Answered step by step

Verified Expert Solution

Question

1 Approved Answer

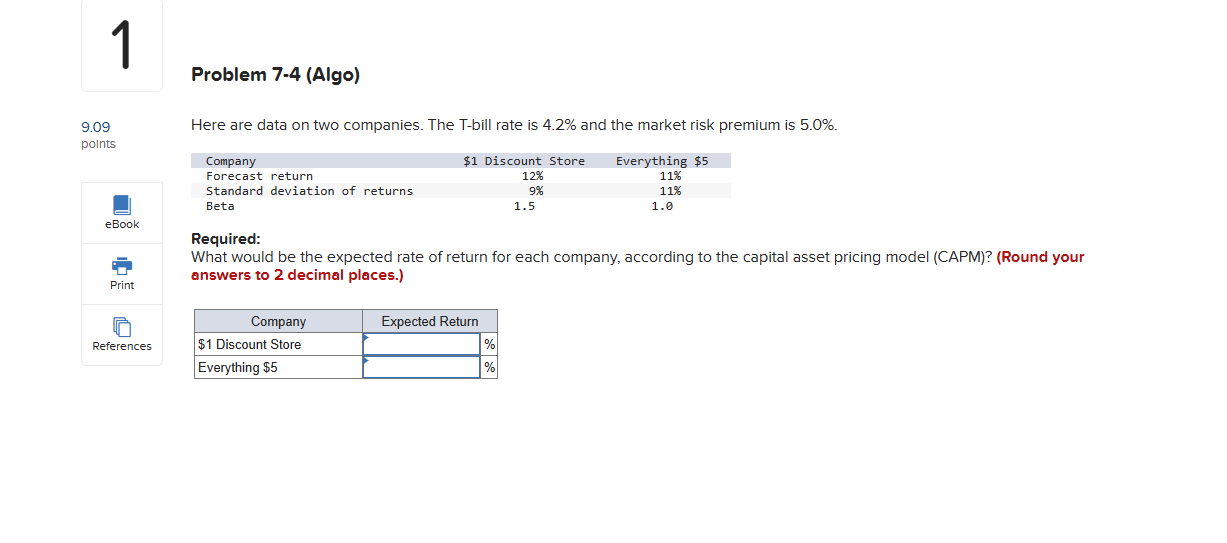

1 9.09 points Problem 7-4 (Algo) Here are data on two companies. The T-bill rate is 4.2% and the market risk premium is 5.0%.

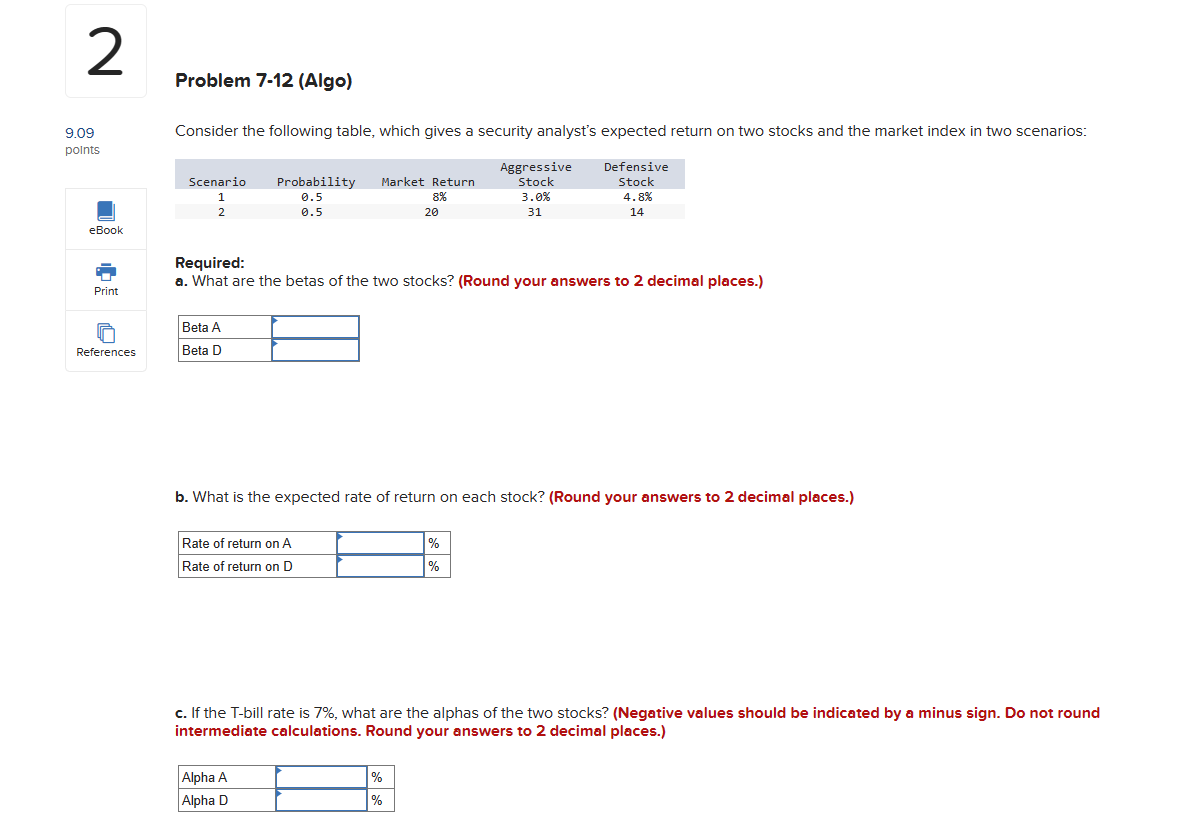

1 9.09 points Problem 7-4 (Algo) Here are data on two companies. The T-bill rate is 4.2% and the market risk premium is 5.0%. Company $1 Discount Store Forecast return 12% Standard deviation of returns Beta 9% 1.5 eBook Print Everything $5 11% 11% 1.0 Required: What would be the expected rate of return for each company, according to the capital asset pricing model (CAPM)? (Round your answers to 2 decimal places.) Company Expected Return References $1 Discount Store Everything $5 % % 2 Problem 7-12 (Algo) 9.09 points Consider the following table, which gives a security analyst's expected return on two stocks and the market index in two scenarios: Aggressive Defensive Scenario 1 2 Probability 0.5 0.5 Market Return 8% Stock 3.0% Stock 4.8% 20 31 14 eBook Print References Required: a. What are the betas of the two stocks? (Round your answers to 2 decimal places.) Beta A Beta D b. What is the expected rate of return on each stock? (Round your answers to 2 decimal places.) Rate of return on A Rate of return on D % % c. If the T-bill rate is 7%, what are the alphas of the two stocks? (Negative values should be indicated by a minus sign. Do not round intermediate calculations. Round your answers to 2 decimal places.) Alpha A Alpha D % %

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Venture capital and the finance of innovation

Authors: Andrew Metrick

2nd Edition

9781118137888, 470454709, 1118137884, 978-0470454701