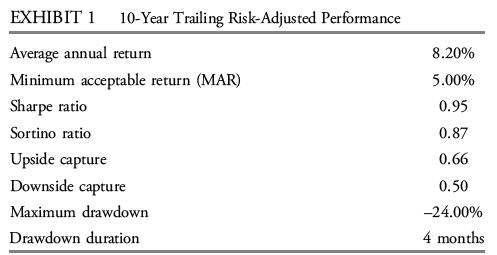

The maximum drawdown and drawdown duration in Exhibit 1 indicate that: A. the portfolio recovered quickly from

Question:

The maximum drawdown and drawdown duration in Exhibit 1 indicate that:

A. the portfolio recovered quickly from its maximum loss.

B. over the 10-year period, the average maximum loss was –24.00%.

C. a significant loss once persisted for four months before the portfolio began to recover.

Alexandra Jones, a senior adviser at Federalist Investors (FI), meets with Erin Bragg, a junior analyst. Bragg just completed a monthly performance evaluation for an FI fixed-income manager. Bragg’s report addresses the three primary components of performance evaluation:

measurement, attribution, and appraisal. Jones asks Bragg to describe an effective attribution process. Bragg responds as follows:

Response 1: Performance attribution draws conclusions regarding the quality of a portfolio manager’s investment decisions.

Response 2: Performance attribution should help explain how performance was achieved by breaking apart the return or risk into different explanatory components.

Bragg notes that the fixed-income portfolio manager has strong views about the effects of macroeconomic factors on credit markets and follows a top-down investment process.

Jones reviews the monthly performance attribution and asks Bragg whether any riskadjusted historical performance indicators are available. Bragg produces the following data:

Step by Step Answer:

The maximum drawdown and drawdown duration in Exhibit 1 indicate that C a significant l...View the full answer