent right is acquired for a period of five years with zero recoverable value at the end. Show how patent is to be amortized over five years.

A company spends every year 2 crore for general skills enhancement of its employees and another 1 crore for specific skill enhancement with reference to a particular machine, how these should be recognized?(a) Both should be capitalized(b) Only 2 crore is to be capitalized.(c) Only 1 crore is to

As on April 1, 2009 the carrying amount of ATM (automated teller machine) of a bank is ₹ 9,00,000. By considering internal and external indicators, the company recognizes impairment loss. The net sales value is assessed at ₹ 7,15,000 and value in use is calculated as ₹ 6,80,000.Show how

A company is likely to receive ₹ 10,000, ₹ 12,000 and ₹ 8,000 at the end of next three years, respectively. Calculate the present value if discount rate is 10% per annum.

A company is likely to receive ₹ 10,000 P.A. for next five years. Calculate the present value if discount rate is 10% per annum.

A plant constructed at a cost of ₹ 30,00,000 in the year 2003 was considered for revaluation in the year 2006 and its net book value was enhanced by ₹ 2,50,000 resulting into revaluation reserve. In the year 2008, an impairment loss of ₹ 2,40,000 is recognized. How is such loss

Pass the following journal entries and make ledger accounts:(i) Started business with cash ₹6,50,000(ii) Deposited cash into bank ₹2,10,000(iii) Purchased machinery for ₹93,000 in cash(iv) Paid rent ₹15,500 by cheque(v) Purchased goods of ₹85,000 from Amit(vi) Paid wages for the month

Capital structure of a company includes the following:(i) Equity share capital: 7,00,000 shares of face value ₹10 each (ii) Preference shares capital: 20,000, 12% shares of face value ₹100 each (iii) Debt of ₹30,00,000 bearing a coupon rate of 15%During the year, the company earned EAT of

Capital of a company on April 1, 2010 comprised 3,00,00,000 equity shares of face value ₹10 each, and 14% preference shares of total value ₹12,00,00,000. On this date, the net balance of reserve and surplus was ₹9,00,00,000. During the year, the company had EAT of ₹30,00,00,000, out of

A company earned EAT of ₹18,00,000, whereas its capital comprised only equity share capital represented by 4,50,000 equity shares of face value 10 each. The average price earning multiplier (P/E Ratio) of the industry to which this company belongs is 30. Estimate value of equity shares of the

An investor purchases 100 shares of a company at a price of ₹50. At the end of one year, he/she gets a dividend of ₹8 per share and sells the share in the market at a price of ₹47 per share after one year. Calculate the return on equity.

An investor purchases 100 shares of a company at a price of ₹160, whereas face value per share is ₹10, he/she expects to get 90% dividend at the end of one year and expected market price at the end of the year is ₹180. Calculate the return on equity.

In the market, 12% ₹100 debentures are available at a price of ₹96 per debenture, the expenses (brokerage and securities transaction tax) at the time of purchase of shares is Re. 1 per debenture. Only one year is left to maturity, it has a provision of redemption at par on maturity. If an

“People might come or might go but the entity of a company does not get affected.” Discuss.

Explain the concept of a limited liability company and differentiate between a public limited company and a private limited company.

Write short notes on the following:(a) Concept of legal separate entity(b) Concept of separate accounting entity(c) Depreciation

Write an essay as to how a limited liability company can raise the capital.

Explain the concept of borrowed capital.

Discuss the concept of audit as a tool to exercise control.

Elaborate the concept of hybrid securities.

“Balance sheet is prepared by following stock concept, whereas profit and loss account is prepared following flow concept.” Discuss.

“Annual report is much superior to the balance sheet.” Explain.

Financial accounting is such an accounting mechanism that helps in making aggregate presentation of monetary transactions to arrive at the financial result of the business enterprise. Explain.

Management Accounting is that branch of accounting that aims at providing information to managers for decision-making. Discuss.

Costing is the technique and process of ascertaining cost. It has the important objective of ascertaining the cost of goods and services being produced. Explain.

Explain cash system of accounting how it is different from accrual system of accounting.

“Accounting concepts are like scientific rules, which are time-tested and applicable universally across the boundaries and in different situations, whereas accounting conventions are certain accounting policies and procedures, which are followed as a matter of practice in the business

“Balance sheet is like corporate bikini, which conceal more than what it reveals.” Do you agree? Explain.

Differentiate between financial capital maintenance and physical capital maintenance.

Showing 500 - 600

of 7094

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

Last

Step by Step Answers