In this chapter, you have learned that the cost of merchandise is a significant cost for all

Question:

In this chapter, you have learned that the cost of merchandise is a significant cost for all merchandising businesses.

In order to maximize profits, management attempts to keep this cost as low as possible. There are four basic components included in every sales dollar. One of these components is the cost of merchandise sold. The component percentage for cost of merchandise sold is calculated by dividing merchandise costs by the amount of net sales.

Instructions:

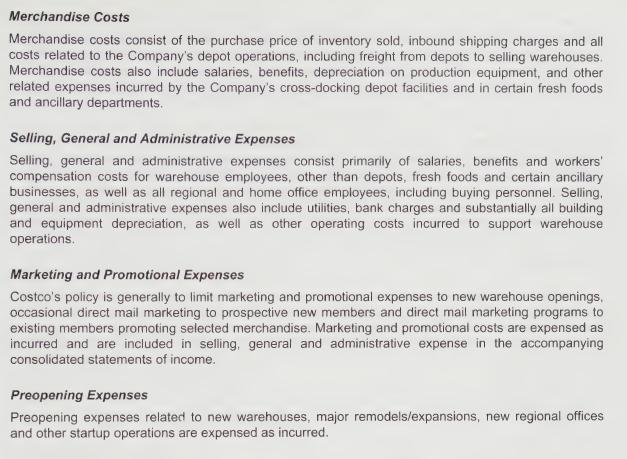

1. Referring to the Notes to Consolidated Financial Statements on Appendix page B-15 in this textbook, describe what Costco considers to be the cost of merchandise sold beyond the purchase price of inventory sold.

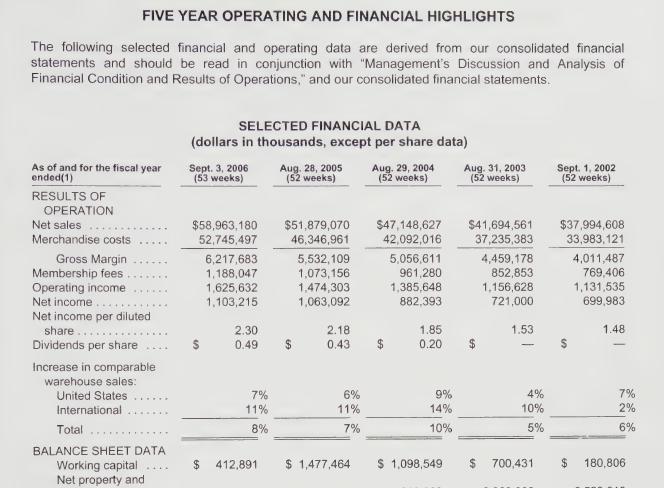

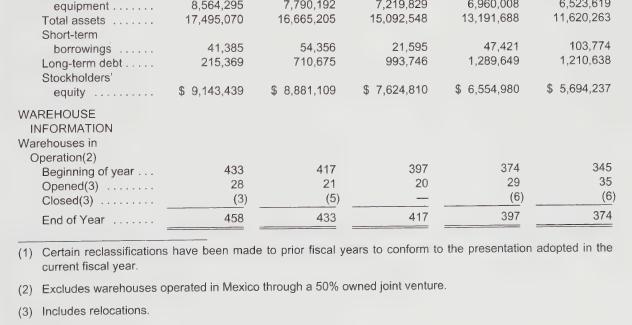

2. Referring to the five-year operating and financial highlights on Appendix page B-3:

a. List the component percentages of net sales for merchandise costs for each year beginning a 2002 and ending with 2006.

b. Looking at the component percentages for each year beginning with 2002, describe any trends regarding merchandise costs.

c. Would you classify the trend identified in question 3 as “favorable” or “unfavorable” for Costco? Explain.

d. For every \($100\) in net sales in 2006, how much did Costco spend to obtain merchandise? For every \($100\) in net sales in 2002, how much did Costco spend to obtain merchandise?

Data from Appendix page B-3

Data from Appendix page B-15

Step by Step Answer: