Consider the HullWhite model where the short rate is defined by Suppose we define a new variable

Question:

Consider the Hull–White model where the short rate is defined by

![]()

Suppose we define a new variable x(t) where

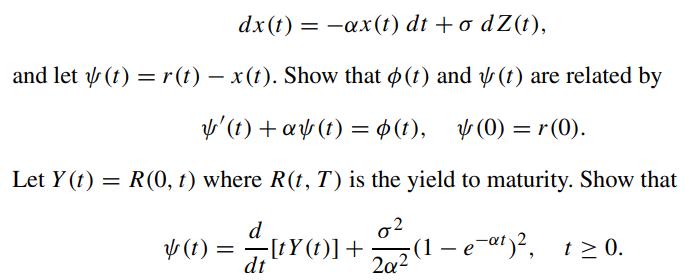

Also, show that the bond price B(t,T ) can be expressed as (Kijima and Nagayama, 1994)

![B(0, T) B(0, t) 0 + 43 {1-[2-e-a(T-1)]+ (2 - e- - (2 eat)}. In B(t, T) In + - - - [e-a (T-1) e-(Tt) 1][r(t)](https://dsd5zvtm8ll6.cloudfront.net/images/question_images/1700/5/7/7/938655cc292124f11700577935127.jpg)

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Answered By

Utsab mitra

I have the expertise to deliver these subjects to college and higher-level students. The services would involve only solving assignments, homework help, and others.

I have experience in delivering these subjects for the last 6 years on a freelancing basis in different companies around the globe. I am CMA certified and CGMA UK. I have professional experience of 18 years in the industry involved in the manufacturing company and IT implementation experience of over 12 years.

I have delivered this help to students effortlessly, which is essential to give the students a good grade in their studies.

2+ Reviews

10+ Question Solved

Related Book For

Question Posted: