New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

financial accounting

Financial Accounting 1st Edition Dhanesh K. Khatri - Solutions

From the following balance sheet, calculate liquidity ratio. Liabilities Equity Share Capital Reserves P & L Account Bank Overdraft Bills Payable Sundry Creditors Amount (3) 1,00,000 50,000 50,000 30,000 25,000 45,000 3,00,000 Fixed Assets Stock Assets Sundry Debtors Bills Receivables Cash and

From the following balance sheet, calculate solvency group ratio. Liabilities Equity Share Capital Preference Share Capital General Reserves Securities premium P & L Account Debentures Secured Bank Loan Bank Overdraft Sundry Creditors Tax Payable Dividend Payable Amount

EBIT of a company for the year is ₹9 lakh and capital structure of the company includes equity share capital (face value ₹10 each) of ₹30 lakh, 10% debentures of ₹10 lakh and 12% preference share capital of ₹10 lakh. Tax rate for the company is 30%. Calculate financial leverage and EPS.

A company is selling 30,000 units of its product @ ₹40 per unit, variable cost per unit is ₹22 and total operating fixed cost of the company is ₹1,80,000. Calculate operating leverage and show by how much percentage EBIT will increase if sales increases by 25 percentage from the present level

By using the income statement of Example 7 and the following balance sheet, calculate investment-based profitability ratios. Particulars Equity Share Capital (face value 10) 10% Preference Share Capital General Reserve Securities Premium P & L Account Debenture Sundry Creditors Tax Payable Balance

The following facts have been extracted from the annual accounts of Zavit Ltd:Net sales ₹30 lakh, EBIT ₹6 lakh, equity net worth ₹18 lakh, long-term debt 6 lakh, short-term interest bearing debt ₹2 lakh. Total interest payment ₹1.5 lakh.If tax rate is 30%, then calculate(i) ROIC (ii) ROE

Prepare fund flow statement and carry out inferences.Additional information:(i) Investments costing ₹8,000 were sold during the year 2009–10 for ₹8,500.(ii) Provision for tax made during the year 2009–10 was ₹9,000.(iii) During the year part of the fixed asset costing (book value) 10,000

DXL Ltd issued 10% bonds of face value ₹50,000 on April 1, 2006 at a market price of ₹46,960. DXL Ltd categorized these bonds to be ‘held-till-maturity’. Show how the difference between maturity value of ₹50,000 and the issue price will be amortized over the holding period.

The balance sheet of DXI Ltd for the year 2009–10 disclosed ₹5,60,000 as liability for derivative contract expiring in next six months from the date of balance sheet. In the next financial year, i.e., 2010–11 the liability for the derivative contract was discharged at ₹5,45,000. Show how

The manufacturer of automatic gear scooters gives a warranty of three years on every scooter for the repair or replacement of the scooters that fail to perform as per the specifi cation. The past experience reveals that on an average 7% of the scooters require repair costing ₹4,000 each and

Continuing with Example 3. If in case the each scooter can raise only one claim during the period of three year. During the year 2010–11, 350 scooters were repaired at a cost of ₹2,700 each and another 150 were replaced at a cost of ₹6,200 each. Show how subsequent measurement of these

XY bank gives guarantee in the favour of MM bank for loan taken by MM of ₹20 lakh. As on 2007–08 the financial position of MM is sound and there is not internal or external indicator indicating default by MM. During the year 2008–09, MM suffered heavy loss on account of sub-prime crisis and

The average age of employees of a company is 55 years the retirement age is 60 years. The defined benefit plan introduced in the current year envisages payment of extra-retirement benefit equal to 10% of the last salary drawn for each of year of service put in by the employee from the date of

Sunshine Limited (SL) invited application for the issue of 1,00,00,000 equity shares of face value ₹ 10 each issued at par for cash all the shares were subscribed for and issued as per the rules. Another 50,000 equity shares of ₹ 10 were issued to the vendors of machinery. Show how financial

On February 14, 2011, Deepak Limited (DL) entered into a contract for buying two lot of call option with product series ‘CA, Tata Motors (1700), 1200, April 2011, 30’ and sold one lot of put option with product series ‘PA, Maruti Suzuki (800), 1450, April 2011, 40’. It also entered into a

TTKS Limited issued (i) 30,000, 12% redeemable preference shares of face value ₹ 100 each at 10% premium, (ii) 50,000, 14% non-redeemable preference shares of face value ₹ 10 each at a premium of ₹ 20 each, (iii) 25,000, 3 years, 9% redeemable debentures amounting to ₹ 25,00,000, (iv)

XL Limited (XXL) has issued 20,000 10% debentures of face value ₹ 100 each, each debenture is convertible into two equity shares after 12 months from the date of issue of debenture. Rate of interest on similar debentures without conversion option is 12% per annum. Show how it is to be recognized.

On April 1, 2000 Simplox Limited (SL) issued 10% convertible debentures of face value ₹ 200 each. Each debenture is convertible into four equity shares after five years from the date of issue. Had SL issued redeemable debentures then it would have offered an interest rate of 11% on these

On April 1, 2010 a co-operative society has 300 members each contributing 200 units of face value ₹ 10 each. The bye-laws of the society provide that on account of redemption of units number of members shall not fall below 120 with each contributing minimum 200 units. On April 1, 2011 society

On January 1, 2010 Subodh Limited (SL) purchased a futures with quantity 200 shares of XYZ @ 120 per share with twelve months to expiry. On March 31, 2010 market spot market price of XYS is ₹ 140 per share. Show how this futures is to be recognized.

Sachkhand Enterprises (SE) buys the following option contract on Feb. 4, 2011 from Naam Enterprises (NE):(i) CA, RIL (300), April 2011, 1,050, @ ₹ 29.(ii) PA, Tata Motor (500), April 2011, 1,250, @ ₹ 40. He makes the payment of premium for both the option contracts. On March 31, 2011 at the

Sunshine Hotels Limited (SHL) extends boarding and lodging facility to the business executives of multinational companies for which it receives payment in the US dollar ($). On January 1, 2011 it raised a bill for $ 30,000 to one of its customers. On this date, the exchange rate for Indian rupee

Diamond Jewellers Limited (DJL) has its foreign business operation in USA. The foreign business division disclosed jewellery costing US $ 10,000 as closing stock. The exchange rate on the date of purchase of these items was ₹ 46 per US $ on balance sheet date recoverable value of closing stock is

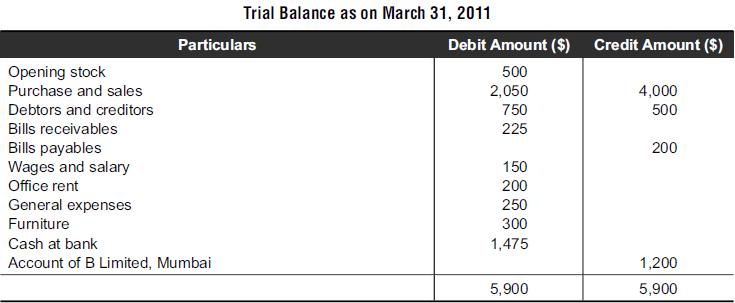

Convert the following trial balance of New York branch (NYB) of B Limited (BL) in Mumbai. Closing stock with the branch was $ 600 B Limited showed NYB's account with Rs. 40,000 debit balance. In the books of BL branch, furniture appeared at ₹11,500. The exchange rate on March 31, 2010 was 46 and

Taking the data of Example 10, show how exchange difference is to be recognized.Data from Example 10Sunshine Hotels Limited (SHL) extends boarding and lodging facility to the business executives of multinational companies for which it receives payment in the US dollar ($). On January 1, 2011 it

On April 1, 2009 Wizex Limited (WL) issued foreign currency denominated debentures worth 1,00,000 US $ the debentures with initial exchange rate ₹45 per dollar, these are redeemable in four equal installments at an interval of six months. The exchange rate on the respective redemption date was as

Ding Dong Limited (DDL) buys a call option to buy a fix number of its own shares on expiry of the option. It also buys a call option to buy a share of its subsidiary on expiry of the option. Show how these are to be recognized.

Show how financial liabilities, equity or financial asset is to be recognized in each of the following cases:(i) A co-operative society has 500 members each holding 100 units of ₹10 each. The statute of co-operative society provides for the redemption of units at the initiation of members but in

On April 1, 2000 Simplox Limited (SL) issued 10% convertible debentures of face value ₹200 each. Each debenture is convertible into four equity shares after five years from the date of issue.Had SL issued redeemable debentures then it would have offered an interest rate of 11% on these

Taking the data of Example 9, if on the expiry, i.e., on last Thursday April 28, 2011 premium is ₹75 and ₹8, respectively. Then accounting will be as follows:Data from Example 9Sachkhand Enterprises (SE) buys the following option contract on Feb. 4, 2011 from Naam Enterprises (NE):(i) CA, RIL

X Ltd invited application to issue 20,000 equity shares of face value ₹10 each at par. The complete amount is to be paid with the application. The company received application for (a) 20,000 shares;(b) 18,000 shares;(c) 25,000 shares. The shares were issued as per the provisions of law. Pass

Dee Cee Ltd invited application to issue 10,000 equity shares of face value ₹10 each at par. The amount to be paid as to ₹4 at the time of application, ₹2.50 on allotment, and the remaining amount on first and final call. The company received the application for 10,000 shares all the shares

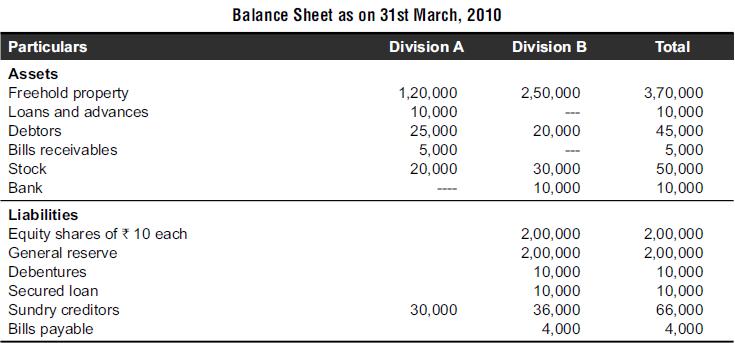

The following are the balance sheets of AB Limited as on 31st March, 2010, which has two distinct business segments i.e. ‘Division A’ and ‘Division B’. On 31st March, 2010, it was decided to spin off division A by transferring it to a newly established company A Limited which shall issue

On 1st April, 2010, Dubar Limited acquired the assets and liabilities of Super Limited.Dubar and Super agreed for the following scheme of business acquisition:(i) Dubar not to take investment of Super.(ii) Freehold property of Super to be valued at ₹1,70,000 and stock at ₹60,000.(iii) Stock of

On April 1, 2010 Gussain Limited (GL) purchased 30% equity shares of George Huss Limited (GHL) at a cost of ₹1,80,000. The equity of GHL Limited on this date comprised(a) Equity share capital ₹3,00,000,(b) Securities premium ₹2,00,000,(c) Reserve and surplus ₹1,00,000.During the year

Jay Pee Ltd invited application to issue 10,000 equity shares of face value ₹10 each at par. The amount to be paid as to ₹3 at the time of application, ₹2 on allotment, and the remaining amount on first and final call. The company received the application for 12,000 shares, applicants for

J.J. Ltd invited application to issue 20,000 equity shares of face value ₹10 each at par. The amount to be paid as to ₹5 at the time of application, ₹3 on allotment, ₹1 per share on first call and ₹1 per share on second and last call. The company received the application for 28,000

J.K. Ltd invited application to issue 30,000 equity shares of face value ₹10 each at 10% premium. The amount to be paid as to ₹6 at the time of application, ₹4 (including premium) on allotment, Re. 1 per share on first and final call. The company received the application for 35,000 shares,

M.M. Ltd invited application to issue 12,000 equity shares of face value ₹10 each at 10% discount. The amount to be paid as to ₹3 at the time of application, ₹2 on allotment, and remaining amount on first call. The company received the application for 17,000 shares, applicants for 2,000

Taking the data of Example 6, if shares of both the defaulting shareholder are forfeited as per rules and further reissued at ₹8.50 per share as fully paid, show entries relating to forfeiture and reissue of shares.Data from Example 6M.M. Ltd invited application to issue 12,000 equity shares of

If in Example 7, only 400 shares relating to first defaulter are reissued then show how the entries should be passed.Data from Example 7Taking the data of Example 6, if shares of both the defaulting shareholder are forfeited as per rules and further reissued at ₹8.50 per share as fully paid, show

Show the following items in the balance sheet as on March 31, 2010:Authorized share capital of the company is 2,00,000 equity shares of face value ₹10 each. .Out of these, 1,50,000 shares were issued at a premium of Re. 1 each by the company as fully paid. All the amounts were received except on

Show the following items in the balance sheet as on March 31, 2011. Authorized share capital of the company is 5,00,000 equity shares of face value ₹10 each. Out of these, 3,00,000 shares were issued at a discount of ₹1 each by the company as fully paid. All the amounts were received except on

Jay Pee Ltd invited application to issue 10,000 9% preference shares of face value ₹10 each at par. The amount to be paid as to ₹3 at the time of application, ₹2 on allotment, and the remaining amount on first and final call. The company received the application for 12,000 shares. applicants

On March 31, 2010, a company has 5,000 ₹100 14% preference shares. The preference shareholder can opt for any of the two options for the redemption of these shares. The options are (i) Redemption at par by cash payment and (ii) Conversion into equity shares of face value of ₹10 each at a

On March 31, 2010 2,000 ₹100 redeemable preference were outstanding. These are due for redemption at premium of 5%. The company issued necessary equity shares at par to provide for the redemption of preference shares. The balance sheet of the company discloses that it has general reserve of

J.K. Ltd invited application to issue 3,000 12% redeemable debentures of face value ₹100 each at par. The amount to be paid are ₹ 60 at the time of application, ₹30 on allotment, ₹10 per debenture on first and final call. The company received the application for 5,000 debentures, applicants

X Limited has 20,000; ₹100 each, 12% debentures on April 1, 2010. The terms of issue provide that every year 1/5 of debentures to be redeemed at par by annual drawings. In the year 2010–11, the required number of debentures was redeemed show necessary journal entries in the books of accounts.

On April 1, 2010 X Limited has 10,000; ₹100 each, 12% debentures. The terms of issue provide that every year 1/5 of debentures to be redeemed by making purchase from open market. During the year 2010–11, the company purchased the following debentures for immediate cancellation:(i) 800

On April 1, 2010, X Limited has 10,000; ₹100 each, 12% debentures. The terms of issue provide that every year 1/5 of debentures to be redeemed by making purchase from open market. During the year 2010–11, the company purchased the following debentures:(i) 800 debentures at a market price of

Debentures of face value ₹100 each are having a coupon rate 12% p.a. have a provision for interest payment every year on September 30 and March 31. The following were the market prices:(i) On July 1, cum-interest ₹99 per debenture (ii) On February 1, ex-interest ₹99.50 per debenture. If 200

On July 1, 2008, Dewee Limited issued 30,000 10% debentures of face value ₹100 each at par.After 18 months from the date of issue, each debenture is to be converted into four equity shares of face value ₹10 each at a premium of ₹15 each. On the date of conversion, all the debentures were

On April 1, 2007, Vycity Limited issued 2,000 ₹100 9% debentures at a premium of 10%. Debentures have a maturity of four years. To provide for the redemption of debentures, the company created debenture sinking fund at an interest rate of 5% per annum. Re. 0.2320185 invested @ 5% p.a. results

Taking the data of Example 21, show necessary accounts regarding redemption of debentures.Data from Example 21On April 1, 2007, Vycity Limited issued 2,000 ₹100 9% debentures at a premium of 10%. Debentures have a maturity of four years. To provide for the redemption of debentures, the company

J.K. Ltd invited application to issue 30,000 equity shares of face value ₹10 each at par. The amount to be paid as to ₹6 at the time of application, ₹3 on allotment, Re. 1 per share on first and final call. The company received the application for 50,000 shares, applicants for 5,000 shares

ABC Ltd was registered with an authorized share capital of ₹5,00,000 divided into 50,000 equity shares of face value of ₹10 each. Out of this on December 1, the company issued 30,000 shares that were fully subscribed by the public, the amount was payable as follows:On application ₹2; on

M.N. Ltd invited application to issue 10,000 equity shares of face value ₹10 each at 20% premium. The amount to be paid as to ₹5 (including ₹1 of premium) at the time of application, ₹5 (including Re. 1 of premium) on allotment, ₹1 per share on first and Re. 1 on second and final call.

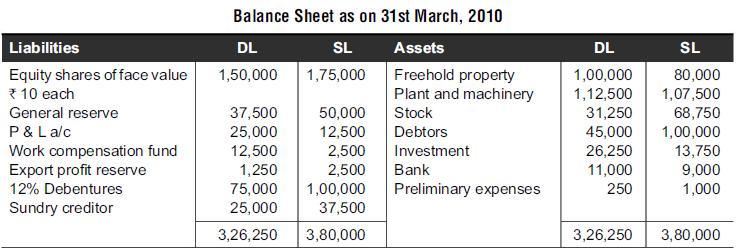

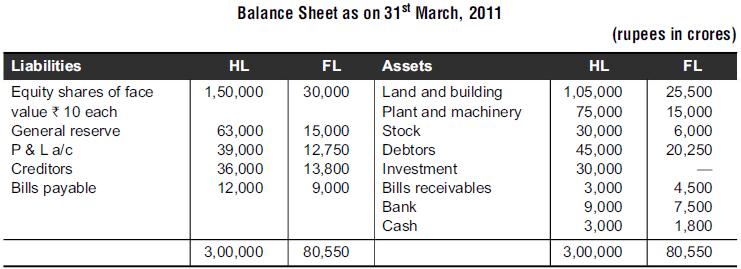

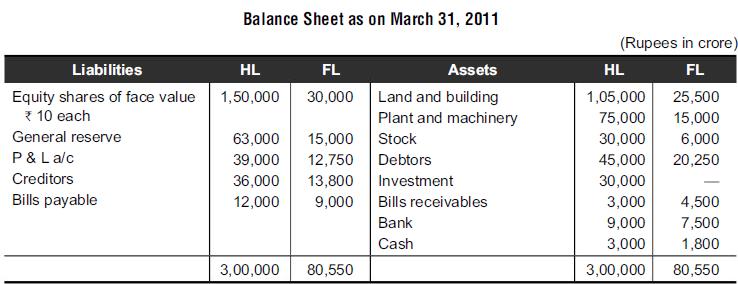

The balance sheets of Hanging Limited (HL) and Flat Limited (FL) on 31st March, 2011 are as follows:On the balance sheet date, HL acquired the business of FL for which it agrees to pay the following purchase consideration on the date of business combination.(i) HL to issue one share of its for

By taking the data of Example 4, assume that the clause (iv) is replaced with the clause “HL is to issue additional number of shares if market price of its shares falls below ₹21 by the end of financial year 2011–12 to keep the value of shares issued at the initial level.” Then show how

(i) Keeping the data of Example 5 and inserting the following provision, show how it should be recognized by HL.(ii) The fair value of assets can be assessed on the date of business combination but it has been included in the scheme of business combination that the proper estimation of fair value

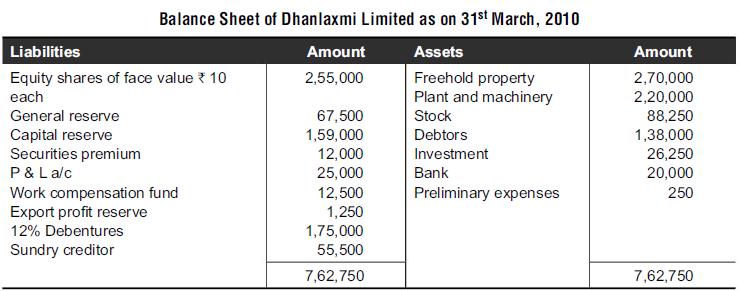

Dhanlaxmi Limited has two divisions. Namely Dhan and Laxmi. On 1st April, 2010, it decided to create a new company to which it will pass on the plant and machinery worth ₹1,00,000 and sundry creditors worth ₹50,000 for which newly established company Rooplaxmi Limited will issue shares of

Taking the data of Example 7, if Dhanlaxmi transfers all the debentures along with the plant and machinery and creditors mentioned therein and Rooplaxmi issues the shares of only ` 50,000 then how the balance sheets will appear.Data from Example 7Dhanlaxmi Limited has two divisions. Namely Dhan and

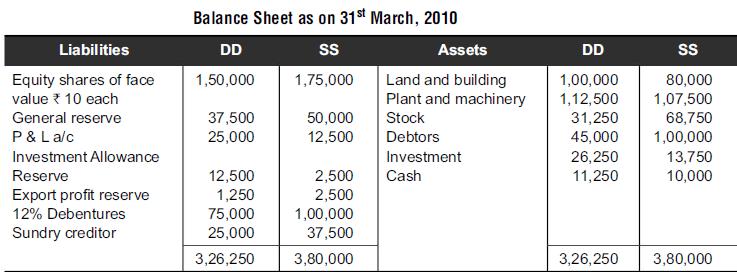

DD Limited and SS Limited amalgamated on 1st April, 2010. All the assets and liabilities of both the companies were acquired by newly established company DS Limited. Following was the balance sheet of both the companies on 1st April, 2010.DS agreed to issue required number of equity shares of face

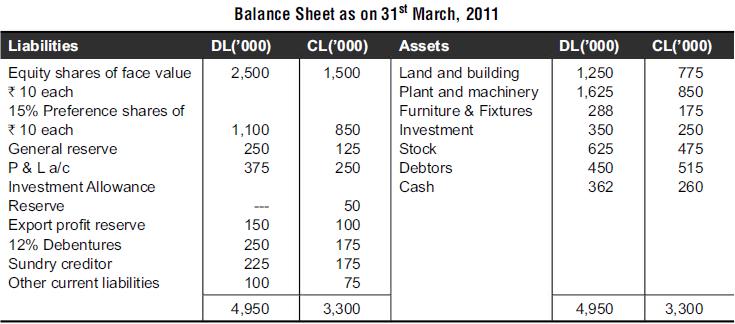

On 1st April, 2011, Dickins Limited (DL) acquired the business of Ceepee Limited (CL) by acquiring all the assets and liabilities at the book value it agreed to discharge the purchase consideration as follows:(i) To issue 1,75,000 equity shares of face value of ₹10 each to the equity

Taking the data of Example 10 under ‘amalgamation in the nature of merger’, show how realization account and equity shareholder’s account will appear in the books of CL and post amalgamation balance sheet in the books of DL.Data from Example 10On 1st April, 2011, Dickins Limited (DL) acquired

Taking the data of Example 9 & 10 and assuming that amalgamation is in the nature of purchase and that after the amalgamation acquirer is required to maintain statutory reserves, show how these will appear in the books of account of CL and DL.Data from Example 9DD Limited and SS Limited amalgamated

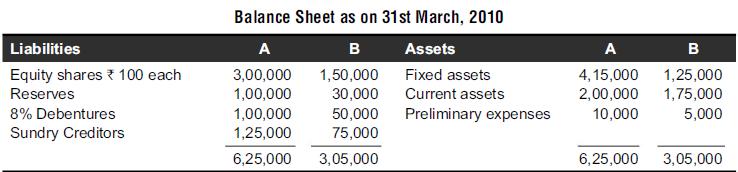

The following are the balance sheets of A and B as on 31st March, 2010:Goodwill of A and B is to be valued at ₹60,000 and ₹20,000, respectively. A purchased B on the basis of intrinsic value of shares. Show accounts in the books of B and post amalgamation balance sheet in the books of A.

Taking the data of Example 1, if we consider that GL purchased 30% equity of GHL at a cost of ₹2,15,000 and there was no difference between the book value and fair value of the assets. Then show how goodwill is to be recognized. If we further assume that the fair value of net assets increased by

Gee Limited (GL) is an associate of Jee Pee Limited (JPL). During the year, GL sold goods of selling price ₹3,00,000 to JPL. On March 31, 2011 closing stock of JPL comprised stock amounting to ₹70,000 out of the goods purchased from GL. Financial statements of GL disclose a gross profit

Gee Limited (GL) is an associate of Jee Pee Limited (JPL). During the year, JPL sold goods of selling price ₹3,00,000 to GL. On March 31, 2011, closing stock of GL comprised stock amounting to ₹70,000 out of the goods purchased from JPL. Financial statements of JPL disclose a gross profit

Suppose in Example 4, JPL sold a machinery to GL on which it earned a profit of ₹60,000. The useful life of the asset is ten years. JPL holds 45% equity in GL. Show how unrealized profit is to be recognized in the year 2010–11.Data from Example 4Gee Limited (GL) is an associate of Jee Pee

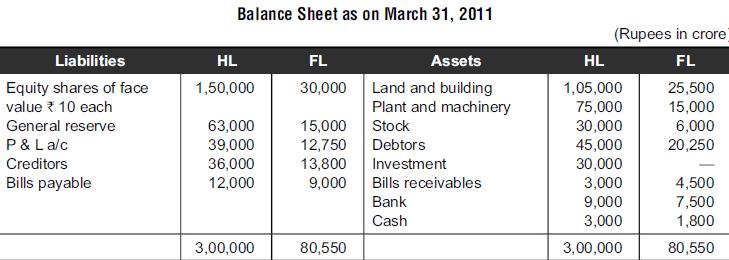

On October 1, 2010 Hanging Limited (HL) acquired 1,800 equity shares of ₹10 each of Flat Limited (FL) at a total market value of ₹ 25,500. The balance sheet of both the companies on March 31, 2011 is as follows:Out of the debtors and bills receivables of HL, ₹7,500 and ₹2,400,

X and Z are running their separate business and enter into a joint venture namely XZ by contribution capital in 2:3, respectively. During the course of business, Z sells a building of ₹6,00,000 and also sells stock worth ₹1,00,000 to XZ. Z makes 20% profit on both the transactions. By the end

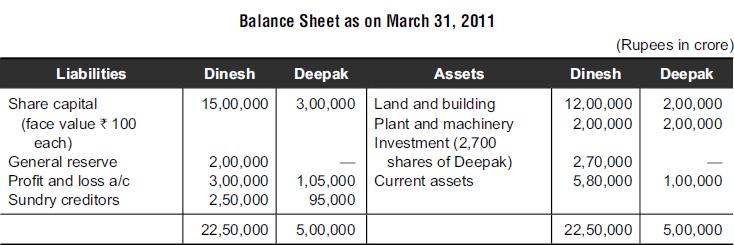

From the following balance sheet, prepare consolidated balance sheet of Dinesh Limited, which has one subsidiary namely Deepak Limited:Deepak Limited had a credit balance of ₹45,000 in its profit and loss account as on April 1, 2010. Dinesh Limited acquired shares in Deepak Limited on October

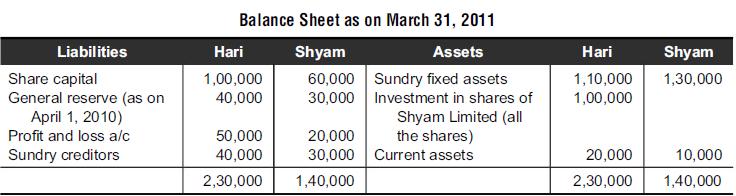

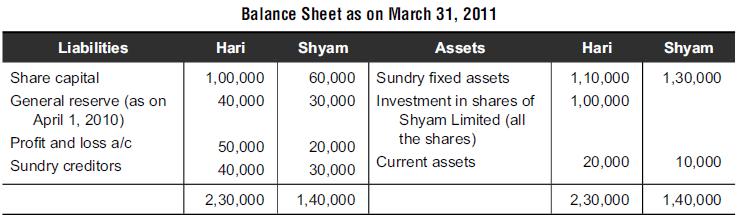

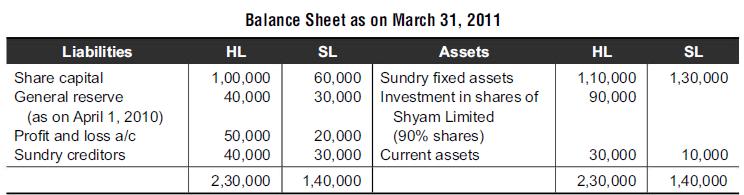

Hari Limited acquired all the shares of Shyam Limited on April 1, 2010 and the balance sheet of both the companies as on March 31, 2011 is as follows:The profit and loss account of Shyam Limited has a credit balance of ₹6,000 on April 1, 2010. Prepare consolidated financial statement as on March

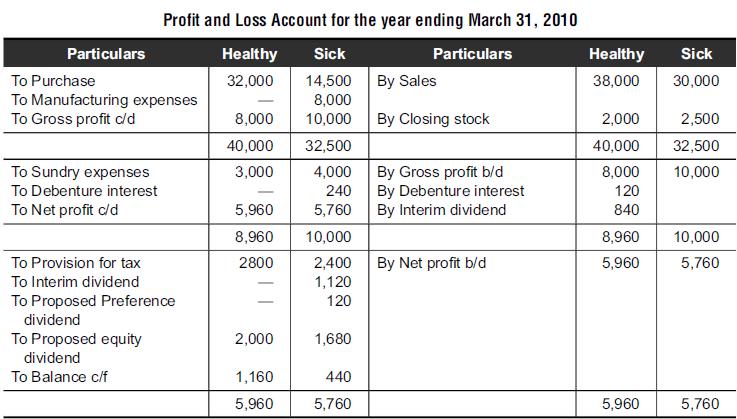

The following are the profit and loss accounts of Healthy Limited (HL) and Sick Limited (SL) for the year ending March 31, 2010:Additional Information:The following additional information is available:(i) The issued share capital of SL is 800 equity shares of ₹10 each fully paid and 200 6%

Hari Limited acquired all the shares of Shyam Limited on April 1, 2010 and the balance sheet of both the companies as on March 31, 2011 is as follows:The profit and loss account of Shyam Limited has a credit balance of ₹6,000 on April 1, 2010. Prepare consolidated financial statement as on March

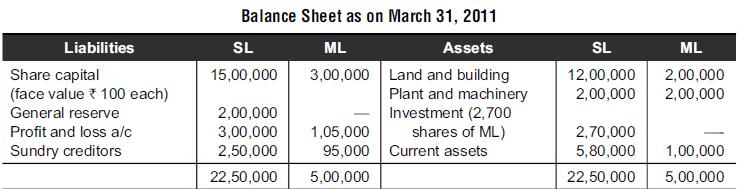

From the following balance sheet, prepare consolidated balance sheet of Simple Limited (SL) that has one subsidiary namely ML.ML had a credit balance of ₹45,000 in its profit and loss account as on April 1, 2010. SL acquired shares in ML Limited on October 1, 2010. On this date, land and building

On April 1, 2010 Hemant Limited (HL) acquired 1,650 equity shares of ₹10 each of Fuel Limited (FL) at a total market value of ₹ 29,000. The balance sheet of both the companies on March 31, 2011 is as follows:Out of the debtors and bills receivables of FL ₹7,500 and ₹2,400, respectively

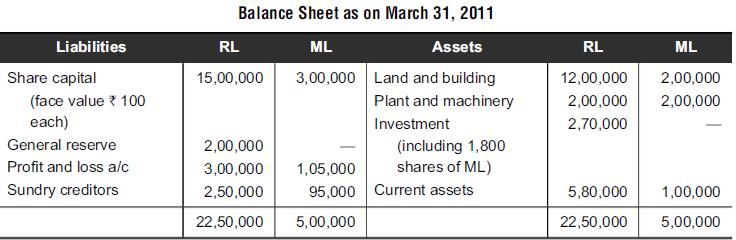

From the following balance sheet, prepare consolidated balance sheet of Ram Limited (RL) that has one subsidiary namely Mohan Limited (ML).ML had a credit balance of ₹45,000 in its profit and loss account as on April 1, 2010. RL acquired shares in ML on July 1, 2010 at a cost of ₹2,00,000.

Hari Limited (HL) acquired 90% shares of Shyam Limited (SL) on April 1, 2010 and the balance sheet of both the companies as on March 31, 2011 is as follows:The profit and loss account of Shyam Limited has a credit balance of ₹6,000 on April 1, 2010. The fair value of sundry fixed assets on the

Jindal Aluminum Limited (JAL) acquired a machinery from Jagson Enterprises (JE) for a lease term of four years, which covers almost complete economic life of the asset. The lease commences on April 1, 2009 and will expire on March 31, 2013. The fair value of the machine at the commencement of the

Taking the data of Example 1, apportion the total lease payments between finance charge and outstanding liability.Data from Example 1Jindal Aluminum Limited (JAL) acquired a machinery from Jagson Enterprises (JE) for a lease term of four years, which covers almost complete economic life of the

Zigna Limited (ZL) acquired machinery from Alok Healthcare (AH) on operating lease for a period of three years. The lease rent payable by ZL are ₹50,000; ₹1,10,000 and ₹1,40,000 during three years, respectively. Show how ZL should recognize the lease rent in its accounts.

Jagat Limited (JL), a lease finance company, leased a transport vehicle to Zig-Zag Transport Company (ZRL) the initial cost of the vehicle on April 1, 2008 is ₹12,00,000. The lessee, ZRL has agreed to pay equated lease rent at the end of each of the year over next four years. At the end of the

Using the data of Example 4, allocate the receivable from finance lease as to finance income and reduction in principal amount of the receivables to be recognized by the lessor over the lease term of four years.Data from Example 4Jagat Limited (JL), a lease finance company, leased a transport

Murti Finance and Leasing (MFL) buys passenger vehicles and gives these passenger vehicles on lease to corporate clients. It purchased 10 cars costing ₹6,00,000 each on April 1, 2007 and provided these cars on lease for a period of two years to one of its client Jims International (JI) by

Simson Limited (SL) has a mining equipment with carrying amount ₹1,20,000 and useful life of the equipment is 5 years. On April 1, 2006 SL enters into a package deal with a Sigma Finance Limited (SFL) whereby it sells the equipment to SFL with the condition to take the equipment on lease by

On April 1, 2009, a company is having an asset at a carrying amount ₹9,50,000 with fair value ₹11,00,000 and it has entered into a package deal with one of the finance companies to sell the asset with the condition to take it back on operating lease for a period of five years. How profit or

Deepak Enterprises (DE) acquired a machinery from Jagat Enterprises (JE) for a lease term of five years that covers almost complete economic life of the asset. The lease commences on April 1, 2009 and will expire on March 31, 2014. The fair value of the machine at the commencement of the lease term

Taking the data of Example 9, apportion the total lease payments between finance charge and outtanding liability for lessee.Data from Example 9Deepak Enterprises (DE) acquired a machinery from Jagat Enterprises (JE) for a lease term of five years that covers almost complete economic life of the

ZEN Limited (ZL) acquired a machinery from Ashok Healthcare (AH) on operating lease for a period of three years. The lease rent payable by ZL are ₹2,10,000; ₹1,20,000 and ₹2,40,000 during three years, respectively. Show how ZL should recognize the lease rent in its accounts.

On April 1, 2010, X Limited had 1,00,000 equity shares and it has profit after tax attributable to equity shareholders of ₹5,00,000. During the year 2010–11 on July 1, 2010, it issued 20,000 new shares and on January 1, 2011, 30,000 more shares were issued on conversion. The reported profit

A company has 3,600 equity shares on April 1, 2010 on August 31, 2010 company issued 1,200more shares and on February 1, 2011 it bought back 600 shares. Calculate weighted averagenumber of equity shares on March 31, 2011.

Aman Limited (AL) purchased goods worth ₹ 3,20,000 and ₹ 1,80,000 from Rajiv Limited (RL) on cash and for one-month credit, respectively. AL accepted a bill of exchange of two months’ duration for ₹ 2,00,000 in favour of Dilip Limited (DL). Do these transactions result in financial assets

PAT on April 1, 2010 is ₹1,20,000 with outstanding weighted average number of shares 50,000 of face value ₹10 each and fair value per share for the year 2010–11 is ₹20 per share. Weighted number of shares resulting from option due during the year 2010–11 is 10,000 with an exercise price

A company has profit after tax of ₹10,00,000 on April 1, 2011 with number of shares outstanding 5,00,000 of face value ₹10 each fully paid. On this date, there were 10,000 12% convertible debentures of face value ₹100 each convertible into 10 equity shares of face value ₹10 each fully paid

Profit after tax attributable to equity shares on March 31, 2010 is ₹18,00,000 and on March 31, 2011 is ₹60,00,000. The number of shares outstanding on March 31, 2010 was 40,00,000. On October 1, 2010, the company issued bonus shares in the ration of 2:1 by capitalization of profits. Calculate

On April 1, 2010 Jee Limited (JL) has 180 crore shares outstanding of face value ₹10 fully paid up. On January 31, 2011, it issued 60 crore more shares of face value ₹10 and ₹5 paid up. Calculate weighted average number of shares for calculating EPS.

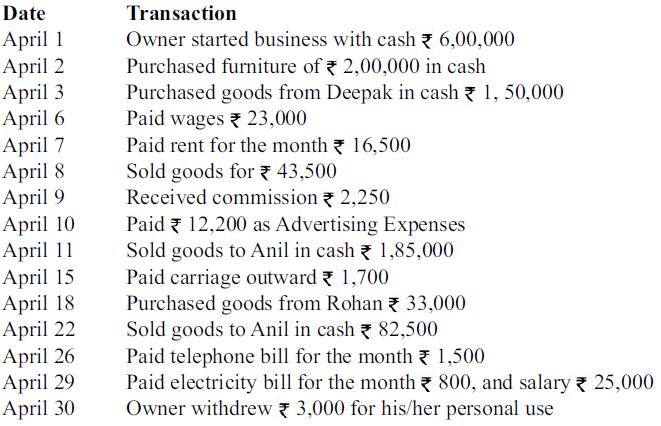

Pass necessary journal entries in the journal for the following transactions: Date April 1 April 2 April 3 April 6 April 7 April 8 April 9 April 10 April 11 April 15 April 18 April 22 April 26 April 29 April 30 Transaction Owner started business with cash 6,00,000 Purchased furniture of 2,00,000 in

Showing 300 - 400

of 7094

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

Last

Step by Step Answers