Joint cost apportionment and decision on further processing A company manufactures four products from an input of

Question:

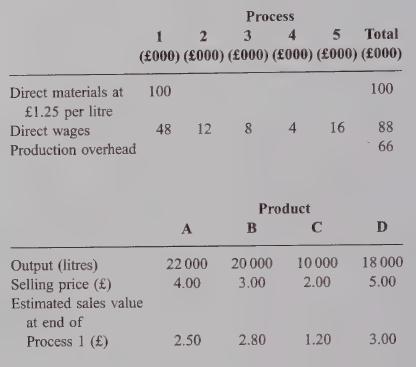

Joint cost apportionment and decision on further processing A company manufactures four products from an input of a raw material to process |. Following this process, product A is processed in process 2, product B in process 3, product C in process 4 and product D in process 5. The normal loss in process | is 10% of input, and there are no expected losses in the other processes. Scrap value in process | is £0.50 per litre. The costs incurred in process | are apportioned to each product according to the volume of output of each product. Production overhead is absorbed as a percentage of direct wages.

Data in respect of the month of October:

You are required to:

(a) calculate the profit or loss for each product for the month, assuming all output is sold at the normal selling price; (4 marks)

(b) suggest and evaluate an alternative production strategy which would optimize profit for the month. It should not be assumed that the output of process | can be changed;

(12 marks)

(c) suggest to what management should devote its attention, if it is to achieve the potential benefit indicated in (b).

Step by Step Answer: