-

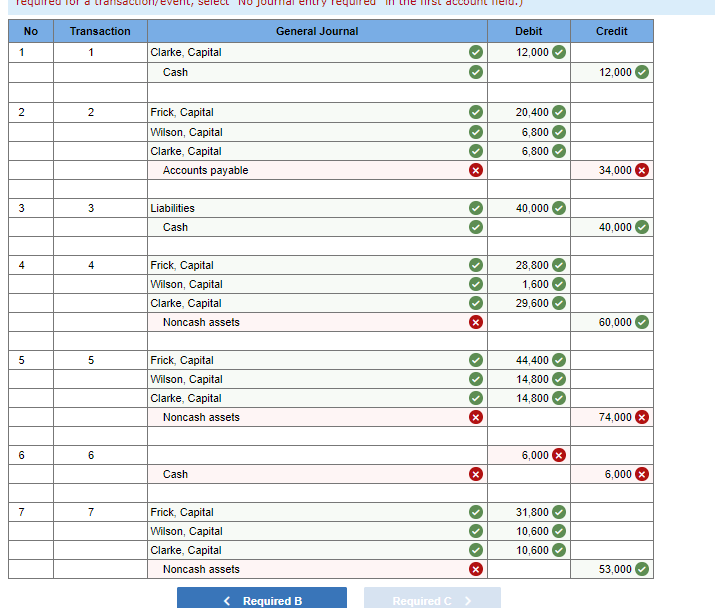

1

Record the entry for initial cash payments made to partners in accordance with predistribution plan.

-

2

Record the allocation of losses to partners on sale of noncash assets.

-

3

Record the extinguishment of all partnership liabilities.

-

4

Record the entry for cash payments made to partners in accordance with predistribution plan.

-

5

Record the allocation of losses to partners on sale of remaining noncash assets.

-

6

Record the payment of liquidation expenses.

-

7

Record the entry for final cash payments made to partners based on ending capital balances.

-

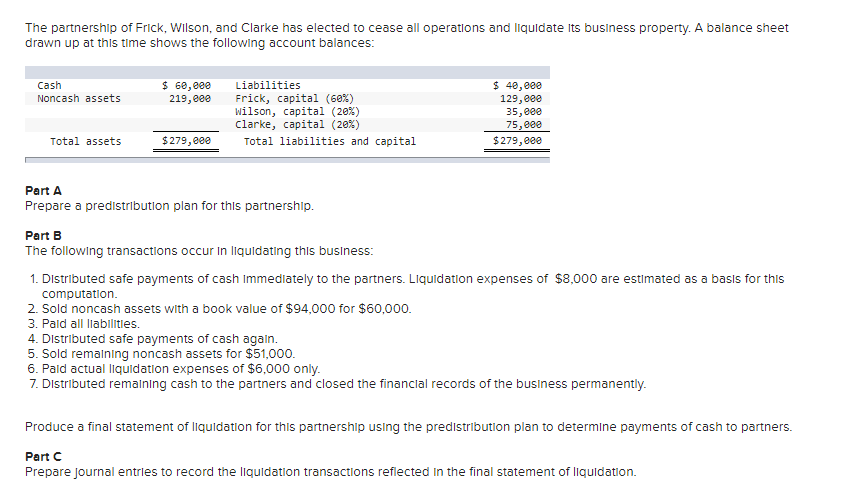

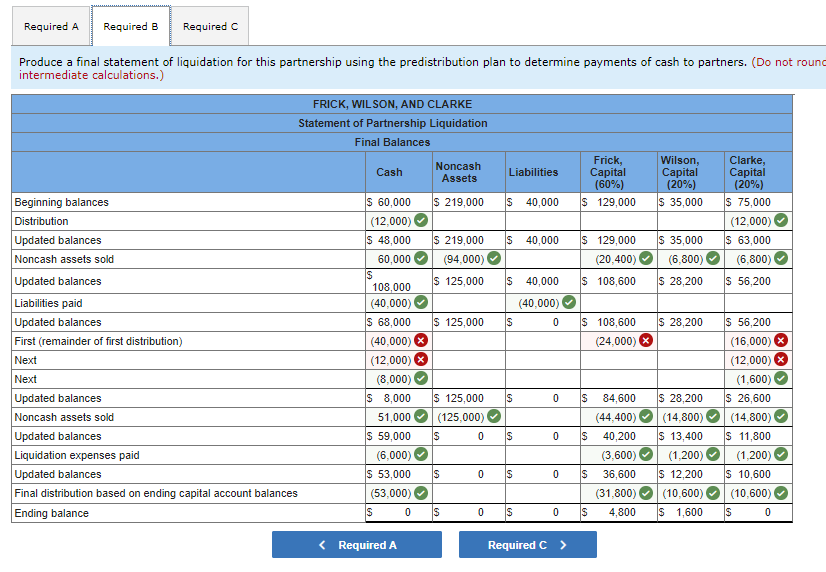

The partnership of Frick, Wilson, and Clarke has elected to cease all operations and liquidate Its business property. A balance sheet drawn up at this time shows the following account balances: Cash Noncash assets $ 60, eee 219, eee Liabilities Frick, capital (60%) Wilson, capital (20%) Clarke, capital (20%) Total liabilities and capital $ 40, eee 129, eee 35, eee 75, eee $ 279, eee Total assets $ 279, eee Part A Prepare a predistribution plan for this partnership. Part B The following transactions occur in liquidating this business: 1. Distributed safe payments of cash Immediately to the partners. Liquidation expenses of $8,000 are estimated as a basis for this computation. 2. Sold noncash assets with a book value of $94,000 for $60,000. 3. Pald all liabilities. 4. Distributed safe payments of cash again. 5. Sold remaining noncash assets for $51,000. 6. Pald actual liquidation expenses of $6,000 only. 7. Distributed remaining cash to the partners and closed the financial records of the business permanently. Produce a final statement of liquidation for this partnership using the predistribution plan to determine payments of cash to partners. Part C Prepare Journal entries to record the liquidation transactions reflected in the final statement of liquidation. Required A Required B Required Produce a final statement of liquidation for this partnership using the predistribution plan to determine payments of cash to partners. (Do not round intermediate calculations.) FRICK, WILSON, AND CLARKE Statement of Partnership Liquidation Final Balances Noncash Frick, Wilson, Clarke, Cash Assets Liabilities Capital Capital Capital (60%) (20%) (20%) Beginning balances $ 60,000 $ 219,000 S 40,000 $ 129,000 $ 35,000 $ 75,000 Distribution (12,000) (12,000) Updated balances $ 48,000 $ 219,000 IS 40,000 $ 129,000 $ 35,000 $ 63,000 Noncash assets sold 60,000 (94000) (20,400) (6.800) (6,800) S Updated balances $ 125,000 $ 40,000 108,000 $ 108,600 $ 28,200 $ 56,200 Liabilities paid (40,000) (40,000) Updated balances $ 68,000 $ 125,000 S 0 $ 108,600 $ 28,200 $ 56,200 First (remainder of first distribution) (40,000) (24,000) (16,000) Next (12,000) (12,000) Next (8,000) (1,600) Updated balances $ 8,000 $ 125,000 S 0 S 84,600 $ 28,200 $ 26,600 Noncash assets sold 51,000 (125.000) (44,400) (14.800) (14,800) Updated balances $ 59,000 IS 0 S 0 S 40,200 $ 13,400 $ 11,800 Liquidation expenses paid (6.000) (3.600) (1,200) (1.200) Updated balances $ 53,000 S 0 S 0 S 36,600 $ 12,200 $ 10,600 Final distribution based on ending capital account balances (53.000) (31.800) (10.600) (10,600) Ending balance 0 S 0 0 4.800 $ 1,600 $ 0 HITSL account No Transaction General Journal Debit Credit 1 1 12.000 Clarke, Capital Cash 12.000 2 2 Frick, Capital Wilson, Capital Clarke, Capital Accounts payable XOOO 20,400 6,800 6,800 34,000 3 3 40,000 Liabilities Cash 40,000 4 4 Frick, Capital Wilson, Capital Clarke, Capital Noncash assets XOOO 28,800 1,600 29,600 60.000 5 5 44,400 Frick, Capital Wilson, Capital Clarke, Capital Noncash assets 14,800 14,800 74,000 6 6 6,000 Cash X 6,000 7 7 Frick, Capital Wilson, Capital Clarke, Capital Noncash assets 31,800 10,600 10,600 53,000