Assume the Black-Scholes framework. Three months ago, you sold 1,000 units of a 1-year European put option

Question:

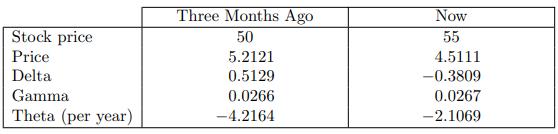

Assume the Black-Scholes framework. Three months ago, you sold 1,000 units of a 1-year European put option on a nondividend-paying stock. You immediately delta-hedged your position with appropriate number of shares of the stock, but have not ever re-balanced his portfolio. You now decide to close out all positions.

You are given:

(i) The stock’s volatility is 30%.

(ii) The put option is at-the-money currently.

(iii) Your careless secretary has provided you with the following values. However, she is not sure about whether these values are for the put option you sold or for a call option with the same strike, time to maturity, and underlying stock:

Calculate your three-month holding profit.

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Because the delta three months ago is positive while the current delta is negative the ...View the full answer

Answered By

Allan Simiyu

I am an adroit Writer. I am a dedicated writer having worked as a writer for 3 years now. With this, I am sure to ace in the field by helping students break down abstract concepts into simpler ideas.

8+ Reviews

54+ Question Solved

Related Book For

Question Posted: