Using risk-neutral valuation, derive a formula for a derivative that pays cash flows over the next two

Question:

Using risk-neutral valuation, derive a formula for a derivative that pays cash flows over the next two periods. Assume the risk-free rate is 4 percent per period.

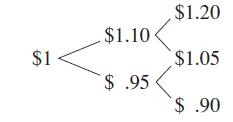

The underlying asset, which pays no cash flows unless it is sold, has a market value that is modeled in the adjacent tree diagram.

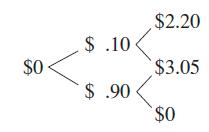

The cash flows of the derivative that correspond to the above tree diagram are

Find the present value of the derivative.AppendixLO1

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Answered By

Felix Mucee

I am a detailed and thorough professional writer with 5 years of administrative experience- the last 2 years in academic writing and virtual office environment. I specialize in delivering quality services with respect to strict deadlines and high expectations. I am equipped with a dedicated home office complete with a computer, copier/scanner/fax and color printer.

I provide creative and detailed administrative, web search, academic writing, data entry, Personal assistant, Content writing, Translation, Academic writing, editing and proofreading services. I excel at working under tight deadlines with strict expectations. I possess the self-discipline and time management skills necessary to have served as an academic writer for the past five years. I can bring value to your business and help solve your administrative assistant issues.

13+ Reviews

33+ Question Solved

Related Book For

Financial Markets And Corporate Strategy

ISBN: 9780077119027

1st Edition

Authors: David Hillier, Mark Grinblatt, Sheridan Titman

Question Posted: