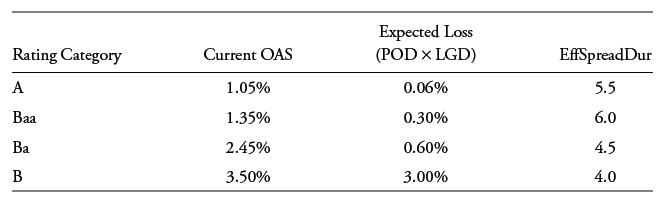

An active credit portfolio manager considers the following corporate bond portfolio choices familiar from an earlier example:

Question:

An active credit portfolio manager considers the following corporate bond portfolio choices familiar from an earlier example:

The investor anticipates an economic slowdown in the next year that will have a greater adverse impact on lower-rated issuers. Assume that an index portfolio is equally allocated across all four rating categories, while the investor chooses a tactical portfolio combining equal long positions in the investment-grade (A and Baa) bonds and short positions in the high-yield (Ba and B) bonds.

Calculate excess spread on the index and tactical portfolios assuming no change in spreads over the next year (ignoring spread duration changes).

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

The following table summarizes expected excess returns E Excess Spread Spreado EffSpreadDur AS...View the full answer

Answered By

PALASH JHANWAR

I am a Chartered Accountant with AIR 45 in CA - IPCC. I am a Merit Holder ( B.Com ). The following is my educational details.

PLEASE ACCESS MY RESUME FROM THE FOLLOWING LINK: https://drive.google.com/file/d/1hYR1uch-ff6MRC_cDB07K6VqY9kQ3SFL/view?usp=sharing

3+ Reviews

10+ Question Solved

Related Book For

Question Posted: