18.17 Consider the regression model in matrix form Y = XB + WG + U, where X...

Question:

18.17 Consider the regression model in matrix form Y = XB + WG + U, where X and W are matrices of regressors and B and G are vectors of unknown regression coefficients. Let X

= MWX and Y

= MWY, where MW = I - W(WW)-1W.

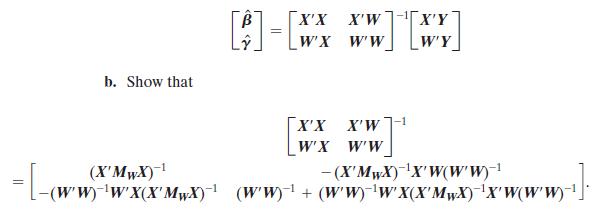

a. Show that the OLS estimators of B and G can be written as

(Hint: Show that the product of the two matrices is equal to the identity matrix.)

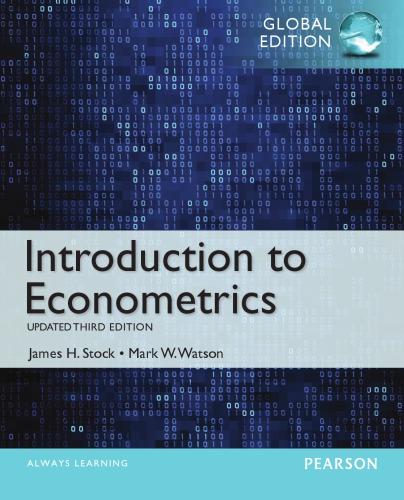

c. Show that B n = (XMWX)-1XMWY.

d. The Frisch–Waugh theorem (Appendix 6.2) says that B n = (XX)-1XY. Use the result in

(c) to prove the Frisch–Waugh theorem.

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Answered By

Mishark muli

Having any assignments and any other research related work? worry less for I am ready to help you with any task. I am quality oriented and dedicated always to produce good and presentable work for the client once he/she entrusts me with their work. i guarantee also non plagiarized work and well researched work to give you straight As in all your units.Feel free to consult me for any help and you will never regret

11+ Reviews

37+ Question Solved

Related Book For

Introduction To Econometrics

ISBN: 9781292071367

3rd Global Edition

Authors: James Stock, Mark Watson

Question Posted: