Question

Scofield Enterprises has been operating for one year and the company needs additional working capital to expand its business. The owner doesn't really know whether

Scofield Enterprises has been operating for one year and the company needs additional working capital to expand its business. The owner doesn't really know whether the business is profitable or not, but she is sure from the increase in orders already experienced that the business concept can be successful. Now she needs to provide GAAP-compliant financial statements to the banker and may hire your company to create them. The company has been entering information in general ledger software all year and the software has generated an Unadjusted Trial Balance which is available separately in a spreadsheet. The owner of Scofield Enterprises sat down with your boss this week when she realized that the bank wasn't going to accept the computer output, and their conversation is available at ACCT 3310 Professional Application: Part I provided below in this folder.

Listen to and watch the conversation between the accountant and the owner at ACCT 3310 - Professional Application: Part I. Use the unadjusted trial balance on the Original Trial Balance worksheet, plus the information you gather from the owner / accountant's discussion to develop GAAP-compliant financial statements Prepare adjusting / error correction journal entries in the General Journal worksheet. Prepare an Adjusted Trial Balance on the Trial Balance worksheet. Prepare an Income Statement, Statement of Retained Earnings, and Balance Sheet Prepare a memorandum in a separate WORD file to the owner that presents your evaluation of the company's cash management and profitability and explains the transformation of the unadjusted trial balance to finished financial statements.

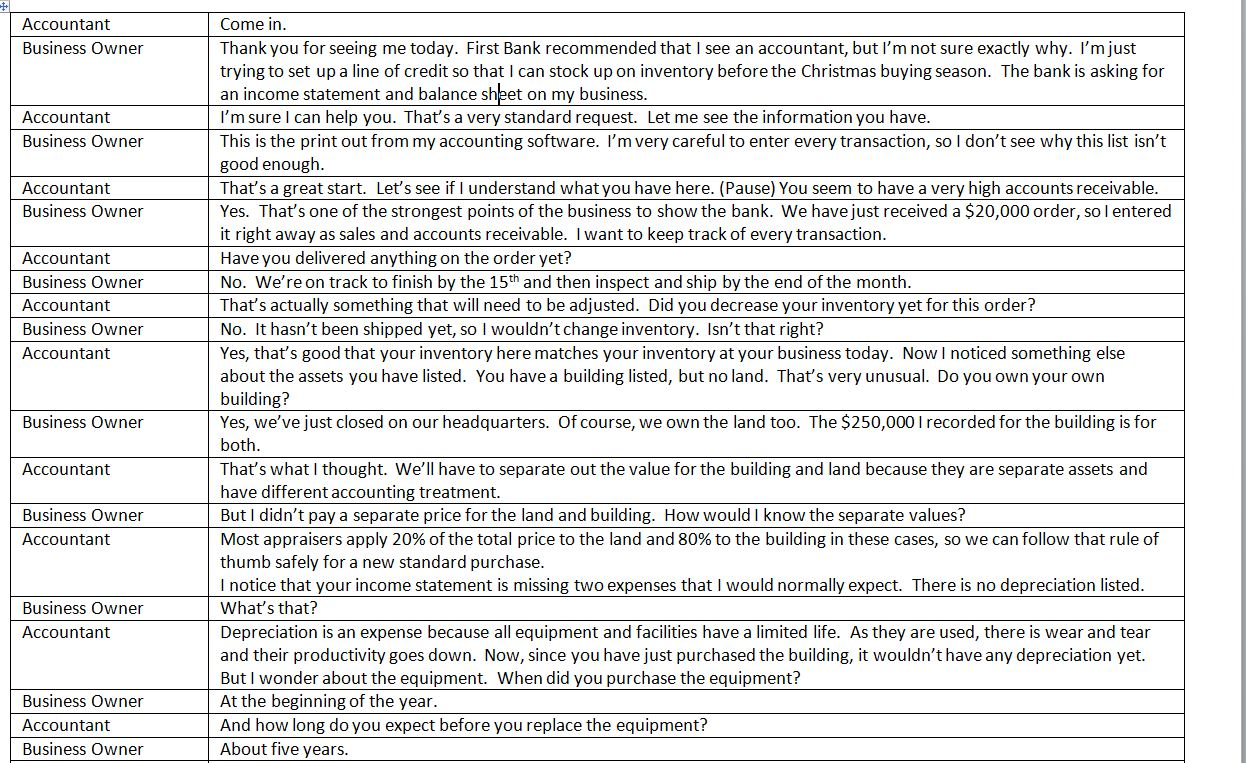

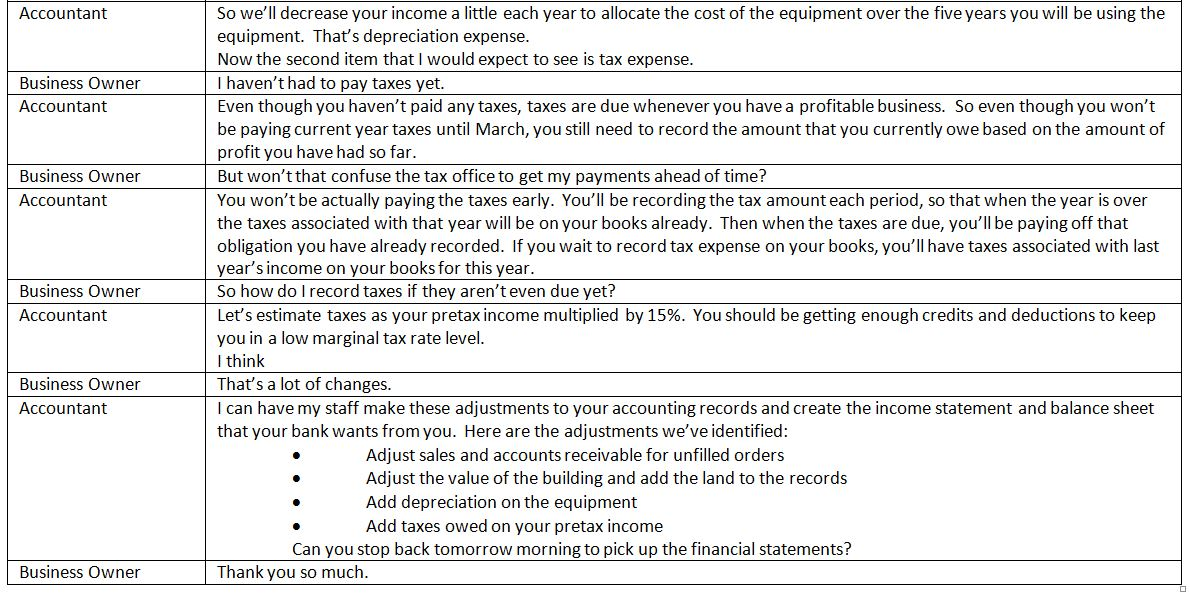

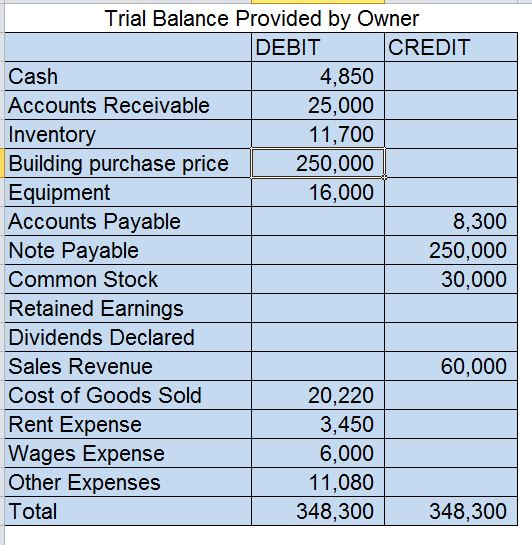

Accountant Business Owner Accountant Business Owner Accountant Business Owner Accountant Business Owner Accountant Business Owner Accountant Business Owner Accountant Business Owner Accountant Business Owner Accountant Business Owner Accountant Business Owner Come in. Thank you for seeing me today. First Bank recommended that I see an accountant, but I'm not sure exactly why. I'm just trying to set up a line of credit so that I can stock up on inventory before the Christmas buying season. The bank is asking for an income statement and balance sheet on my business. I'm sure I can help you. That's a very standard request. Let me see the information you have. This is the print out from my accounting software. I'm very careful to enter every transaction, so I don't see why this list isn't good enough. That's a great start. Let's see if I understand what you have here. (Pause) You seem to have a very high accounts receivable. Yes. That's one of the strongest points of the business to show the bank. We have just received a $20,000 order, so I entered it right away as sales and accounts receivable. I want to keep track of every transaction. Have you delivered anything on the order yet? No. We're on track to finish by the 15th and then inspect and ship by the end of the month. That's actually something that will need to be adjusted. Did you decrease your inventory yet for this order? No. It hasn't been shipped yet, so I wouldn't change inventory. Isn't that right? Yes, that's good that your inventory here matches your inventory at your business today. Now I noticed something else about the assets you have listed. You have a building listed, but no land. That's very unusual. Do you own your own building? Yes, we've just closed on our headquarters. Of course, we own the land too. The $250,000 I recorded for the building is for both. That's what I thought. We'll have to separate out the value for the building and land because they are separate assets and have different accounting treatment. But I didn't pay a separate price for the land and building. How would I know the separate values? Most appraisers apply 20% of the total price to the land and 80% to the building in these cases, so we can follow that rule of thumb safely for a new standard purchase. I notice that your income statement is missing two expenses that I would normally expect. There is no depreciation listed. What's that? Depreciation is an expense because all equipment and facilities have a limited life. As they are used, there is wear and tear and their productivity goes down. Now, since you have just purchased the building, it wouldn't have any depreciation yet. But I wonder about the equipment. When did you purchase the equipment? At the beginning of the year. And how long do you expect before you replace the equipment? About five years. Accountant Business Owner Accountant Business Owner Accountant Business Owner Accountant Business Owner Accountant Business Owner So we'll decrease your income a little each year to allocate the cost of the equipment over the five years you will be using the equipment. That's depreciation expense. Now the second item that I would expect to see is tax expense. I haven't had to pay taxes yet. Even though you haven't paid any taxes, taxes are due whenever you have a profitable business. So even though you won't be paying current year taxes until March, you still need to record the amount that you currently owe based on the amount of profit you have had so far. But won't that confuse the tax office to get my payments ahead of time? You won't be actually paying the taxes early. You'll be recording the tax amount each period, so that when the year is over the taxes associated with that year will be on your books already. Then when the taxes are due, you'll be paying off that obligation you have already recorded. If you wait to record tax expense on your books, you'll have taxes associated with last year's income on your books for this year. So how do I record taxes if they aren't even due yet? Let's estimate taxes as your pretax income multiplied by 15%. You should be getting enough credits and deductions to keep you in a low marginal tax rate level. I think That's a lot of changes. I can have my staff make these adjustments to your accounting records and create the income statement and balance sheet that your bank wants from you. Here are the adjustments we've identified: Adjust sales and accounts receivable for unfilled orders. Adjust the value of the building and add the land to the records Add depreciation on the equipment Add taxes owed on your pretax income Can you stop back tomorrow morning to pick up the financial statements? Thank you so much. Trial Balance Provided by Owner DEBIT Cash Accounts Receivable Inventory Building purchase price Equipment Accounts Payable Note Payable Common Stock Retained Earnings Dividends Declared Sales Revenue Cost of Goods Sold Rent Expense Wages Expense Other Expenses Total 4,850 25,000 11,700 250,000 16,000 20,220 3,450 6,000 11,080 348,300 CREDIT 8,300 250,000 30,000 60,000 348,300

Step by Step Solution

3.40 Rating (150 Votes )

There are 3 Steps involved in it

Step: 1

Income Statement Particulars Amount SalesAdjusted for unfilled order ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Document Format ( 2 attachments)

60901d2b1bf4d_21496.pdf

180 KBs PDF File

60901d2b1bf4d_21496.docx

120 KBs Word File

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Intermediate Accounting

Authors: James D. Stice, Earl K. Stice, Fred Skousen

17th Edition

032459237X, 978-0324592375