Which of the following statements best characterizes how the active portfolio is positioned for yield curve changes

Question:

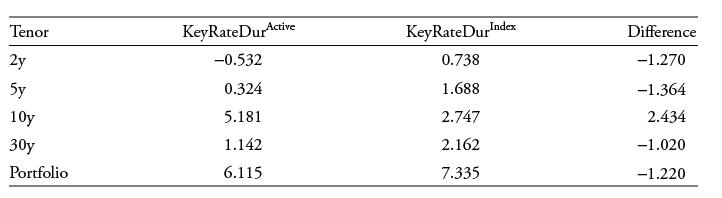

Which of the following statements best characterizes how the active portfolio is positioned for yield curve changes relative to the index portfolio?

A. The active portfolio is positioned to benefit from a bear steepening of the yield curve versus the benchmark portfolio.

B. The active portfolio is positioned to benefit from a positive butterfly movement in the shape of the yield curve versus the index.

C. The active portfolio is positioned to benefit from yield curve flattening versus the index.

A financial analyst at an in-house asset manager fund has created the following spreadsheet of key rate durations to compare her active position to that of a benchmark index so she can compare the rate sensitivities across maturities.

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

The active portfolio is positioned to benefit from a yield curve flattening versus the index This ca...View the full answer

Answered By

Utsab mitra

I have the expertise to deliver these subjects to college and higher-level students. The services would involve only solving assignments, homework help, and others.

I have experience in delivering these subjects for the last 6 years on a freelancing basis in different companies around the globe. I am CMA certified and CGMA UK. I have professional experience of 18 years in the industry involved in the manufacturing company and IT implementation experience of over 12 years.

I have delivered this help to students effortlessly, which is essential to give the students a good grade in their studies.

2+ Reviews

10+ Question Solved

Related Book For

Question Posted: